Here’s Why Frito-Lay North America Is The Most Significant Division For PepsiCo

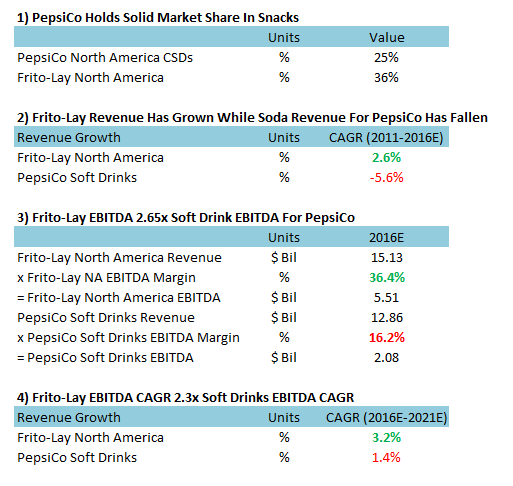

PepsiCo (NYSE:PEP) is mostly associated with carbonated soft drinks (CSD), mainly because of its namesake soda brand Pepsi, and other strong soda brands such as Mountain Dew and Diet Pepsi. However, more than half the revenue for the company comes from its snacks business, including Frito-Lay North America, which, in fact, is the most profitable division of the company, and constitutes ~25% of the net sales.

As customers continue to ditch sugary CSDs for alternative beverage segments, PepsiCo’s dependence on this segment is also decreasing. Only 21% of the company’s net revenue comes from all its soda sales globally, as per our estimate. While soda consumption in the U.S. has declined for eleven consecutive years now, impacting sales for manufacturers such as PepsiCo, Coca-Cola, and Dr Pepper, snack consumption hasn’t been similarly affected. Innovations in this segment in terms of gluten-free products and nutritious variants, and in terms of product packaging, have helped grow sales for the North America savory snacks market at a CAGR of 5% between 2010-2015. As Americans continue their large snacking habit, Trefis estimates this market to grow at 3.1% CAGR between 2015-2020. A little slowdown compared to the previous high growth rate could be due to the continual push for a healthier lifestyle, however, higher consumption from the younger generation is expected to, overall, boost growth.

Here’s why Frito-Lay North America is the most significant division for PepsiCo:

While in CSDs, PepsiCo’s market share is second to Coca-Cola’s much larger ~42% share, the company’s Frito-Lay division holds the number one position in the savory snacks market in North America, followed by Kellogg’s and Mondelez, which have single-digit market shares. Dominance in a category gives PepsiCo more pricing advantage due to a loyal customer base and strong brand awareness.

In addition to higher revenue growth in the last five years, what makes Frito-Lay North America the most significant division for PepsiCo is its high EBITDA margin, which is the largest compared to any other division, and higher expected growth in EBITDA going forward.

Have more questions on PepsiCo? See the links below.

- PepsiCo Earnings Review: Macroeconomic Headwinds Bring Down An Otherwise Strong Core Performance

- PepsiCo: The Year 2015 In Review

- What’s PepsiCo’s Revenue And EBITDA Breakdown?

- What’s PepsiCo’s Fundamental Value Based On Expected 2016 Results?

- By What Percentage Have PepsiCo’s Revenues And EBITDA Grown Over The Last Five Years?

- Where Will PepsiCo’s Revenue And EBITDA Growth Come From Over The Next Three Years?

- How Has PepsiCo’s Revenue And EBITDA Composition Changed Over 2012-2016E?

- Why Snacks Are More Valuable Than Carbonated Drinks For PepsiCo

- Why Carbonated Soft Drinks Will Contribute Relatively Lower To PepsiCo’s Drinks Business

Notes:

- Will PepsiCo Beat The Consensus In Q1?

- What’s Next For Pepsi Stock After A Mixed Q4 And 6% Fall Last Year?

- After A 25% Fall In 2023 Is Campbell A Better Pick Than PepsiCo Stock?

- What’s Next For PepsiCo Stock After A Q3 Beat?

- What To Expect From PepsiCo’s Q3?

- Which Is A Better Pick – PepsiCo Stock Or Amgen?

See More at Trefis | View Interactive Institutional Research (Powered by Trefis)