Where Is Dish Network’s Stock Headed After An 80% Rise?

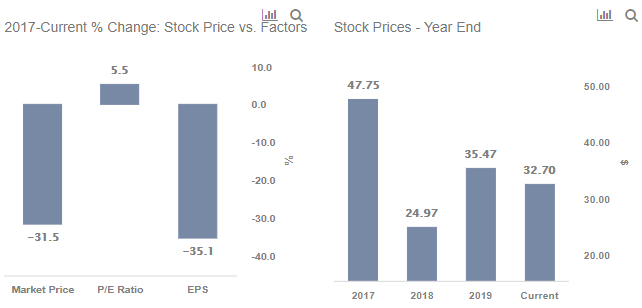

Despite an 83% rise since the March 23 lows of this year, at the current price of around $33 per share we believe Dish Network’s stock (NASDAQ: DISH) has a marginal upside from its current level. DISH’s stock price has rallied from $18 to $33 off the recent bottom compared to the S&P which moved 36%. DISH managed to outperform the broader market as it posted better than expected revenues in Q1 2020 along with its 5G and postpaid mobile plans being on track. With the current stock price being slightly lower than the level at the beginning of the year, we believe that DISH’s stock is likely to see a slight rise from the current level. Our dashboard What Factors Drove -31% Change In Dish Network Stock Between 2017 And Now? provides the key numbers behind our thinking.

Some of the stock price decline of the last 2 years is justified by the 11% decrease in Dish Network’s revenues, from $14.4 billion in 2017 to $12.8 billion in 2019, mainly due to lower subscriber-related revenues as an increasing number of users are switching to SVOD (streaming-video on demand) platforms, like Netflix and Amazon. This was further exacerbated by a 31% decline in net income, as net income margin dropped from 15% in 2017 to 11.7% in 2019, due to higher subscriber acquisition costs and impairment charges. On a per share basis, earnings dropped from $4.50 in 2017 to $2.92 in 2019.

- With Echostar Merger Approaching, What To Expect From Dish’s Q3 Results?

- Can Dish Network Stock Return To Its Pre-Inflation Shock Highs?

- Dish Stock Has Big Upside Potential To Its Pre-Inflation Peak

- How Will The Cyber Attack Impact Dish’s Q1 Results?

- Is Dish Network Stock A Buy Despite Many Headwinds?

- Will Dish Network Stock Continue To Underperform?

While the company saw steady decline in revenue and profit, the P/E multiple increased from 10.6x in 2017 to 12.1x in 2019 (multiple dropped in 2018 due to sharp decline in stock price), as the slide in EPS was much higher than the stock price decline during this period. The P/E multiple currently stands at 11.2x, which is still higher than levels seen 2 years ago as the market seems to believe that the effect of coronavirus will be offset by the expansion of 5G technology.

What’s The Trigger For Upside?

The ongoing crisis and the resulting lockdowns have led to a slowdown in industrial and economic activity, driving up unemployment and partial employment. Lower income has affected consumer spending power, leading to decreased demand for the company’s offerings, with demand for streaming services from Netflix, Amazon, and Disney increasing significantly, adversely impacting Dish Network. This was confirmed in the Q1 2020 results where we saw that the pandemic caused severe disruption in certain commercial segments served by the company including the hospitality and airline industries. The company lost 413,000 net Pay-TV subscribers in the reported quarter compared with 259,000 lost a year ago. Moreover, DISH lost nearly 281,000 net Sling TV subscribers and 132,000 DISH TV subscribers. However, the market seemed to be unfazed with the loss in subscribers during the crisis, as the company managed to increase revenue almost 1% due to a 4.4% increase in average revenue per user (ARPU) on y-o-y basis.

Investors also seem to be buoyed by Dish’s plans of being in the post-paid mobile business in a year from now. Also, its ambitious 5G rollout plan seems to be bearing fruit, with Dish announcing that it hopes to get a 5G network core nailed up in at least one US market in 2020. Having invested close to $11 billion directly to acquire certain wireless spectrum licenses and related assets, the company plans to cover around 70% of the US population by mid-2023.

Over the coming weeks, we expect subdued growth in the number of new Covid-19 cases in the U.S. to buoy market expectations. Following the Fed stimulus — which set a floor on fear — the market has been willing to “look through” the current weak period and take a longer-term view. With investors focusing their attention on 2021 results, the valuations vs historic valuations become important in finding value. Our dashboard forecasting U.S. Covid-19 cases with cross-country comparisons analyzes expected recovery time-frames and possible spread of the virus. Further, our dashboard -28% Coronavirus crash vs. 4 Historic crashes builds a complete macro picture. The complete set of coronavirus impact and timing analyses is available here.

In the near term, we believe the company’s stock has upside potential. Based on Dish Network’s valuation, Trefis has a fair price estimate of $36 per share for DISH’s stock. In contrast, see how much can close-rival Comcast gain post Covid-19?

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams