Turnaround Stock Pick: MetLife (MET)

Submitted by George Putnam, III as part of our contributors program.

MET Stock Offers Strong Brand Recognition, Management Prowess & Global Diversification–at a Depressed Price

MetLife, Inc.: 200 Park Ave., New York, NY 10166; 212-578-2211

- Will United Airlines Stock Continue To See Higher Levels After A 20% Rise Post Upbeat Q1?

- Up 8% This Year, Why Is Costco Stock Outperforming?

- Down 7% In A Day, Where Is Travelers Stock Headed?

- What’s Next For Johnson & Johnson Stock After Beating Q1 Earnings?

- Should You Pick UnitedHealth Stock At $480 After A Q1 Beat?

- American Express Stock Is Up 17% YTD, What To Expect From Q1?

Category: Large-Cap ($40.3 Bil.)

Symbol: MET

Exchange: NYSE

Business: Life Insurance

Annual Revenue: $70.26 Bil. (12/31/11)

Earnings: $6.71 Bil.

1/30/13 Price: 37.20

12 month Range: 39.55-27.60

Max. Rec Price: 45

Est Dividend Yield: 2.0%

BACKGROUND: Founded in 1864 as the National Union Life and Limb Insurance Company, MetLife (MET) has grown into the largest life insurance company in the U.S. It currently has about $4.2 trillion of life insurance in force.

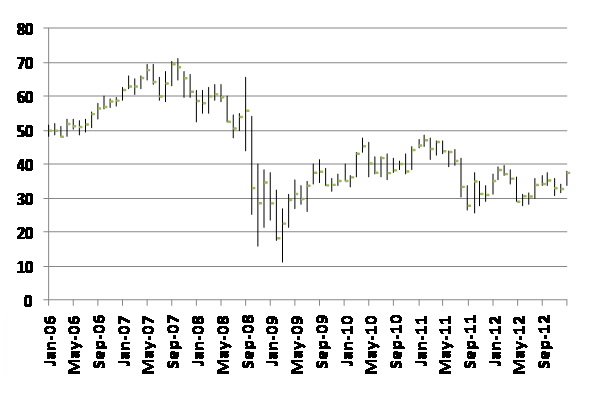

The stock rose gradually to a high of 71 in 2007. Then, like many financial companies, MetLife saw its stock get hit hard in 2008, and it has never really recovered.

ANALYSIS: MetLife has long had one of the strongest franchises and best recognized brands in the life insurance business. The company is now shedding other business lines so that it can focus more on its core competency. For example, MetLife recently completed the sale of its banking business to GE. This not only removes the distraction of the banking business, but it also gets the company out from under the more stringent capital requirements that apply to bank holding companies.

The company is also shifting its business mix to improve its risk profile. One example of this is management’s decision to move away from the capital intensive and market sensitive variable annuity business.

In addition to its strength in the U.S., MetLife has a substantial and growing presence abroad. It is particularly strong in emerging markets which are likely to offer much greater growth opportunities than the U.S. and Europe. The company greatly boosted its global and emerging market exposure when it purchased AIG’s ALICO unit in 2010.

Despite the strength of the franchise, the stock looks cheap on a valuation basis as investors continue to spurn old line financial companies. The stock currently trades at just 0.62 times book value, compared to well above 1.0 where it traded for many years before 2008. Moreover, the stock has a forward price/earnings ratio of only about 7x.

While MetLife has extricated itself from bank holding company regulation, it is still subject to the non-bank Systematically Important Financial Institution rules created by the Dodd-Frank legislation. Since those rules are still evolving, the company has been cautious about buying back stock or increasing its dividend. However, I expect MetLife to take one or both of those shareholder friendly steps once the regulatory fog begins to clear.

I believe that Wall Street’s current aversion to financial stocks creates an opportunity to buy a powerful and growing insurance franchise at a depressed price and recommend buying MetLife up to 45.