Chevron To Ride High On The Recovery In Commodity Prices In 1Q’17

Chevron (NYSE:CVX), one of the world’s largest integrated energy companies, is slated to release its March quarter of 2017 financial performance on 28th April 2017((Chevron To Announce March Quarter 2017 Results, www.chevron.com)), the same day Exxon Mobil (NYSE:XOM), its closest competitor, announces its results for the quarter. Given the recoil in commodity prices in the last few months, the market expects to see a huge jump in the earnings of both these oil and gas majors. However, the recovery in Chevron’s results is likely to be more pronounced than that of Exxon, since the former posted heavy losses in the same quarter of last year, while the latter remained profitable during that period. That said, just like Exxon, Chevron’s 1Q’17 earnings will also be negatively impacted by the weakness in refining margins due to the reversal in commodity prices.

See Our Complete Analysis For Chevron Here

Key Trends Witnessed in 1Q’17

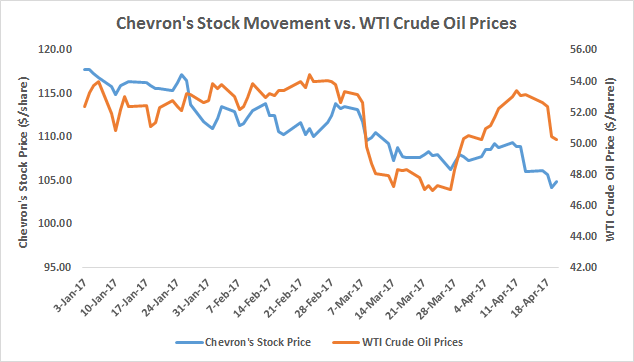

The year 2017 began on a high note for the oil and gas sector, the Organization of Petroleum Exporting Countries (OPEC) began delivering on the production cuts finalized in November 2016. As a result, the commodity prices surged, causing crude oil prices to trade between $50-$55 per barrel for majority of the first quarter. However, the growing US inventory and production in March increased the uncertainty in the commodity markets, sending oil prices below the $50-per-barrel mark, yet again. Still, the oil prices averaged at $52 per barrel for the quarter, drastically higher than the average of $33 per barrel recorded in the same quarter last year. Thus, we expect a notable rise in Chevron’s top-line as well as profits for the quarter.

However, as mentioned earlier, the rebound in commodity prices is likely to pull down Chevron’s refining margins for the quarter. Thus, the company’s downstream operations, which augmented its operations in the weak price environment, are expected to weigh negatively on its improving upstream operations.

Source: Google Finance; US Energy Information Administration (EIA)

On the financial front, Chevron highlighted its intent to become cash balanced in 2017, and to grow its free cash flows in the forthcoming years. For this, the company aims to restrict its capital expenditure at under $20 billion for 2017 and between $17 to $22 billion in the next few years. Apart from this, the oil major reinforced its priority to maintain and grow its dividend, while keeping a strong balance sheet through commodity price cycles. To this effect, the company had increased its quarterly dividend by 1 cent in the December quarter of 2016, and maintained the dividend at $1.08 per share for 2Q’17. While this increase is lower compared to that of Exxon’s, this indicates the company’s willingness to share its improving profitability with its stakeholders.

In terms of operational updates, Chevron’s subsidiary, Cabinda Gulf Oil Company (CABGOC) Limited, commenced production from the main production facility of the Mafumeira Sul project offshore Angola in March 2017. The project is the second stage of development of the Mafumeira Field in Block 0, which has a design capacity of 150,000 barrels of liquids and 350 million cubic feet of natural gas per day. CABGOC is the operator of the project and holds 39.2% interest in the field. The project ramp-up to full production is expected to continue through 2018.

Further, Chevron announced the completion of the sale of its geothermal business in Indonesia to Star Energy Consortium in the first quarter. The company received cash proceeds for the deal, which are likely to be reflected in the March quarter results. To add to this, the company also announced the divestment of its assets in Bangladesh to Himalaya Energy Co. Ltd. These asset sales clearly depict that the company is making progress towards achieving its objective of becoming cash neutral by the end of this year.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap