What Is Oracle’s Near-Term Outlook?

Oracle‘s (NYSE:ORCL) fiscal first quarter results beat market expectations on EPS, while missing on revenue. Management’s focus on its Gen 2 Cloud and Autonomous Database was again highlighted during the company’s financial analyst day in October. While management admits that it may be early days to gauge the performance of the company’s architectural revolution (Gen 2 Cloud), incremental traction in Oracle’s customer base moving to Gen 2 could be a huge positive for the company.

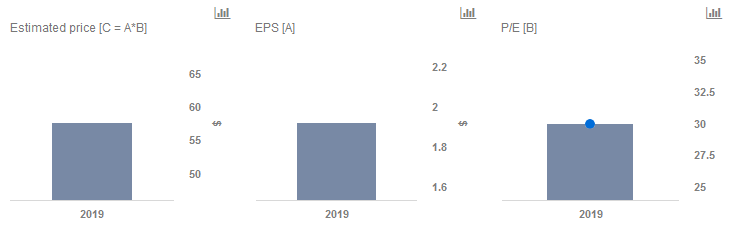

We currently have a price estimate of $58 per share for Oracle, which is around 20% higher than the current market price. Our interactive dashboard on Oracle’s Price Estimate outlines our forecasts and estimates for the company. You can modify any of the key drivers to visualize the impact of changes on its valuation.

What To Expect Moving Forward

Per Oracle’s management, the Q1 revenue miss was primarily due to forex headwinds and the company was actually able to beat its own targets. Furthermore, the board increased the share repurchase authorization to $20 billion.

Management also noted that Oracle continues to win customers by displacing competing products on the ERP side. On the Oracle Cloud Infrastructure (OCI) adoption, management noted that early indicators such as ISV adoption have been positive. Even on Autonomous Database Cloud (ADC), management claims that existing customers are slowly dipping their feet in, and the surprising success they have seen is likely to drive a rapid migration to the Oracle cloud from on-premise.

Larry Ellison, the company’s Chairman and CTO, further spoke about the USPs of Gen 2 Cloud and Autonomous Database during Oracle’s analyst day in October. He stated the current breed of cloud infrastructures cannot ensure security for enterprise customers. Oracle’s Gen 2 Cloud provides security leveraging its radically different architecture, which separates cloud control from user code. While at an access level even Oracle will not be able to access customer data without permission, from a security standpoint automated security measures will ensure threats are quarantined before they can spread. Ellison also discussed at length the lower cost and higher performance that OCI can offer versus industry leader AWS.

Fiscal Q2 will be an important quarter for Oracle, since the results are likely to build on management’s assertions. We will be looking for color on the velocity of adoption of OCI and ADC across Oracle’s existing customers and against competition. If Oracle can execute on the vision laid out during its investor day, management’s belief that “it seems like an amazing deal to buy our stock” could turn out to be prescient.

Do not agree with our forecast? Create your own price forecast for Oracle by changing the base inputs (blue dots) on our interactive dashboard.

Like our charts? Explore example interactive dashboards and create your own.