Here’s What Will Drive Intel’s Near Term Earnings Growth

Intel (NASDAQ:INTC) is seeing strong growth in its Data Center business, and we expect it to drive the company’s near term earnings growth. The strong demand for high performance products, such as Xeon Scalable, has aided the segment growth in the recent past, and we expect this trend to continue in the near term. Apart from the Data Center Group, the company’s Client Computing Group will also aid the overall earnings growth, led by modest growth in the overall PC TAM (total available market). We have created an interactive dashboard ~ What Will Drive Intel’s Near Term Earnings Growth. You can adjust the revenue and margin drivers to see the impact on the company’s overall earnings, and price estimate.

Expect Data Center Group To Drive Near Term Growth

- Down 29% This Year, What Lies Ahead For Intel Stock Following Q1 Earnings?

- Will Intel Stock Return To Pre-Inflation Shock Highs Of $68?

- Gaining 50% Over The Last 12 Months, Will Intel Stock Rally Further After Q4 Results?

- Will Intel Stock Recover To Pre-Inflation Shock Highs?

- Up 44% This Year And With Foundry Plans Taking Shape, Will Intel Stock See Further Gains?

- What To Expect From Intel’s Q3 Results?

We forecast the Data Center Group revenues to grow in low 20s percent for the full year 2018. The segment is benefiting from its cloud business, as well as high performance products, primarily Xeon Scalable. The company is seeing growth in all verticals, Cloud, Enterprise & Government, and Communications. Cloud, in particular, is seeing strong growth and saw a 50% jump in Q3 revenues. The overall public cloud computing market is expected to grow in the low 20s percent to $186 billion in 2018, according to a research by Gartner. Growth in cloud computing will result in higher demand for faster and high performance servers, and this will bode well for Intel. While Intel’s market share in data center servers is in the high nineties percent, AMD is trying to increase its market share with its EPYC processors (Also see ~ Expect Ryzen And EPYC To Drive AMD’s Future Earnings Growth). Given the overall growth in the cloud computing, Intel’s Data Center Group will continue to see strong growth in the near term, in our view. Also, we expect a slight uptick in EBITDA margins, led by higher ASPs for its products.

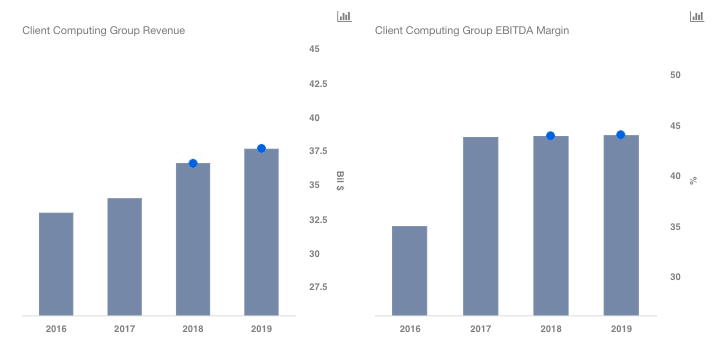

Client Computing Group Will Aid The Overall Earnings Growth

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.