Higher Motorcycle Sales Drive Honda’s Q2 Results; Profitability Outlook Remains Speculative

Honda Motors (NYSE: HMC) released its September quarter results on October 30, 2018, and conducted a conference call with analysts on the same day. The company posted approximately $35 billion sales revenues in this quarter, a 1.7% increase in its sales revenues as compared to the period last year, largely driven by higher sales volumes in its motorcycle segment and higher revenues from its financing services segment. The company posted an EPS of $1.08 (assuming $1 dollar is equal to 110 yen), which included approximately $0.5 billion litigation settlement and restitution income related to an airbag inflator accident last year. Going forward, the company forecasts lower operating margins in FY’19 due to negative currency impacts and declining automobile sales in its key markets.

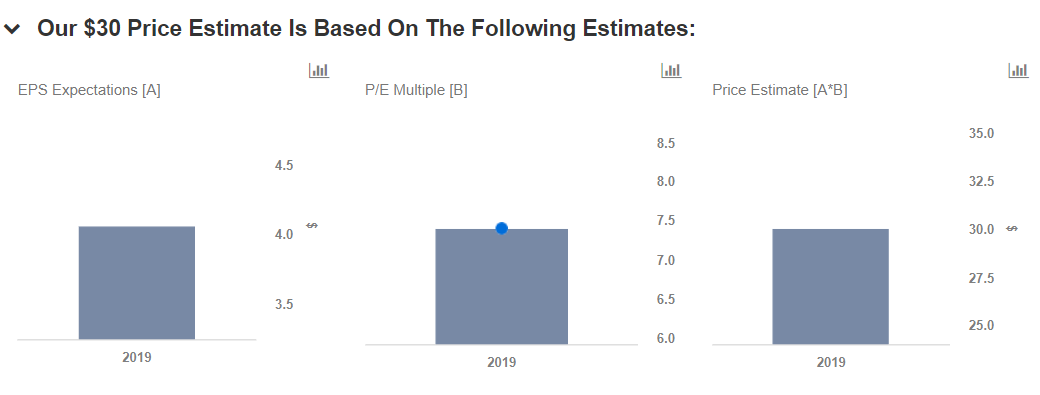

We have a price estimate of $30 per share for the company, which is higher than the current market price. View our interactive dashboard – Our Outlook For Honda Motor Company In FY’19 – and modify the key assumptions to reach a price estimate of your own.

Key Highlights From Q2’19 and H1’19

The company posted a 1.7% increase in sales revenue and a 21.7% increase in its consolidated profit in its second-quarter results, primarily due to increased sales revenue at motorcycle and financial services business operations. The increase in the operating profit was attributed to the positive impact from revenue and model mix and the multi-district class action litigation settlement in the same period last year. The company’s motorcycle sales for this quarter witnessed a 1.5% increase as compared to the year-ago quarter, largely due to higher volume sales in Indonesia, Vietnam, and Brazil. Further, the company expects higher motorcycle production by 2020 due to an expansion of production capacity in one of the plants in India. The company is expecting a steep rise in its motorcycle demand in some of its key markets, which also includes developing economies like Brazil and Vietnam.

Power products sales were relatively flat compared to the last year, while the automobile sales witnessed a decrease mainly due to sales decline in North America and China despite a growth in sales in its domestic market. Despite the lower automobile sales in North-America, the company realized a 4% increase in its sales revenue for this quarter, backed by higher pricing of its automobiles in this region.

The company also experienced a 6% increase in sales in its domestic market. Asian sales revenue was down 0.7% in this quarter though first-half sales revenue for Asian markets was up by 5%. Automobile business saw a 0.9% decline in revenue. The company experienced an 11% increase in its sales revenue from the financial services segment. Unit sales from domestic markets for the first half in the automobile segment stood at 346k units. The company had posted a 40% increase in operating profit for the first 6-months, largely due to the litigation settlement and higher sales volume of its motorcycles and higher sales revenue from its finance field operations.

Further, Honda is planning to invest nearly $3 billion in GM’s Cruise, with $750 million already invested in this quarter. The investment will be spread over the next 2 years, which will increase Honda’ stake in GM’s cruise to 5.7%. Cruise has been set up as a separate business unit with an outlook to develop autonomous (including driver-less) vehicles that can be manufactured at high volumes for global deployment. Softbank also has a substantial stake in Cruise.

Key Expectations From Honda Motor Company in FY19

The company expects a 3% increase in its sales revenues, depicting a mild rise in its automobiles sales amid the declining sales in China and a sharp rise in its motorcycle sales. The company has revised its motorcycle sales forecast by 0.7% for FY’19 consequently. Operating profits are expected to be lower in this financial year, largely due to negative currency impacts outside the US (strong yen) and higher SG&A expenses and capital expenditures. The impact of a plant flooding in Mexico is expected to weigh on the operating profit margins in FY’19, though the company has increased its expectation for operating profit by 80 basis points from its previously expected $6.5 billion. We expect $7.4 billion in net income for the company.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.