What’s Happening with Netflix Stock?

[7/20/2020] Netflix Stock Drops On Weak Q3 Subscriber Guidance

Netflix stock (NYSE:NFLX) fell by about 13% over the last week – declining from about $569 to around $493 – as the company published its Q2 earnings and guided lower-than-expected subscriber adds for the third quarter. Sure, the drop is sizeable, but let’s step back a bit: Netflix stock is still up by about 50% year-to-date. So what’s really happening with Netflix?

Netflix added a stronger-than-expected 10.1 million subscribers in Q2 (versus its guidance of 7.5 million adds), as the Covid-19 pandemic and continued lockdowns helped the company maintain momentum. However, Netflix has guided just 2.5 million net subscribers adds for Q3, well below analysts’ expectations and also below the 6.7 million subscribers it added in Q3 2019 [1]. In fact, this is lower than the 2.7 million subscribers it added in Q2 2019.

- Up 27% Year To Date, Will Q1 Results Drive Netflix Stock Higher?

- Netflix On A Roll As It Benefits From Paid Sharing And Ads. Is The Stock Undervalued At $610?

- Up 50% Over Last Year, Will Q4 Earnings Drive Netflix Stock Higher?

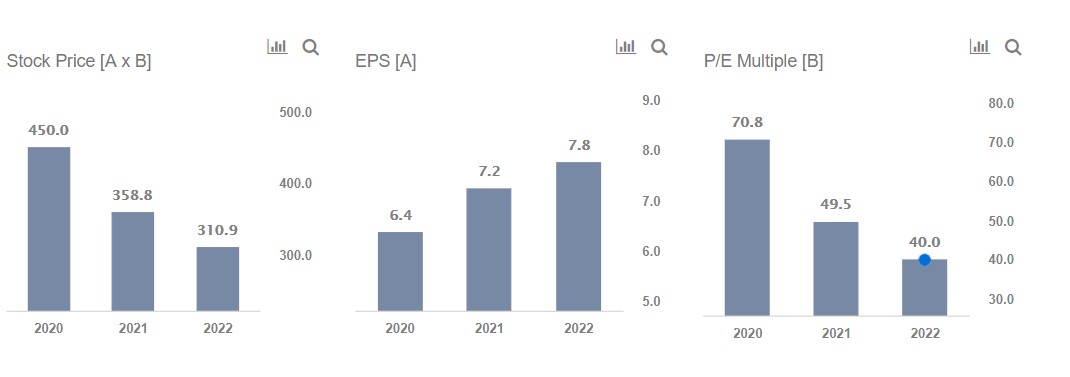

- Will Netflix Stock Rally 40% To Return To Pre-Inflation Shock Highs?

- How Will The Password Sharing Crackdown Help Netflix Q3 Results?

- Will Netflix Stock Return To Pre-Inflation Shock Highs Of Over $650?

To be fair, the company has been hinting since its Q1 results that growth in this closely-tracked metric could remain subdued over the next few quarters as it was seeing a pull-forward of subscribers, with people who would have likely subscribed over the second half of the year subscribing to the streaming service earlier than expected due to the outbreak.

So why is the stock reacting so strongly to muted subscriber guidance?

Investors Less Forgiving About Subscribers Misses As Pricing Remains Challenge

Netflix’s cash spending on content is soaring – the company was projected to spend $17 billion on content over 2020. While Covid-19 is likely to slow this down temporarily, cash spends on content per subscriber have been rising steadily. The only way Netflix can fund this is by either boosting prices or by adding more subscribers. While Steaming ARPU (adjusted for foreign exchange impacts) grew 5% year-over-year in Q2 thanks to the price increases in 2019, mounting competition means that Netflix will have its hands tied when it comes to price increases in the near- to medium-term. For example, Disney and Apple have priced their streaming services very competitively at $7 and $5 per month in the U.S. compared to $13 for Netflix’s most popular plan.

This likely means that investors still count subscribers adds as the most significant lever of Netflix’s valuation – explaining the sharp sell-off over the weak guidance for this metric in the next quarter.

Did you know that Netflix market cap recently edged past media behemoth, Disney? Which is the better bet? Find out more in our analysis Disney vs. Netflix: Does The Stock Price Movement Make Sense?

[6/24/2020] Netflix Pricing And Margins Risk

Netflix (NASDAQ:NFLX) has moved the price lever enviably not just once but twice over the last three years. The company raised pricing on its most popular plan from $10 to $11 in 2017 and once again to $13 in early 2019. This was the key reason behind the company’s net earnings margin (profits after all expenses as a fraction of sales) expanding from about 2% in 2016 to over 9% in 2019. However, there is a significant risk that this golden lever could be gone for some time. In this analysis, we look at the price lever in the context of Netflix’s key challenge of managing cash content costs.

As a follow-up to our upside case for how Netflix Stock could climb 2x, we outline a downside scenario that could see Netflix stock drop by almost 50% from current levels if its pricing power is reduced and margin growth stalls. Find out more in our dashboard Netflix Downside Scenario: Headed Back To $250?

3 Facts

Let’s look at 3 facts to understand our downside risk view of Netflix:

- Fact 1: $82 of Netflix cash content cost per subscriber in 2019, up from $62 in 2015

- Fact 2: $112 of Netflix annual average revenue per subscriber in 2019, up from $95 in 2017

- Fact 3: $84 for Disney, and $60 for Apple’s revenue per subscriber in 2020

The only way to sustain the $112 in annual ARPU is to keep plowing on #1 – content costs – faster than the giants Apple, Disney, and Amazon

Disney+, Apple TV+ and Others Turn Up The Heat With Lower Pricing

Overall, we think it’s unlikely that Netflix will be able to increase U.S. pricing in the near-to-medium term, with competition in the streaming space heating up. Giants such as Disney, Apple, and Amazon continue to barrel forward, strengthening and doubling down on free or cheaper video offerings. For perspective:

- Disney+ is priced at an attractive $7 per month price and offers a formidable library of legacy content besides a growing library of original programming.

- Apple’s new service ($5 per month) is offered for free for a year with the purchase of a new Apple device. The personal computing behemoth is also investing significantly in content, with plans to spend about $6 billion on its initial lineup of TV shows. [2]

- Amazon – the largest player in terms of household penetration – has also been steadily improving its value proposition, bundling more offers to its Prime subscription.

Why Price Increases Are Important To Netflix

Netflix’s content costs are rising fast, with cash spending on content growing from $9 billion in 2017 to $14.6 billion in 2020, and this has meant that Netflix has been burning through an increasing amount of free cash. On the other hand, subscriber growth has been slowing, particularly in North America. This means that Netflix’s cash spent on content per subscriber has risen from $76 in 2017 to $82 in 2019, and the company needs to boost pricing to justify this. Sure, the coronavirus pandemic could temporarily change this dynamic, as subscriber adds over Q1 2020 jumped due to stay-home orders, while content production likely slows down. But the general trend of higher content spends is likely to remain intact, given that Netflix was projected to spend over $17 billion on content in 2020, with management also hinting at subdued subscriber growth in the next few quarters. [3]

Streaming Not A Zero-Sum Game, But Investors Could Rethink Valuation If Earnings Slow

While the streaming space is not a zero-sum game, with users often opting for multiple services at a time, the new competitive landscape gives Netflix much less leverage with respect to pricing. After all, Netflix U.S. subscriber adds dropped about 70% year-over-year to just 0.55 million in Q4 2019 – the quarter in which Disney and Apple launched their new services. In addition, Netflix stock is quite volatile and reacts sharply to the news. If subscriber growth were to falter and look weak post-Covid, for example in 2021, it’s possible that smaller revenue growth for one or two quarters with continued growth in content costs help conjure scenarios of EPS flattening which can result in Netflix’s valuation multiple dropping from levels of around 70x forward earnings presently, to about 50x by 2021. The stock has dropped by 15% to 20% multiple times in the past, as we outline in our analysis How Has Netflix Stock Reacted To Earnings Shocks In The Past? If investors gauge that this is going to be a more secular trend, its possible that the multiple could fall further and remain depressed, as we spell out in our interactive analysis Netflix Downside Scenario: Headed Back To $250?

