Will Salesforce’s Stock Continue Growing?

Salesforce.com’s stock (NYSE: CRM) has gained 7% since the end of FY 2021 (ended January 2021), in comparison the S&P 500 gained 17%. The company has seen a high revenue growth over recent years, while net income has grown steadily. In Q1 FY 2022 (ended April 2022) the company recorded a solid revenue growth of 23% y-o-y with the Customer 360 platform gaining traction. Remaining performance obligation at the end of the first quarter was at $35.0 billion, an increase of 19% y-o-y. Cash generated from operations saw a high growth of 74% y-o-y. We believe as organizations turn to cloud and the company continues on the path of innovation, the stock will also continue to grow.

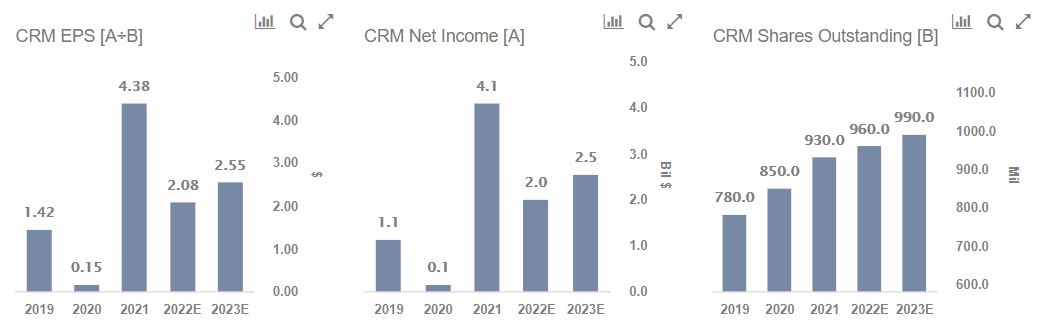

We expect Salesforce.com’s revenues to grow by 26% to $26.8 billion for FY 2022. Further, its net income is likely to be $2 billion, taking the EPS figure to $2.08, which coupled with the P/E multiple of 136x will lead to Salesforce.com’s valuation of $282, up more than 17% from the current market price.

- Down 7.3% In A Day, Where Is Salesforce Stock Headed?

- Up 69% In The Last Twelve Months, What To Expect From Salesforce Stock?

- Up 74% Since The Beginning of 2023, Will Salesforce Stock Continue Its Strong Rally?

- Salesforce Stock Is Undervalued

- Salesforce Stock To Edge Past The Consensus In Q1

- Salesforce Stock Is Trading Below Its Fair Value

[Updated 12/23/2020] Does Salesforce.com’s Stock Have 25% Growth Potential?

Having gained more than 24% in FY 2021 (FY ends in January), Salesforce.com’s stock (NYSE: CRM) still has further growth potential. CRM’s stock has rallied from $182 to $226 in FY 2021 compared to the S&P 500 which moved 15% in the same period. The company has seen a high revenue growth over recent years, and its P/S multiple has also risen steadily. We believe the stock, after the recent rally, still has potential for further growth.

Due to the Covid-19 crisis, organizations started shifting toward the cloud which benefited Salesforce as it saw its revenues rise by 26% in the first nine months of the year, compared to the same period in the previous year. In Q3 2020, Salesforce beat consensus estimates for revenue recorded at $5.4 billion, up 20% y-o-y and earnings recorded at $1.19 compared to -$0.12 in the same period of the previous year. Further, the company reported $2.6 billion in cash inflows from operating activities for the first nine months.

We expect Salesforce.com’s revenues to grow by 23% to $21.1 billion for FY 2021. Further, its net income is likely to grow to $1.4 billion, increasing the EPS figure to $1.47 for FY 2021. Thereafter, revenues are expected to grow further to $25.2 billion in FY 2022. In addition, the EPS figure is likely to improve to $2.36, which coupled with the P/E multiple of 116.8x will lead to Salesforce’s valuation around $275, up more than 20% from the current market price.

[Updated 08/05/2020] Has Salesforce’s Stock Peaked?

After a 45% rise since the March 23 of this year, at the current price of around $203 per share, we believe Salesforce.com’s stock (NYSE: CRM) has no upside left. Salesforce’s stock has increased from $140 to $203 off the recent bottom, compared to the S&P which increased by around 47%. 90% of Salesforce’s revenue is deferred hence the coronavirus is not expected to impact its top line much, leading to the stock recovery. The company also reported positive Q1 2021 (ended April 2020) results, with revenue up 30% y-o-y amid the months where the lockdown was in force across the world.

Salesforce’s stock has nearly reached the level it was at before the drop in February and March due to the coronavirus outbreak becoming a pandemic. Despite that, the revenues will likely be better than last year primarily due to a high percentage of deferred revenue, which we believe the market has already accounted for at current price.

The company gained 42% of its share price since the end of December 2017, and some of this rise over the last 2 years was helped by a 62% rise in Salesforce’s revenues from $10.5 billion in FY 2018 to $17.1 million in FY 2020 (FY ends in January). The net income margin fell from 3.4% in FY 2018 to less than 1% in FY 2020. The fall in margin in FY 2020 is primarily due to one-time foreign incremental tax costs.

The company has seen a steady revenue rise over recent years, and its P/S multiple has also been rising steadily. We believe the stock has no upside left after the recent rally due to the potential uncertainty of Covid outbreak.

Salesforce’s P/S multiple increased from 7x in December 2017 to 8x in December 2019. The company’s P/S has improved to 10x amid the coronavirus pandemic as the revenues are not expected to be affected.

Effect of Coronavirus

The global spread of coronavirus has led to lockdown in various cities across the globe, which has affected industrial and economic activity. This is likely to adversely affect consumption and consumer spending. Notably, Salesforce’s stock is up by about 12% since January 31, after the World Health Organization (WHO) declared a global health emergency in light of the spread of coronavirus. However, during the same period, the S&P 500 index saw a rise of about 2%. Despite the coronavirus pandemic the company saw a 30% growth in Total revenues for Q1 2021. Salesforce Platform and Other led the revenue growth recorded at 61% y-o-y with $273 million contributed from the acquisition of Tableau (The segment’s growth was still high at 31% if we remove the contribution due to Tableau’s acquisition).

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio that’s beaten the market since 2016.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams