Here’s Why A “Company Owned” Model Works For Starbucks

Restaurant companies are employing different methods of expansion and efficient management. While McDonald’s is moving towards a 95% franchised model and Burger King (owned by Restaurants Brand International) is already operating an efficient franchised model, nearly 50% of the 25,000+ restaurants of Starbucks (NYSE:SBUX) are still company owned. The company is growing aggressively but its expansion strategy is not based on a shift towards a franchised based model. Our forecast estimates that by 2023, the company will still have a 50:50 ratio for franchised and company owned restaurants.

Maintaining Company Culture And A Higher Control Over Employees

Higher operating expenses for company-owned restaurants, higher capital spend, and the ease in expansion through a franchisee model has encouraged other restaurant companies to shift towards a fully franchised model. As McDonald’s works on this transition the company has started witnessing a growth in operating profits. However, a franchise-based model leads to lower control of the company management on day-to-day operations and Starbucks’ management wants to maintain a certain level of control on its stores and hence favors company-owned restaurants. The company wants its baristas to understand its culture, vision, and value statement, and believes that this is possible only if its restaurants are company owned. While Starbucks has adopted the franchisee model for international expansion and several of its domestic stores are also licensed, the company still has a significant percentage of company owned stores in order to maintain its culture.

Efficiently Run, Profitable Company-Owned Restaurants

- Down 7% Since 2023, Can Starbucks’ Stock Reverse This Trend Post Q1 Results?

- Down 26% From Its Pre-Inflation Shock High, What Is Next For Starbucks Stock?

- After 6% Drop This Year, Pricing Growth To Bolster Starbucks’ Q4

- Can Starbucks Stock Return To Pre-Inflation Shock Highs?

- Starbucks’ Stock To See Little Movement Past Q3?

- Starbucks Stock To Likely Trade Lower Post Q2

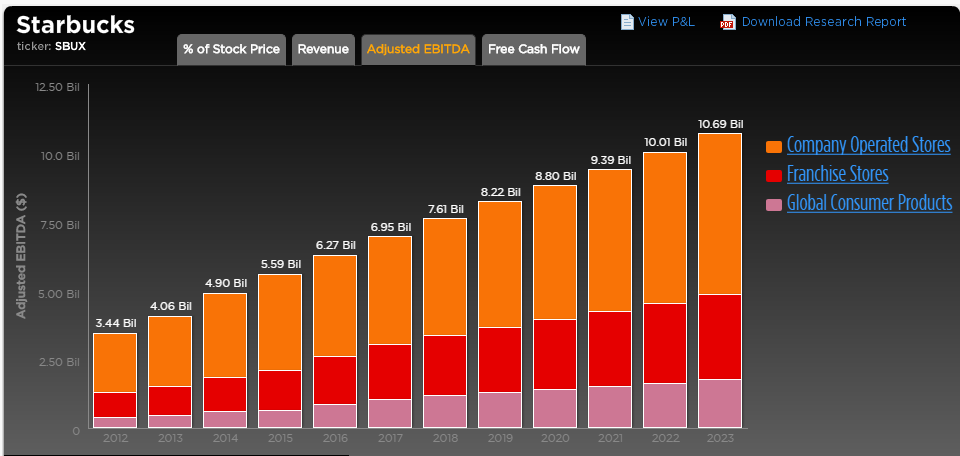

Starbucks has been running its company-owned restaurants efficiently and the company generates a higher EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization) margin from these stores compared to its peers. The company generated a 21% EBITDA margin from its company-owned restaurants in 2016 (and we estimate a similar figure for 2017) compared to the 19% figure for McDonald’s. Chipotle Mexican Grill which follows a 100% company-owned model, generated an EBITDA margin of around 25% in 2015, before the company was hit by the E. coli virus and margins declined significantly. While this number is higher than Starbucks’ margin figure, Chipotle operates only 2,000 company owned restaurants and the comparative number for Starbucks is around 12,500. This indicates that Starbucks has been able to scale up its restaurants without compromising significantly on margins. Company operated restaurants contribute more than 50% towards Starbucks’ EBITDA, indicating that they are more profitable compared to franchise restaurants since the number of restaurants under both categories are nearly equal.

Capital Intensive Business Model, Affected By Raw Material Price Changes

While restaurants such as McDonald’s and Dunkin’ Brands generate a significant portion of their revenues from franchisee royalties and fees, the profitability of Starbucks’ company-owned restaurants depends on optimization of resources and prices of raw materials. Higher prices of coffee beans, employee’s expenses, and other related costs are likely to impact margins of these restaurants and the company has witnessed a steady decline in the EBITDA margin of these restaurants in the past few years.

This indicates that Starbucks’ model is risky and margins are prone to fluctuations depending on the raw material costs. Further, the company’s model is also capital intensive as it needs significant investment to open a new company-owned restaurant, rather than granting a franchisee license. The company needs more investment for growth under this model.

While the franchise-based model is less risky and more profitable in the long term, we believe Starbucks is not likely to move towards a 100% franchised model in the near future. The company is growing with a combination of company-owned and franchised restaurants and its company-owned restaurants are profitable – generating higher margins compared to its peers. The company’s management is focused on ensuring that the company culture is maintained in the key locations where it operates its own restaurants and this strategy is crucial for the company’s brand value and growth in the long term.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap | More Trefis Research

Like our charts? Embed them in your own posts using the Trefis WordPress Plugin.