Are There Any Other Options For Netflix To Boost Growth?

Netflix has executed masterfully in international markets, where there is still room to improve penetration. The company’s international subscriber base stood at just 112 million vs. 69 million in North America as of Q1 2020, and its increasing focus on regional content should help it sign on new subscribers. However, customers in many of these markets are much more price-sensitive, and this could prove a challenging trade-off from a margins standpoint.

Disney stock is down by over 20% year-to-date compared to Netflix, which is up by 35%. Which is the better bet? Find out more in our analysis Disney vs. Netflix: Does The Stock Price Movement Make Sense?

[6/16/2020] How Netflix Stock Can Double

Is Netflix’s stock (NASDAQ: NFLX) pricey, trading at about 100x trailing earnings? Not at all. Especially if you consider the fact that the earnings could be about 4x the current level in the next few years. How is that? Firstly, we believe that Netflix revenues can double by 2025 to levels of about $45 billion from about $20 billion in 2019 and an estimated $24.5 billion in 2020, representing a growth rate of almost 15% per year (for context annual growth was about 30% over the last two years). Netflix’s international streaming business has managed excellent entry into more than 190 countries and is likely to follow the expansion playbook the streaming giant has executed so well in the U.S and Canada. Sure, revenue growth could be still higher if the Coronavirus pandemic causes a permanent shift in content consumption patterns and potentially gives Netflix better pricing power, but 2x growth in the top line over the next five years looks quite achievable as a base case.

Combine revenue growth with the fact that Netflix’s margins (net income, or profits after all expenses and taxes, calculated as a percent of revenues) are on an improving trajectory – they grew from roughly 2% in 2015 to over 9% in 2019. Netflix’s larger content-producing peers like Disney have margins around 14% and we see Netflix margins could reach and potentially exceed these levels going forward, doubling to about 18% by 2025. Why is this possible? Netflix has lower costs of customer acquisition and distribution, and fixed costs such as content amortization will be better absorbed as revenues scale-up. So is 4x growth in earnings possible in the next five years? Yes. Looks very reasonable when you combine 2x revenue growth with the 2x growth that’s possible in Netflix’s margins.

Now if earnings grow 4x, the P/E multiple will shrink to 1/4th its current level, assuming the stock price stays the same. But that’s exactly what Netflix investors are betting will not happen! If earnings expand 4-fold over the next few years, instead of P/E shrinking from around 100x now to about 25x, a scenario where the P/E metric stays at about 45x or even 50x looks more likely. For perspective, the broader entertainment sector traded at a trailing multiple of 48x prior to the Coronavirus crisis and it’s safe to assume that Netflix will trade at least at these levels. [4] This would make a roughly 2x growth in Netflix’s stock price a real possibility in the coming years.

So yes, Netflix could, in fact, be considered to be a good buy right now – with a word of caution. Investors must evaluate Netflix’s cash flows in contrast to earnings.

What about the 5-year time horizon for our scenario? In practice, it won’t really make much difference whether it takes 3 years or 5. As long as Netflix is on this revenue and margins expansion trajectory, the stock price will likely respond in a similar way.

Separately, what if earning margins land at close to 14% or 15% instead of the 18% we estimate? We believe this risk is balanced by the upside to our 15% revenue growth estimate to come in closer to 20% or even higher given that Netflix’s history of execution in international markets resulted in about 30% growth in the last few years.

Is Netflix stock a better buy than software titan Microsoft? Our dashboard Netflix vs. Microsoft: Does The Stock Price Movement Make Sense? has the underlying numbers.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Notes:- Q2 2020 Investor Letter, Netflix [↩]

- Apple splashes $6bn on new shows in streaming wars, Financial Times, August 2019 [↩]

- Netflix will spend over $17 billion on content in 2020: Analyst, Fortune, January 2020 [↩]

- PE Ratio by Sector, NYU Stern, January 2020 [↩]