Intuitive Surgical Stock Headed To $1,000 Levels?

Intuitive Surgical (NASDAQ:ISRG), a fast growing medical devices company with a market capitalization of $84 billion, has seen its stock rise by 20% this year, outperforming the broader indices, with the S&P 500 up 4%. The stock now trades at over 72x projected 2020 earnings, despite the fact that the company will post a decline in earnings this year. Does this make the stock expensive? We don’t think so, considering that revenues could grow over 50% by 2023, while earnings growth is expected to be over 90% over the same period, generating strong returns for shareholders. Here’s how this is possible.

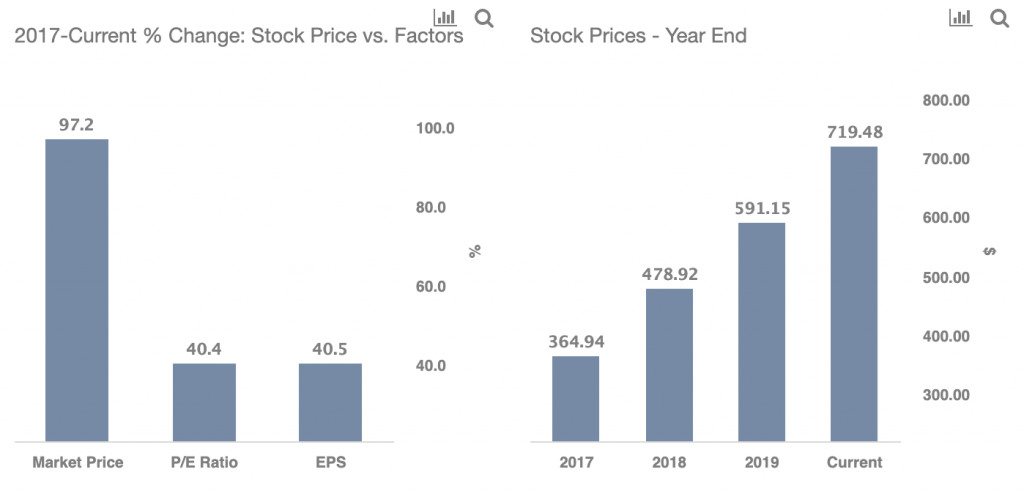

For more details on Intuitive Surgical’s historical performance, see our interactive dashboard What Factors Drove Intuitive Surgical stock up 97% Since The End Of 2017

Intuitive Surgical’s Revenues could grow 50% from the estimated $4.3 billion in 2020 to around $6.7 billion by 2023, representing a growth rate of roughly 16% per year (for context annual growth was about 18% between 2016 and 2019). There are multiple trends that support this continued growth. Firstly, we believe that the deferred elective surgeries due to the Covid-19 pandemic in Q1 and Q2 that is impacting Intuitive Surgical’s sales in 2020, will eventually be attended to. It is not that someone who is advised to have a surgery will decide not to take it. With economies opening up gradually, already several healthcare institutions have started addressing elective surgeries. Intuitive Surgical makes robotic platforms and associated instruments and accessories for different types of procedures. The company has seen steady expansion of its installed base from less than 4,000 units in 2016 to over 5,500 units in 2019, and it will likely be north of 8,000 units by 2023, with patients and physicians opting for robotic surgeries over traditional surgery over the coming years. This can be attributed to benefits associated with robotic assisted procedures, including less blood loss, fewer scars compared to traditional surgery, and faster recovery.

- Should You Pick Intuitive Surgical Stock At $375 After An Upbeat Q4?

- Is Intuitive Surgical Stock A Pick After A 9% Fall In A Month Amid Mixed Q3?

- Procedure Volume Growth To Drive Intuitive Surgical’s Q3

- With 2x Potential Returns Is DexCom A Better Pick Over Intuitive Surgical?

- Here’s What To Expect From Intuitive Surgical’s Q2

- Should You Buy Intuitive Surgical Stock Over MDT?

While Intuitive Surgical will likely post a decline in earnings this year, the company could see strong earnings growth over 2020-2023, as the company’s past investments in R&D and product development start paying off, along with continued expansion of its installed base. The company has been able to improve its Net Margins from 28% in 2014 to 34% in 2019. While we do expect a hit on margins in 2020, the margins will likely rebound to 34% levels by 2023 or sooner, and continue to expand over the coming years. In fact, Intuitive Surgical’s Net Margins are better than some of its peers, such as Abbott with margins of 18% in 2019, Boston Scientific’s 21%, and Medtronic’s 21%. Considering our revenue projections of roughly $6.7 billion and 34% margins, $19.00 in Adjusted EPS is likely possible by 2023, as compared to the projected $10.00 in 2020.

Now, if Intuitive Surgical’s earnings grow 90% between 2020-2023, the P/E multiple will shrink to 38x from its current level, assuming the stock price stays the same, correct? But that’s what Intuitive Surgical’s investors are betting will not happen! If earnings expand 90% over the next few years, instead of the P/E shrinking from around 72x presently (based on expected 2020 earnings) to about 38x, a scenario where the P/E metric falls more modestly, perhaps to about 55x, looks more likely. For context, Intuitive Surgical has seen a steady growth in P/E multiple from 40x in 2017 to 46x in 2019, given the increased adoption of robotic surgery, a trend which is likely to continue over the coming years. This would make growth in Intuitive Surgical’s stock price by over 45%, to around $1,050 levels, likely over the next three years.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams