This Healthcare Company Is Likely To Offer Better Returns Over 3M Stock

We think that Thermo Fisher Scientific stock (NYSE: TMO) currently is a better pick compared to 3M stock (NYSE: MMM), despite Thermo Fisher Scientific trading at a more expensive valuation of 6.5x trailing revenues compared to 2.9x for 3M stock. Even if we were to look at P/EBIT ratio, TMO stock appears to be more expensively priced with 23x P/EBIT ratio, compared to 13x for MMM stock. This gap in valuation actually makes sense, given that Thermo Fisher Scientific has seen much more rapid and consistent sales growth over 3M in the past few years, and it is also more profitable, as we discuss in the sections below. We compare a slew of factors such as historical revenue growth, returns, and valuation multiple in an interactive dashboard analysis 3M vs Thermo Fisher Scientific: Which Stock Is A Better Bet? Parts of the analysis are summarized below. We compare these two companies given that they both have a similar revenue base.

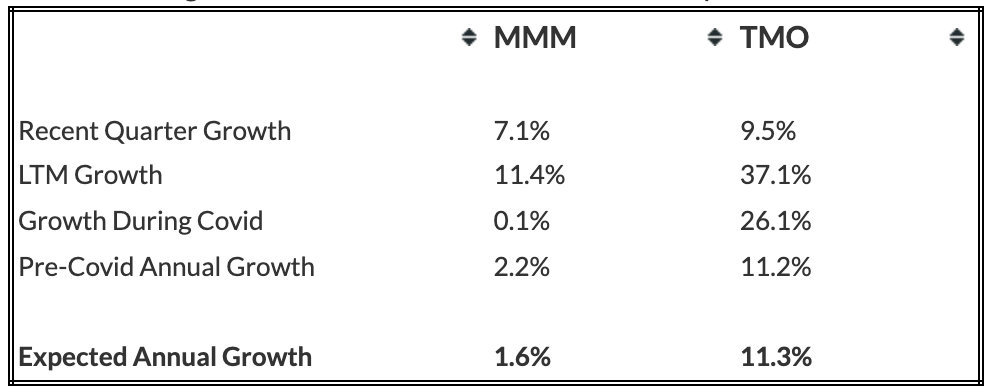

1. Thermo Fisher Scientific Revenue Growth Is Stronger

- Both companies managed to see strong sales growth post the pandemic, but Thermo Fisher Scientific has witnessed much faster and more consistent revenue growth over the years. Thermo Fisher Scientific’s sales have jumped from $18.3 billion in 2016 to $39.1 billion over the last twelve months, while 3M’s revenues have risen from $30.1 billion to $35.3 billion over the same period.

- The recent rise in Thermo Fisher Scientific’s revenue can be attributed to an increase in sales of Covid-19 testing and treatment products. The sales growth is aided by continued market share gains for its instruments. Note that once the instruments are installed, it also generates recurring revenue in the form of after sales service and it also results in demand for consumables.

- Looking at 3M, its revenue growth over the recent quarters is being driven by high demand for safety and personal protective equipment, while sales for some of its other products, including office products was hit during the pandemic due to many offices being shut, given the lockdowns and shelter-in-place restrictions, resulting in lower demand. The demand for transportation products was also down due to lower production of cars, amid chip shortages. Our dashboard on 3M’s revenues offers more details on the company’s segments.

- Looking forward, Thermo Fisher Scientific’s revenue is expected to grow at a faster pace compared to 3M. The table below summarizes our revenue expectation for TMO and MMM over the next three years, and points to a CAGR of 11% for Thermo Fisher Scientific, compared to a CAGR of just 2% for 3M.

- What’s Next For 3M Stock After A 15% Fall This Year?

- After A 14% Fall This Year Is 3M Stock A Better Pick Over Honeywell?

- What’s Next For 3M Stock After A 24% Fall This Year?

- Should You Pick Starbucks Over 3M Stock For Next Three Years?

- What’s Happening With 3M Stock?

- Will 3M See A Sharp Decline In Q2 Earnings?

2. Thermo Fisher Scientific Is More Profitable With Lower Risk

- Thermo Fisher Scientific’s operating margin of 27% over the last twelve month period is better than 22% for 3M.

- Even if we were to look at the recent margin growth, Thermo Fisher Scientific stands ahead, with last twelve month vs last three year margin change at 7.8%, compared to just 0.5% for 3M.

- Looking at financial risk, Thermo Fisher Scientific is again attractive with lower risk compared to 3M. It’s 1% debt as a percentage of equity is much lower than 16% for 3M, while its 16% cash as a percentage of assets is higher than the 10% for 3M, implying that TMO has better debt and cash position, and MMM stock is a comparatively more risky bet.

The Net of It All

- Both the companies have similar revenue base, but the revenue growth has been stronger for Thermo Fisher Scientific. Furthermore, Thermo Fisher Scientific is more profitable and it offers lower financial risk compared to 3M, implying it is a better bet compared to MMM stock, based on historical performance.

- But what about future expectation? Using P/S as a base, due to high fluctuations in P/E and P/EBIT, we believe TMO is the better choice of the two. The table below summarizes our revenue and return expectation for TMO and MMM over the next three years, and points to an expected return of 21% for TMO over this period vs. just 6% for MMM, implying that investors are better off buying TMO over MMM despite its more expensive valuation, in our view. Our dashboard 3M vs Thermo Fisher Scientific has more details on how we arrive at these numbers.

- Note that Covid-19 is proving more difficult to contain than initially thought, due to the spread of more contagious virus variants and infections in many geographies, including the U.S. and Europe, are higher than what they were a few months back. The concerns around Omicron have spooked the markets at large. If there is another large spike in Covid-19 cases from the new variant, resulting in any disruption in economic growth, it is likely to impact sales of several companies, including 3M.

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio that’s beaten the market consistently since the end of 2016.

| Returns | Jan 2022 MTD [1] |

2022 YTD [1] |

2017-22 Total [2] |

| MMM Return | 0% | 0% | -24% |

| TMO Return | -3% | -3% | 240% |

| S&P 500 Return | 0% | 0% | 79% |

| Trefis MS Portfolio Return | 0% | 0% | 292% |

[1] Month-to-date and year-to-date as of 1/4/2022

[2] Cumulative total returns since 2017