Deutsche Bank’s Cost-Cutting Efforts Should Help Earnings Grow In 2019 Despite Weak Revenue Outlook

Deutsche Bank (NYSE: DB) recently released its results for the first quarter. The German banking giant reported a better-than-expected net income figure of €201 million for Q1 2019 (up 67% y-o-y), as a sizable reduction in compensation as well as other operating costs offset the impact of weak revenues. Per Trefis estimates, Deutsche Bank’s shares have a fair value of $9, which is roughly 25% ahead of the current market price. We have summarized our full-year expectations for Deutsche Bank in our interactive dashboard – How Did Deutsche Bank Fare in Q1 and what can we expect for full-year 2019? You can modify any of our key drivers to gauge the impact of changes on the bank’s valuation. Also, see will find more Trefis Financial Services company data here.

A Quick Look at Deutsche Bank’s Revenue Sources

Deutsche Bank reported €25.3 billion in Total Revenues in 2018. This included 3 primary revenue streams:

- Private & Commercial Bank: €13 billion in FY 2018 (51% of Total Revenues). This segment derives revenues by provides banking services to retail and affluent clients as well as small- and medium-sized businesses.

- Corporate and Investment Bank: €10.1 billion in FY 2018 (40% of Total Revenues). Revenues for this segment are derived by providing services to institutional, corporate and wealth management clients to help them raise capital, grow their businesses, invest and manage risks.

- Asset Management: £2.2 billion in FY 2018 (9% of Total Revenues). This segment generates revenues by providing retail as well as institutional clients a fully-integrated asset management offering.

Key Takeaways From Deutsche Bank’s Q1 Results

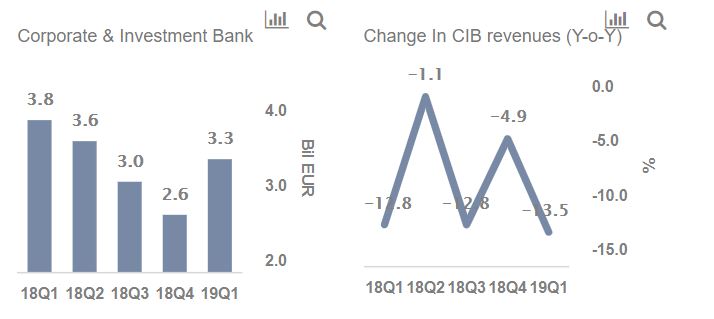

Corporate & Investment Bank (CIB) Was Hurt By Industry Headwinds

- Deutsche Bank’s CIB division reported a pre-tax loss of €88 million for the first quarter of 2019 while its revenues declined by 13% y-o-y to €3.3 billion. This decline can be attributed primarily to an 18% decline in Equity Sales & Trading revenues due to challenging market conditions which hurt securities trading activity for the period. The bank’s Origination & Advisory revenues also fell 5%, as higher Advisory revenues were offset by lower revenues from its Debt as well as Equity Origination desks.

- However, Global Transaction Banking revenues increased 6% (y-o-y) to €975 million driven by higher net interest income, particularly in cash management.

- Going forward, we expect the CIB division to return to profitability as market activity increases and client confidence rebounds.

Asset Management Business Had A Mixed Quarter

- Asset Management reported revenues of €525 million, down 4 % versus the prior year quarter while pre-tax profit increased by 34% to €96 million. The year-on-year decline in revenue was driven in part by lower management fees resulting from net outflows for the trailing twelve months and the market decline in the fourth quarter of 2018, while higher profits were mainly due to a 16% reduction in non-interest expenses.

- Total Assets under Management increased by 6% to € 706 billion during the quarter driven by market recovery, positive forex changes and net inflows of €2 billion. Going forward, the bank expects net new money growth to be in the range of 2-3%, while the segment’s adjusted Cost-to-Income Ratio is projected to be less than 65% (down from 71% in Q1). We believe that a steady growth in new inflows coupled with reduction in operating expenses will likely boost revenues and profitability of this division in the near term.

Cost Cutting Measures Continue

- Deutsche Bank has been extremely successful in reducing costs over the years, with non-interest expense falling from €38.6 billion in 2015 to €23.5 billion in 2018 (CAGR: -15.3%). This can be primarily attributed to the bank’s rigorous cost management efforts, which has helped the bank reduce non-compensation expenses by more than 50% during this period.

- During the first quarter, the bank was able to reduce adjusted costs by 7% year-over-year – marking the fifth consecutive quarterly reduction in adjusted costs (excluding bank levies). This decline can be attributed to year-on-year reductions in both compensation and non-compensation costs, led by a reduction in workforce and active management of consumption and vendor spending. Additionally, the management reaffirmed that the bank remains on track to achieve its target of €21.8 billion in adjusted costs for 2019.

Outlook for Full-Year 2019

- For the full year, we expect minimal growth in Deutsche Bank’s revenues, although net income margin is expected to improve to 4.5% (from -0.1% in 2018) on the back of lower operating expenses and a lower effective tax rate.

- We expect the bank’s EPS for full-year 2019 to be around €0.54. Using this figure with our estimated forward P/E ratio of 14 and a EUR-USD exchange rate of 1.15, this works out to a price estimate of $9 for Deutsche Bank’s shares which is roughly 25% ahead of the current market price.

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

More Trefis Data

Like our charts? Explore example interactive dashboards and create your own.