Royal Dutch Shell Stock Looks Quite Undervalued

After slashing quarterly dividend by 66% and suspending share buyback program, investors fear that Royal Dutch Shell’s (NYSE: RDS.A) cash preservation initiatives will last for a while amidst the low production environment. While commodity prices remain weak from low transportation and industrial demand, Trefis takes a closer look at profitability and asset distribution across the three segments to analyze Royal Dutch Shell’s valuation. With OPEC+ cuts extended till July, upstream oil companies face regulatory pressure to curtail production further, and the company expects a 40-50% contraction (y-o-y) in oil product sales volume for Q2. Interestingly, the company has not significantly lowered integrated gas and LNG production volumes, which are expected to shrink by 15-20% compared to the prior-year quarter.

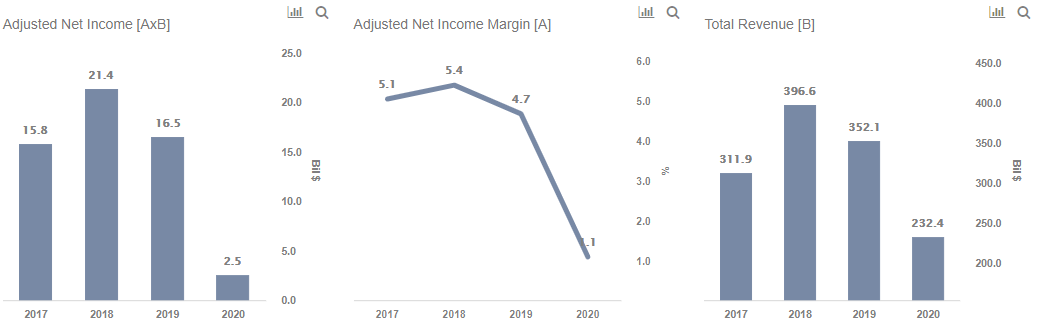

Shell is one of the largest integrated oil majors with $352 billion in annual revenues and 3,665 MBD of oil & gas production. It has three operating segments: Upstream, Downstream, and Integrated Gas.

Integrated Gas segment to support earnings during this phase of low demand for liquid fuels

- In 2019, the integrated gas segment generated $45.6 billion in revenues (including inter-segment sales) with 922 MBD of natural gas and 35.5 million tonnes (nearly 816 MBD) of liquefaction volumes.

- Europe, Asia, Oceania, and North America account for 10%, 27%, 22%, and 20% of natural gas production, respectively.

- Along with the expected contraction in the global economy, natural gas demand to likely shrink by 5% in 2020.

- However, the expanding share of natural gas as an energy source for electricity generation is expected to support Shell’s integrated gas segment’s earnings in the long run.

- In the past three years, Shell has increased the segment’s capital expenditure from $3.5 billion in 2017 to $3.8 billion in 2019, along with a 5% growth in total production.

- On the contrary, the Upstream segment’s capital expenses declined by 10% while production volumes remained flat.

Natural Gas production volumes comparable to liquid fuels

- In 2019, Shell’s total production stood at 3,665 MBD, including 1,876 MBD of crude oil and 1,790 MBD of natural gas.

- Considering intersegment sales, the $46 billion of Upstream revenues (majorly liquid fuels) are comparable to the $45 billion of Integrated Gas revenues, which includes LNG sales and the new energy portfolio.

- More so, the integrated gas segment commands a 45% share of the total earnings with a 21% net margin.

- Despite the near-term shock from the coronavirus crisis, the growing demand for natural gas is likely to support the company’s earnings and shareholder returns in the long-run.

- Thus, we estimate Royal Dutch Shell’s stock valuation to be around $51 per share – which is 50% above the current market price.

As oil producers and service providers face the coronavirus storm, which S&P 500 component stocks have the best chance of outperforming the benchmark index? Our 5 In the S&P 500 That’ll Beat The Index: TWTR, ISRG, NFLX, NOW, V look promising.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams