Intel Revenue Growth To Slow?

Intel’s (NASDAQ:INTC) revenue growth could slow to low-single-digits on average between 2018-2021, as compared to high single-digit growth seen between 2016-2018. This can be attributed to slower data center demand in 2019, and the company’s ongoing chips shortage in the PC/notebook market. In this note we discuss Intel’s key revenue sources, its business model, past revenue growth, and expected trajectory. You can look at our interactive dashboard analysis ~ INTC Revenues: How Does Intel Make Money? ~ for more details.

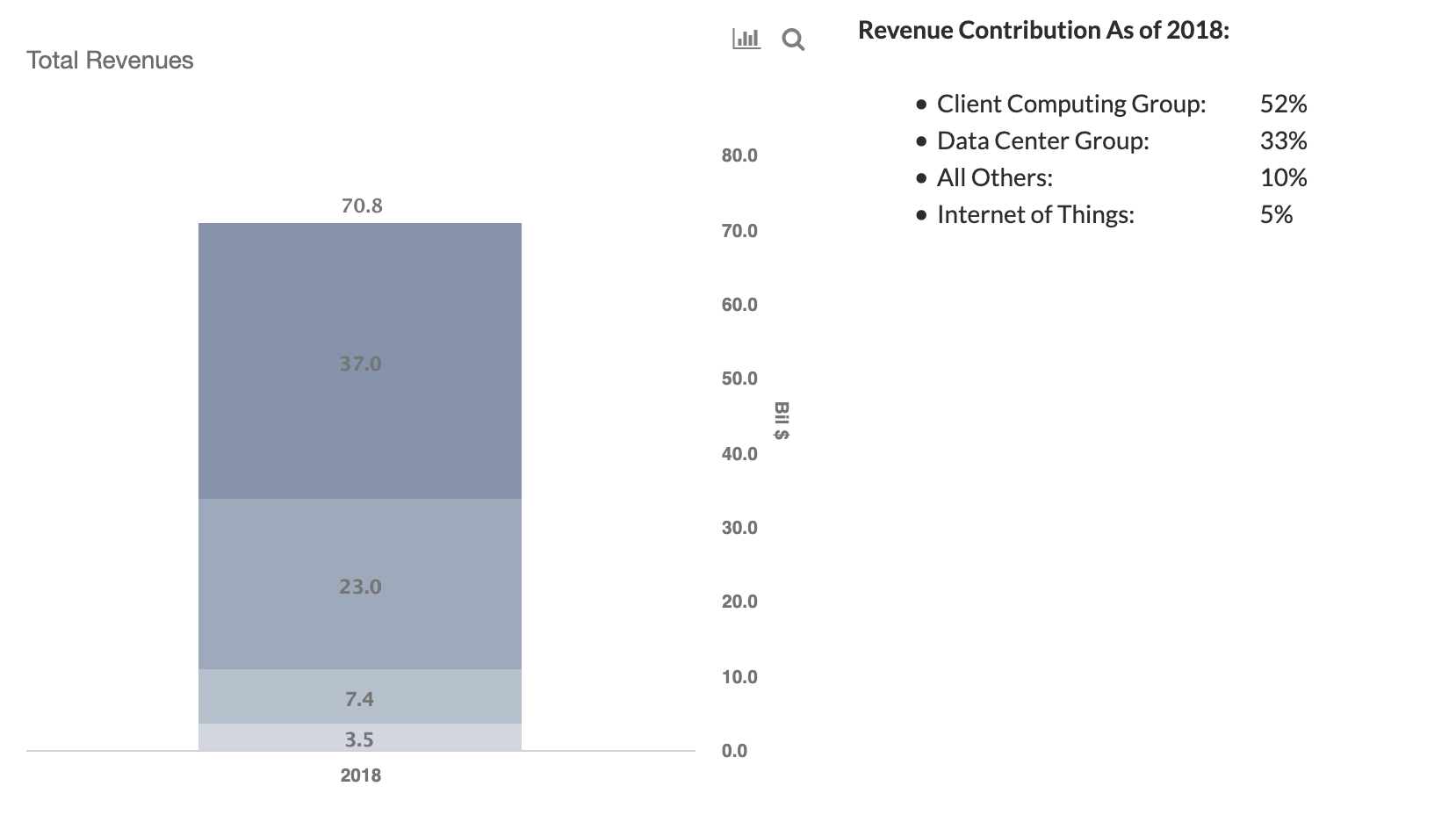

Client Computing Group, Which Includes Products For Desktops, Notebook, And Mobile, Accounts For Over Half of Intel’s Revenue

- Client Computing Group includes revenue from processors and platform products designed for use in notebooks, desktops, tablets, phones, and other mobile communication products.

- Data Center Group includes sales of processors and chipsets designed for the enterprise, cloud, communications infrastructure, and technical computing segments.

- All Other includes revenue from software products for endpoint security, network and content security, risk and compliance, and software products and services that promote Intel architecture as the platform of choice for software development. The division also includes results of operations from Intel’s reported segments including Non-Volatile Memory Solutions Group, Programmable Solutions, and All Other.

- Internet of Things includes revenue that Intel earns from the sale of platforms designed for embedded applications for medical, automotive, industrial, retail, and other market segments; as well as software-optimized products for the embedded and mobile market segments. It also includes small low-power chips that are used in wearable devices and a range of consumer and industrial products.

- Down 29% This Year, What Lies Ahead For Intel Stock Following Q1 Earnings?

- Will Intel Stock Return To Pre-Inflation Shock Highs Of $68?

- Gaining 50% Over The Last 12 Months, Will Intel Stock Rally Further After Q4 Results?

- Will Intel Stock Recover To Pre-Inflation Shock Highs?

- Up 44% This Year And With Foundry Plans Taking Shape, Will Intel Stock See Further Gains?

- What To Expect From Intel’s Q3 Results?

Intel’s Business Model

- What Need Does It Serve?

- Intel primarily serves the microprocessor market for PCs, notebooks, and servers, among others. Microprocessor refers to the central processing unit (CPU) or the brain behind a computer. A microprocessor is the single most important component that drives a computer’s power and performance. Intel also manufactures chipsets used in desktops, notebooks, and wireless devices.

- Who Pays To Intel?

- Original equipment manufacturers (OEMs) and original design manufacturers (ODMs).

- Individuals building custom PCs or replacing their current desktop microprocessors are also buyers.

- Numerous smartphone, tablet, and smart TV manufacturers.

- Server manufacturers such as IBM, Dell, HP, and Fujitsu.

- What Buyers Care About?

- Speed & performance

- Reliability

- Power efficiency / battery consumption

- Price (relative to performance)

- Power consumption and heat (energy efficiency)

- Compatibility with other hardware

- Volume discounts

- Who Are Intel’s Key Competitors?

- While Intel’s market share in the processor market is greater than 70%, its major competitor is AMD, and Nvidia in some product offerings.

- What Are Intel’s Top Selling Points?

- Long track record of providing high-quality microprocessors

- Dependability, compatibility, scalability, and advanced architecture to meet the demand for multi-processing environments.

- ‘Intel inside’ brand is valued by customers

- Ability to offer attractive pricing for volume buyers, such as Dell, Toshiba, and Sony

While Intel’s Revenue Grew 19% Between 2016-2018, They Will Likely See Slower Growth In The Near Term

- Intel total revenue grew from $59.4 billion in 2016 to $70.8 billion in 2018.

- This growth was largely led by its Data Center Group, which benefited from higher demand for its Xeon Scalable products among the enterprise and cloud & communications customers.

- However, as we look forward, the average annual revenue growth rate could slow to low single-digits, with revenues expected to decline in 2019, for the factors discussed in the following sections.

Slower Revenue Growth Going Forward Will Likely Be Led By Data Center Group.

- Of late, Intel has been losing share in the CPU market to AMD. In fact, AMD’s share increased from less than 20% in Q3 2016 to over 30% as of Q3 2019. This trend could continue and impact Intel’s Computing & Graphics revenue in the near term. However, with the new 10nm chips being scaled, the sales could rebound in 2020 and 2021.

- There has been a shortage of Intel’s chips for CPUs over the last few quarters, as the company has been focused on ramping up its production to meet the demand for its data center business.

- This also benefited AMD, as many OEMs started offering Ryzen processor-based desktops and notebooks. However, the shortage issue will likely end by the end of 2019, and Intel could see some growth in 2020 and 2021.

- Intel guidance for the full year 2019 was revised upward post the Q3 earnings announcement, and the company now expects no growth in its Data Center Group revenue, which is better than its earlier forecast of a mid-single-digit decline. This can be attributed to weakened demand from China, and inventory absorption.

- Also, AMD’s EPYC processors have been gaining traction in the server market, and its new “Rome” architecture appears to be strong in performance, and this could pose some threat to Intel’s market share in the near term.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.