Roku’s Low-Margin Players Business Remains Crucial To Its Growth

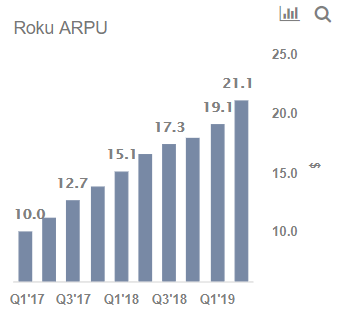

Roku (NASDAQ: ROKU) stock is up 4x this year, driven by the growth of its platform business, which sells ads and distributes streaming video content. While revenues of the platform business have grown at a CAGR of over 100% over the last 3 years, the media players business – which was once Roku’s bread and butter – has been growing at just ~6%. Separately, Roku has been increasingly licensing its operating system (OS) to TV manufacturers for their smart TVs, reducing its dependence on the players business for bringing new customers on to the Roku platform. In this analysis, we take a look at where Roku’s players business stands and what role it could play in Roku’s future.

View our interactive dashboard analysis Why Roku’s Low-Margin Players Business Remains Important To Its Growth

Low Revenue Growth For The Players Segment

- Roku’s hardware revenues have been growing at a CAGR of 6% over the last 3 years, vs. a 100% CAGR for platform revenues.

- We expect growth to slow further in the long-run, due to higher competition from rivals such as Amazon and Google.

- Down 37% This Year, Will Roku Stock Recover Following Q1 Results?

- Roku Stock Gained 56% Over The Last Three Months, Will It Rise Further Following Q4 Results?

- Up 40% Over The Last Week, Will Roku Stock Continue Its Strong Run?

- Roku Stock Up 50% This Year, Will It Rise Further Following Q3 Results?

- Will Cost Cuts, Improving Growth Continue To Power The Roku Stock Rally?

- Is Roku Stock A Buy Following Strong Q2 Results?

Roku Isn’t Making Money On Hardware

- Players gross margins stood at ~11% in 2018, compared to over 70% for the platform division.

- Accounting for other operating expenses, it’s unlikely for the company to be making any money on hardware.

- This is likely because Roku is subsidizing its players to get more people on to its platform – from which it can generate recurring revenues.

We Estimate That Just About 5% of Roku’s Profits Will Come From Players In 2020

Roku’s OS Licensing Business Is Growing Fast, Reducing Dependence On Standalone Player Sales For Adding New Platform Subscribers

- Roku licenses its OS to smart TV manufacturers and this business is gaining traction, with over one-third of smart TVs sold in the U.S. over Q1 2019 being Roku powered.

- The smart TV route might be a more efficient means of platform customer acquisition for Roku, as it only needs to license its OS to manufacturers.

- Smart TV-based Roku platform users could also be more loyal, as TV sets cost several hundreds of dollars and have long replacement cycles (7 to 10 years per IHS Markit).

- In comparison, switching costs for Roku’s streaming hardware is likely to be low, considering its low price points ($30 onward).

Roku Might Still Need To Bank On Its Players To Drive Platform User Growth

- Although the hardware business is unlikely to be accretive to Roku’s earnings or valuation, we believe that it will remain important to the company for the foreseeable future.

- We estimate that the company shipped about 6 million players in 2018. Considering that Roku’s platform user base grew by about 8 million users in 2018, it’s likely that a bulk of the expansion still comes from players.

- Moreover, Roku’s OS licensing is limited to budget and mid-tier TV brands such as TCL, Insignia, and Sharp, meaning that average revenues from these users could be lower. With the Roku streaming hardware, the company could continue to address higher-value customers.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.