Here’s Why The Recent 180% Rally In Roku’s Stock Does Not Make Sense

Roku’s stock (NASDAQ: ROKU) lost more than 53% of its value when it dropped from over $135 at the beginning of 2020 to less than $65 in March 2020 due to the Covid-19 outbreak and the resultant lockdown, which led to expectations of economic slowdown and lower consumer spending power. Since then, the company’s stock has seen a spectacular recovery of 180% over the last 5 months, with it currently standing over $180 per share. The recovery was led by the multi-billion-dollar Fed stimulus announcement which provided a floor to the stock price and strong financial results in the first half of the year. Roku’s stock went up more than 20% in the last one week with analysts initiating coverage with a buy rating and a few existing ones revising their outlook considering the strong demand for the company’s offerings. With the stock currently more than 30% above its level at the beginning of 2020, is the recent price rise really warranted? We believe that the market is exuberant with Roku’s stock having most likely surpassed its near-term potential.

Where Is Roku’s Stock Headed?

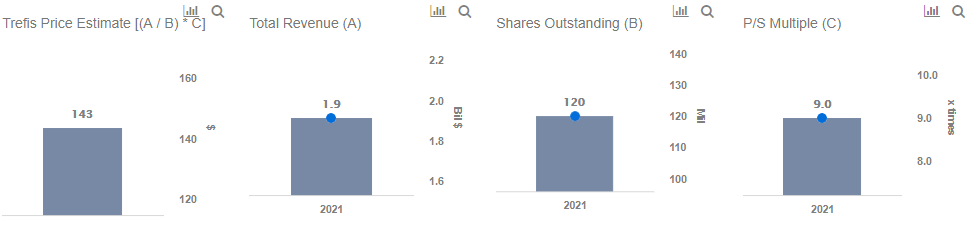

As per Trefis, Roku’s valuation works out to $143 per share which signifies that the stock could potentially decline more than 20% from here. The trigger is the possibility of re-imposition of lockdowns following the recent spike in covid-positive cases in the US. In such a scenario, the company’s ad revenue is expected to take a considerable hit. Though the current pandemic has been a boon for the streaming players due to home confinement of people, it has proved to be a double-edged sword for Roku as the increase in streaming hours has been offset by the lower spending by advertisers due to their finances being adversely affected.

- Down 37% This Year, Will Roku Stock Recover Following Q1 Results?

- Roku Stock Gained 56% Over The Last Three Months, Will It Rise Further Following Q4 Results?

- Up 40% Over The Last Week, Will Roku Stock Continue Its Strong Run?

- Roku Stock Up 50% This Year, Will It Rise Further Following Q3 Results?

- Will Cost Cuts, Improving Growth Continue To Power The Roku Stock Rally?

- Is Roku Stock A Buy Following Strong Q2 Results?

This was reflected in the Q2 2020 results where Roku’s revenues increased 42% y-o-y mainly due to increase in streaming hours, which soared 65% over Q2 2019 to 14.6 billion during the quarter. But Roku does not earn money just by selling its streaming devices; in fact, advertising on its TV operating system and Roku Channel forms a significant chunk of its revenue. Though advertising revenue also increased on a y-o-y basis in Q2 2020, this was mainly driven by the acquisition of Dataxu Inc, a demand-side platform (DSP) company that enables marketers to plan and buy video advertising campaigns. At the same time, advertising spend from other verticals have taken a hit during the pandemic. Coming to profitability, Roku’s saw deterioration in its profits as earnings dropped sharply from -$0.08/share in Q2 2019 to -$0.35/share in Q2 2020.

Despite an increase in revenue, the decline in profitability and the recent surge in Covid-positive cases could prove to be major concerns for Roku. Though a second Covid wave and probable re-imposition of lockdown will see continued healthy growth in streaming, but the advertising revenue (ads & commission forms 70% of Roku’s revenues) will continue to be hit as Roku’s ad platform primarily has considerable exposure to brand advertising spend. It also heavily relies on verticals like casual dining, travel, and tourism, which are most affected by the current crisis and are cutting down on ad spend. Additionally, the absence of any management guidance despite half the year behind us could add to this uncertainty around the stock. With many companies entering the streaming war, another challenge for Roku for continuous healthy growth is to team up with newer players. Roku’s recent partnership with Disney+ has been mutually beneficial for Walt Disney as well as Roku, but three new streaming services – HBO Max, Peacock, and Quibi – are not yet available on Roku.

For the full year 2020, total revenue is expected to be around $1.5 billion and once the current crisis abates, revenue is expected to rise to close to $1.9 billion in FY2021. But Roku is expected to report losses in both the years, with its margins in 2020 and 2021 remaining even below its 2019 level. With share count increasing only marginally, revenue per share (RPS) is expected to rise over 60% by 2021 due to higher revenue. Despite the rise in revenue, the P/S multiple is projected to drop (wiping out the gains in RPS) primarily due to the uncertainty surrounding the revival in ad business, with Roku’s management in fact having stated that even if the crisis abates anytime soon, the total advertising spending is not likely to return to pre-Covid levels until sometime in 2021. Pick-up in the ad business (which currently depends on the abatement of the pandemic) is extremely important for Roku as almost 70% of the company’s revenue comes from Ads and Commission. Thus, factors such as (i) rise in Covid-positive cases, (ii) ad business verticals that Roku mainly depends on being severely affected, (iii) Roku’s inability so far to stitch a partnership with any newly launched streaming offerings and (iv) sliding profitability, could lead to a drop in the P/S multiple. RPS of a little less than $16 and P/S multiple of 9x in 2021 suggests that Roku’s fair value works out to $143, thus reflecting a potential downside of more than 20% from its current level.

Take a look at our outlier analysis for Roku, which puts the spotlight on unexpected but possible scenarios and discusses How Roku’s Stock Could Cross $450 and the specifics of Roku stock downside of $30. For further perspective of the streaming world, see how Disney compares with Netflix.

What if you’re looking for a more balanced portfolio instead? Here’s a top-quality portfolio to outperform the market, with over 100% return since 2016, versus 55% for the S&P 500, Comprised of companies with strong revenue growth, healthy profits, lots of cash, and low risk. It has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams