P&G’s Q2 Earnings To Benefit From Operating Efficiency But Strong Currency Headwinds Likely To Hit Topline

With the world’s leading brands such as Pampers, Tide and Head & Shoulders, Procter & Gamble (NYSE:PG) is all set to release its Q2’17 earnings on January 20th. (Fiscal years ends with June.) In Q1, the improved operating margin led P&G to outperform its peers by earning 5 cents per share more than what analysts had expected. P&G was one of the very few consumer companies whose organic revenue grew and the net revenues managed to remain flat, which can be attributed to the better focus on its leading brands. Prior to that, P&G’s net sales declined year over year both in the March and June quarters which were affected by the currency headwinds that continued on from 2015 into 2016.

In Q2’17, P&G continued to focus on its operational efficiency to further enhance the performance of its bottom-line. The two major takeaways from the quarter ended in December which would likely have an impact on P&G’s Q2 results are:

- The completion of merger of special beauty brands with Coty

- Continued cuts in advertising and overhead costs

While the above mentioned factors are expected to benefit P&G, the currency headwinds and a diminished consumer demand will partially act as a drag on its earnings.

- Is Procter & Gamble Stock Appropriately Priced At $160?

- Should You Pick Procter & Gamble Stock At $155 After A Mixed Q2?

- Is Procter & Gamble Stock Fully Valued At $150?

- Will Procter & Gamble Stock Continue To Rise After 27% Gains In The Ongoing Inflation Shock?

- Should You Buy TMUS Over Procter & Gamble Stock For Better Returns?

- Should You Buy Colgate-Palmolive Stock At $80?

See our complete analysis for Procter & Gamble

P&G is 41 Brands Lighter. Will It Help The Company Post Better Results?

In October, P&G completed the merger of 41 of its beauty brands with Coty in a deal valued at $12.5 billion. Some of these brands include Wella, Clairol, Gucci, Lacoste, Covergirl and Boss. Now that P&G is a lot leaner, its revenues will take a hit as the beauty brands which have been divested had a combined revenue of almost $9 billion (FY2015). Due to the reduction in share count as well, it will not affect the earnings per share of the company drastically. On the other hand, this divestiture might benefit the operating efficiency of the company in two ways:

- P&G is likely to focus and direct its marketing and product development expenses towards its signature household brand names such as Tide, Pampers and Head & Shoulders. As the company expects its competition to grow, the new products will help the company in maintaining its market share, in our view. Some examples of its innovative launches in Q2 were Olay Eyes and Pampers’ Swaddler diapers for premature babies.

- With the divestiture of brands, P&G’s workforce has declined significantly. The company was able to reduce its headcount by 25% in the last 5 years and it plans to continue this reduction up till 30%. This means majority of P&G’s workforce now is involved in its top 65 brands. Any further cut in headcount will have benefitted the operating margins of the company in Q2.

Reduction In Advertising And Overhead Costs Will Continue To Help The Bottom-line

- In a recent presentation on P&G’s analyst day, the company announced that it has reduced its non-manufacturing personnel by 25% over the last 5 years. It further plans to cut it to 30% by June 2017. The benefits of any further cuts in enrollments are likely to have trickled down to the bottom-line in Q2.

- In an effort to optimize its marketing thrust, the company has trimmed down its advertising agency costs by $620 million in the last three years, along with reducing the number of agencies it worked with, by 50%.

- In addition, P&G has improved its supply chain by simplifying the networks it uses to deliver the finished products from the manufacturing sites to the end consumer. The long term benefits of these initiatives started showing up in the company’s results in Q1’17, and are likely to blink in Q2 and rest of the year going forward.

Stronger Dollar and Decline in Consumer Demand To Act As Offsetting Factors

- In the three months ended December, the US Dollar index fell by over 7%, which could act as a headwind to the top-line. P&G has already suffered 6% and 5% currency headwinds in FY’16 and FY’15 respectively.

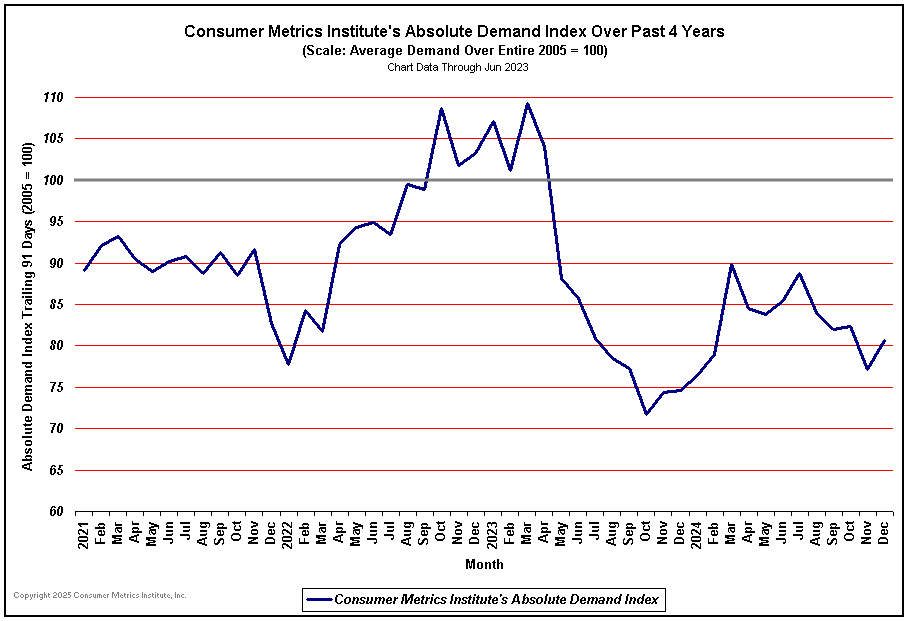

- Apart from that, the trailing 90 day consumer demand index of the US had fallen by around 6% in that quarter, which suggests a tough macro outlook for the top-line growth.

{kind=link}

See More at Trefis | View Interactive Institutional Research (Powered by Trefis)