After A 3x Increase This Year, Could Etsy Stock Rise Further?

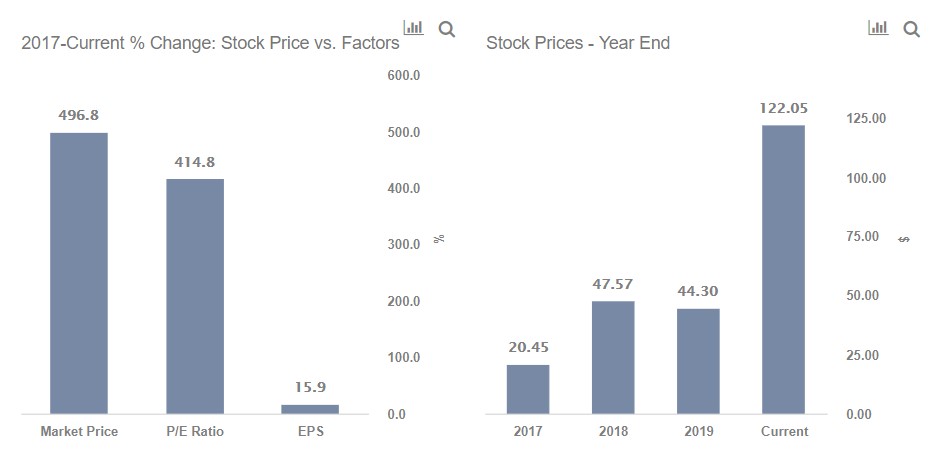

After rising by close to 3x this year, we believe Etsy has little upside left in the near-term. Etsy stock (NASDAQ:ETSY) is up from around $45 in early January to the current price of around $122 per share, better than the S&P 500 which increased by just around 3%. The rise in stock price is driven by Etsy’s solid performance through the Covid-19 pandemic, as the e-commerce marketplace saw demand for masks, handmade products, and craft supplies surge. Etsy stock currently trades at almost 6x the levels at which it was at the end of 2017. While Etsy stock has provided solid returns, with its long-term prospects also remaining strong, we believe the scope for near-term price gains is limited. Our dashboard What Factors Drove 500% Change In Etsy Stock Between 2017 And Now? has the underlying numbers on what drove Etsy’s stock price appreciation.

Some of the stock price rises in the 2017-2019 period are partly justified by the 85% growth in revenues. Etsy’s revenues increased from $441 million in 2017 to $818 million in 2019. This was partly offset by a decrease in net income margin from 18.5% in 2017 to 11.7% in 2019 though the Net Income increased by 17% in the period. On a per-share basis, earnings increased by 16% from $0.69 in 2017 to $0.80 in 2019. Now Etsy’s P/E multiple has seen a sharp increase, rising from about 30x in 2017 to 55x in 2019. The multiple shot up significantly this year and currently stands at 153x due to higher anticipated growth due to Covid-19, which is boosting demand for online shopping, particularly for the niche items that Etsy offers. For perspective, the company saw revenue rising 137% year-over-year to $429 million in Q2, with EPS rising by about 5x to $0.75 per share. The company’s Gross Merchandise Sales (GMS) jumped by about 146% year-over-year during Q2.

- Should You Pick General Electric Stock At $165?

- What’s Next For JetBlue Stock After A Sharp 19% Fall Post Q1 Results?

- Is Kimberly-Clark Stock Fairly Valued At $135 After A Solid Q1?

- How Will AMD’s AI Business Fare In Q1?

- Up 9% Year To Date, Will Chevron’s Gains Continue Following Q1 Results?

- Earnings Beat In The Cards For Honeywell?

Etsy still has a lot more room for growth. While GMS stood at $5 billion in 2019 and about $4 billion over the first half of 2020, the company estimates its total addressable market at about $250 billion online for relevant categories it sells and over $1.7 trillion, including offline. Now although we don’t doubt Etsy’s long-term potential, price, and valuation matter a lot in the near-term and we believe that returns, adjusted for risk in the near term could be weak. With lockdowns being lifted, demand growth could slow down. For instance, Etsy has indicated that year-over-year revenue growth rates in Q3 could stand at between 85% to 115% (compared to 137% in Q2). With the stock already up close to 3x this year, investors will need to focus on the company’s execution post the Covid-19 pandemic to justify further outperformance. Etsy’s stock has been volatile in recent weeks and declined by about 12% over the last five trading days alone, potentially indicating that investors are turning cautious.

So, while Etsy seems to have run out of room to grow in the near-term, want out-performance? Try guessing the % returns for our Pershing-inspired portfolio – based on billionaire Bill Ackman’s firm Pershing Square – vs. the S&P over the last 1 week, 1 month, 3 months, YTD or even 3 years. Our portfolio combines high growth, quality, and risk mitigation criteria in an interesting way.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams