Does Netflix Have A Path To A $250 Billion Market Cap?

Netflix‘s (NASDAQ: NFLX) stock has surged from around $131 in January 2017 to over $275 currently, translating into a market cap increase of over $60 billion ($55 billion to nearly $120 billion currently). The company’s stock has remained fairly volatile, and fluctuated between $201 to $415 over the course of 2018. In this note, we take a look at what it would take for the company to hit a $250 billion market cap going forward.

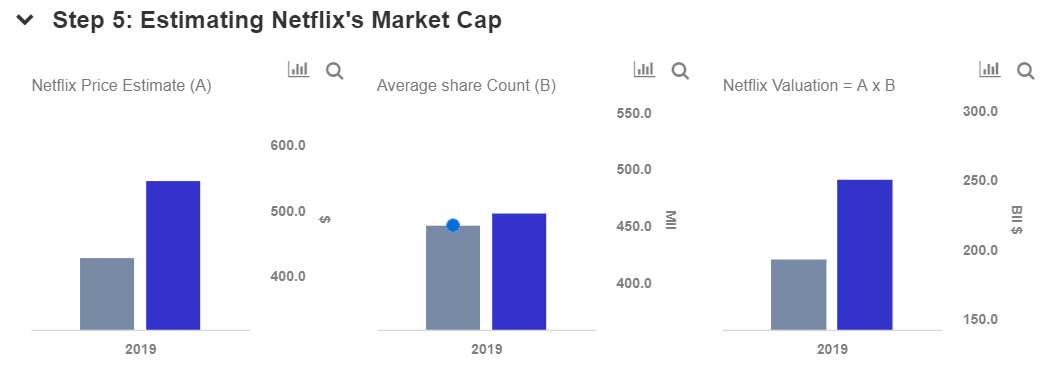

We have created an interactive dashboard analysis with Netflix’s base-case valuation (shown in gray in the below charts). We have included some key value drivers for the company including its total memberships, monthly fee per subscriber, net income margin, average share count and a P/E multiple (based on 2019 revenue) in this dashboard. We have also provided with a scenario (shown in blue) which explores how the company could justify a higher valuation of $250 billion. We have maintained our long-term price estimate for Netflix at $376, which is almost 30% ahead of the current market price and is driven by the company’s strong foothold in the streaming business as well as a robust lineup of TV shows and films.

- Up 27% Year To Date, Will Q1 Results Drive Netflix Stock Higher?

- Netflix On A Roll As It Benefits From Paid Sharing And Ads. Is The Stock Undervalued At $610?

- Up 50% Over Last Year, Will Q4 Earnings Drive Netflix Stock Higher?

- Will Netflix Stock Rally 40% To Return To Pre-Inflation Shock Highs?

- How Will The Password Sharing Crackdown Help Netflix Q3 Results?

- Will Netflix Stock Return To Pre-Inflation Shock Highs Of Over $650?

We expect Netflix to generate around $15.8 billion in revenues for full-year 2018, and earnings of over $1.2 billion. Our revenue forecast represents a year-on-year growth of over 30%. Of the total expected revenues in 2018, we estimate $7.3 billion in the Domestic Streaming business, over $8 billion for the International Streaming business, and nearly $400 million for the Domestic DVD business. Further, we expect the company to grow further and reach $18.4 billion in revenues for 2019. Our bull case assumes that the company’s total revenue could rise to $21 billion in 2019.

Domestic Streaming Subscriptions Continue To Grow

Netflix’s domestic revenues have grown from $3.4 billion in 2014 to $6.1 billion in fiscal 2017, primarily due to growth in the average number of paid memberships, as well as an increase in the average monthly revenue per paying membership. The streaming giant currently has 58 million domestic customers, and this growth has slowed in recent quarters – largely due to the saturation of the U.S. market in terms of Netflix’s penetration. However, there are an estimated untapped 80 million U.S. adults who can access the internet but do not have Netflix, and could be further added to the company’s subscriber base. Currently, we project Netflix’s domestic subscribers to reach nearly 61.7 million by the end of 2019, translating into revenues of $8.1 billion. Our assumption is based on the fact that the company is spending a significant portion of its content budget on original shows. The company already has a long-term goal of ensuring that nearly 50% of the content streamed on its platform is original. In our bull case scenario, we estimate that the number of domestic subscribers and monthly fees could increase further due to healthy subscriber growth. This would lead to improved cash flows and could, in turn, allow Netflix to invest further in content. Cumulatively, this growth in revenues would lead to an upside of $3 billion, or over $6 per share, to our existing valuation estimate.

International Streaming Subscriptions To Power Valuation

Netflix has been growing its international subscribers at an annual rate of nearly 40% over the last two years, leveraging its original content slate and the growth in streaming. While in our base case scenario, we project revenues to grow to $8.1 billion in 2018 and $9.9 billion in 2019, increased international market penetration could boost the revenues for the division even further to $12 billion. In this scenario, the number of subscribers would have to increase as much as 22% from our base case in 2019. This change would result in an upside of $25 billion, or $55 per share to the company’s valuation.

In addition to the above upside scenarios, our net income margin estimate in this scenario was increased from $8% to 9.1%. This translates into net income of nearly $2 billion in 2019, up from $1.5 billion in our base case. The average share count of 460 million gives us earnings per share of $4.19, up from our previous estimate of $3.29. Overall, these upside case estimates result in a price estimate of $544 ($250 billion market cap).

The above bull case scenario does seem relatively unlikely, given the mounting competition – which is expected to intensify once Disney launches its own direct-to-consumer offering (Disney+) and pulls its content from Netflix in 2019. Nevertheless, the stock markets are often momentum-driven, and if Netflix launches more popular content and manages to grow its subscriber base globally, there could be a possibility of a significant rally in its valuation.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.