Here’s A Better Pharmaceutical Pick Over Merck Stock

We think that Bristol Myers Squibb stock (NYSE: BMY) currently is a better pick compared to its industry peer, Merck stock (NYSE: MRK), given its better growth prospects and comparatively lower valuation, with its stock trading at 3.0x trailing revenues, compared to 3.6x for MRK stock. That said, this gap in valuation is also justified given Merck’s better profitability. However, looking at future prospects, we believe that Bristol Myers Squibb will outperform Merck, as we discuss in the sections below. We compare a slew of factors such as historical revenue growth, returns, and valuation multiple in an interactive dashboard analysis Merck vs Bristol Myers Squibb: Which Stock Is A Better Bet? Parts of the analysis are summarized below.

1. Bristol Myers Squibb’s Revenue Growth Is Stronger

- Merck’s sales have jumped from $39.8 billion in 2016 to $54.1 billion over the last twelve months, while Bristol Myers Squibb’s revenues have surged from $19.4 billion to $45.5 billion over the same period, primarily reflecting the impact of its Celgene acquisition in 2019.

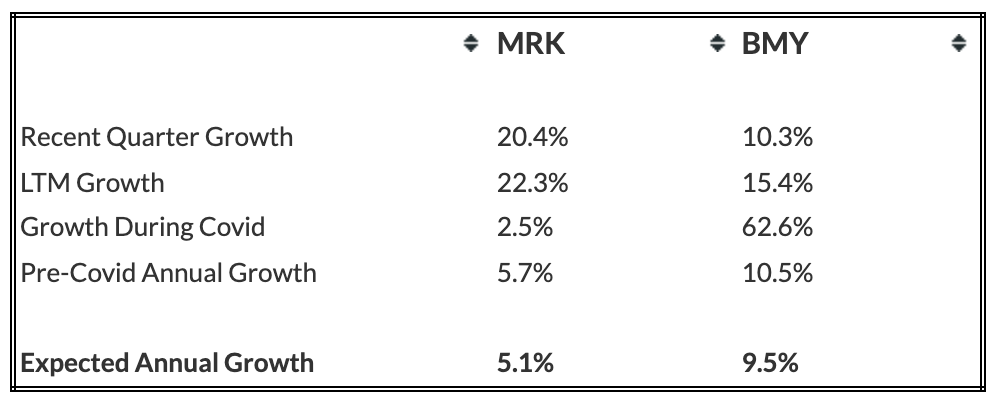

- However, Merck’s revenue growth of 22% over the last twelve month period was higher than the 15% growth for Bristol Myers Squibb, given continued uptick in Keytruda sales with its label expansion and a rebound in demand for vaccines, including Gardasil, after a fall in 2020, due to the impact of the pandemic.

- Looking at a slightly longer time frame, both the companies have seen a rise in sales. That said, Bristol Myers Squibb’s last three-year revenue CAGR of 29%, aided by the Celgene acquisition, compares with a 6% CAGR for Merck.

- Looking forward, with economies now opening up, the demand for pharmaceuticals is likely to remain high in the near term, boding well for revenue growth of both the companies. Our Merck Revenue and Bristol Myers Squibb Revenue dashboards provides more insight on the companies’ revenues.

- Bristol Myers Squibb’s revenue is expected to grow at a faster pace compared to Merck. The table below summarizes our revenue expectation for MRK and BMY over the next three years, and points to a CAGR of 9.5% for Bristol Myers Squibb, compared to a CAGR of 5.1% for Merck.

- Note that we have different methodologies for companies negatively impacted by Covid, and for companies not impacted or positively impacted by Covid while forecasting future revenues. For companies negatively impacted by Covid, we consider quarterly revenue recovery trajectory to forecast recovery to pre-Covid revenue run rate, and beyond the recovery point, we apply average annual growth observed in three years prior to Covid to simulate return to normal conditions. For companies registering positive revenue growth during Covid, we consider average annual growth prior to Covid with certain weight to growth during Covid and the last twelve months.

- After A 30% Fall In A Year Is Pfizer Stock A Better Pick Over Merck?

- At $100 Does Merck Stock Have Room For Growth?

- Should You Pick Merck Stock Over Coca-Cola?

- Should You Buy Merck Stock After An Upbeat Q2?

- How Has Merck Stock Performed During The 2022-23 Inflation Shock?

- Is Merck Stock A Better Pick Over ABBV?

2. Merck Is Also More Profitable And It Has A Better Debt Position

- Merck’s operating margin of 18% over the last twelve month period is much better than -16% for Bristol Myers Squibb.

- Furthermore, if we were to look at the recent margin growth, both of the companies have seen negative growth, with last twelve month vs last three year margin change at -2.6% for Merck, compared to a large -23.6% change for Bristol Myers Squibb.

- Note that Bristol Myers Squibb margins over the last twelve month period were negatively impacted due to a one-time in-process R&D charge of $11.4 billion arising from its MyoKardia acquisition. Bristol Myers Squibb’s operating margin figure stood at 19% for the nine months period ending Sep 2021, still lower compared to around 25% for Merck.

- Looking at financial risk, Merck’s 14% debt as a percentage of equity is lower than 32% for Bristol Myers Squibb, while the latter’s 14% cash as a percentage of assets is higher than the 11% for Merck, implying that MRK has a better debt position, but BMY stock has a better cash position.

3. The Net of It All

- We see that the revenue growth over the recent quarters has been stronger for Merck and it is more profitable compared to Bristol Myers Squibb. That said, BMY has a better cash position and it is trading at a comparatively lower valuation.

- Bristol Myers Squibb has recently announced a 10% increase in its quarterly dividend, and that it is boosting its share repurchase program by $15 billion, implying better than earlier anticipated earnings growth over the coming years.

- Now, looking at future prospects, using P/S as a base, due to high fluctuations in P/E and P/EBIT, we believe BMY is the better choice of the two. The table below summarizes our revenue and return expectation for MRK and BMY over the next three years, and points to an expected return of 30% for BMY over this period vs. 24% for MRK, implying that both the stocks are likely to offer good returns going forward. But if one has to choose between the two, investors are better off buying BMY over MRK, in our view. Our dashboard Merck vs Bristol Myers Squibb has more details on how we arrive at these numbers.

- Note that Covid-19 is proving more difficult to contain than initially thought, due to the spread of more contagious virus variants and infections in many geographies, including the U.S. and Europe, are higher than what they were a few months back. The concerns around Omicron have spooked the markets at large. If this recent large spike in Covid-19 cases from the new variant that we are witnessing now, results in a disruption in healthcare services, it is likely to impact the sales growth of both, Merck and Bristol Myers Squibb.

While MRK and BMY stock may see higher levels, the Covid-19 crisis has created many pricing discontinuities which can offer attractive trading opportunities. For example, you’ll be surprised how counter-intuitive the stock valuation is for Xylem vs. Merck.

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio that’s beaten the market consistently since the end of 2016.

| Returns | Jan 2022 MTD [1] |

2022 YTD [1] |

2017-22 Total [2] |

| MRK Return | 5% | 5% | 36% |

| BMY Return | 1% | 1% | 8% |

| S&P 500 Return | -2% | -2% | 109% |

| Trefis MS Portfolio Return | -6% | -6% | 271% |

[1] Month-to-date and year-to-date as of 1/10/2022

[2] Cumulative total returns since the end of 2016

Invest with Trefis Market Beating Portfolios