Starbucks Disappoints As U.S. Comp Sales Fail To Recover, But Gives Positive Outlook

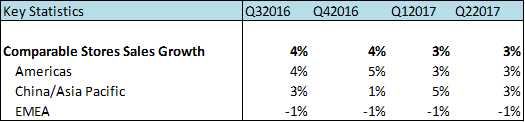

Starbucks (NYSE:SBUX) reported its Q2 2017 results on April 27th and while its earnings per share (EPS) met analyst expectations, revenues missed expectations for the second quarter in a row. Global comparable sales increased by 3% against a consensus estimate of 3.7%. While the success of its Mobile Order and Pay system is causing congestion at its stores, impacting comp sales, Starbucks believes that an engaging digital and mobile relationship with customers will be a key pillar for growth in the long term. The company’s measures to reduce congestion due to mobile orders have started showing results since March. U.S. comp sales increased 4% in March and the company believes that this will accelerate in the future, leading to a stronger second half.

Revenue growth for this quarter was driven primarily by incremental revenues generated from the opening of 2,240 net new stores in the past 12 months and the 3% increase in global comparable sales. The company’s operating margin increased by 40 basis points in this quarter primarily due to sales leverage

- Down 7% Since 2023, Can Starbucks’ Stock Reverse This Trend Post Q1 Results?

- Down 26% From Its Pre-Inflation Shock High, What Is Next For Starbucks Stock?

- After 6% Drop This Year, Pricing Growth To Bolster Starbucks’ Q4

- Can Starbucks Stock Return To Pre-Inflation Shock Highs?

- Starbucks’ Stock To See Little Movement Past Q3?

- Starbucks Stock To Likely Trade Lower Post Q2

The growth in comp sales was primarily due to an increase in average ticket size, offset by a decline in transactions. The EMEA region was an exception, where transactions remained flat but ticket size declined, leading to a decrease in comps.

In order to drive comp sales in the U.S., the company is introducing a new digital order manager (DOM). This system will provide baristas with better visibility on all incoming orders enabling better tracking and real-time order production management. The company is also looking to selective add labor in its busiest stores at peak times to handle the congestion.

China remains a key pillar of Starbucks’ growth. In Q2 2017, comps in China accelerated by 7% which were driven primarily by a growth in transactions as the company continues its aggressive expansion in the region. The company’s strategic partnership with Tencent, offering WeChat as a digital payment option, has been successful and nearly 30% of payments are being tendered from this option. (Read Here’s How A Partnership With WeChat Can Drive Revenues For Starbucks In China). Social gifting is another initiative the company is experimenting with in China, and this is likely to drive growth in the region in the coming quarters.

EMEA continues to be a weak spot with a 14% decline in revenues in Q2. However, if the impact of transfer of the company’s German business to a licensed partner is normalized and adjustments for portfolio shifts and foreign exchange are made, EMEA revenues grew by 6%.

The channel development segment, comprised of the company’s Consumer Packaged Goods (CPG) and Food Service business, reported flat revenue growth in Q2 2017. This was due to an unfavorable revenue deduction adjustment pertaining to prior periods. Excluding this adjustment, the segment reported a 5% increase in revenues.

Going Forward

- Starbucks’ reward program is showing significant traction. In Q2 2107, the company saw 8% growth in average spend per active reward member – the highest growth over a prior year ever. The company is working on several initiatives to leverage this program, which include personalized service, social gifting and using these rewards outside Starbucks.

- The company expects strong revenue growth in the second half of 2017, including accelerated U.S. comp and mid-single digit comp growth.

- Starbucks Reserve remains at the center of the company’s innovation strategy to create experiential retail destinations and several of these stores are under construction globally.

- The company has raised its EPS guidance for the next quarters as it accelerates investments in its Roastery, Reserve and Princi businesses and digital initiatives.

For more details, see our complete analysis for Starbucks

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap | More Trefis Research

Like our charts? Embed them in your own posts using the Trefis WordPress Plugin.