ConocoPhillips’ 1Q’17 Earnings Growth To Be Driven By Higher Commodity Prices And Cost Savings

Given the upswing in commodity prices in the last few months, the market anticipates ConocoPhillips (NYSE:COP), one of the largest independent oil and gas companies, to report a remarkable improvement in its March quarter results this week((ConocoPhillips To Announce March Quarter 2017 Results, 6th April 2017, www.conocophillips.com)), both on an annual and sequential basis. In addition to the improved pricing environment, the E&P company’s relentless efforts to bring down its operating costs are likely to reap solid results, and further boost its first quarter earnings. Just to reiterate, the company had exceeded the earnings estimate by a huge margin in the last quarter due to its cost saving initiatives and better price realizations. Hence, the investors remain optimistic about the company’s 1Q’17 performance.

However, the highlight for the quarter was the two major asset sales finalized by ConocoPhillips. The divestitures will generate proceeds of $16 billion, and will help the company optimize its balance sheet, while reducing its average cost of supply, which will be enhance its profits as well as shareholder returns.

See Our Complete Analysis For ConocoPhillips Here

- Up 15% In Last Six Months, Will ConocoPhillips Stock Continue To Grow Post Q3?

- ConocoPhillips Q2 Earnings: What Are We Watching?

- What’s Next For ConocoPhillips Stock?

- ConocoPhillips Stock To Likely Trade Higher Post Q4

- This Stock Appears To Be A Better Bet Than EOG Resources

- Earnings Beat In The Cards For ConocoPhillips Stock?

Improved Commodity Prices To Boost Top-line

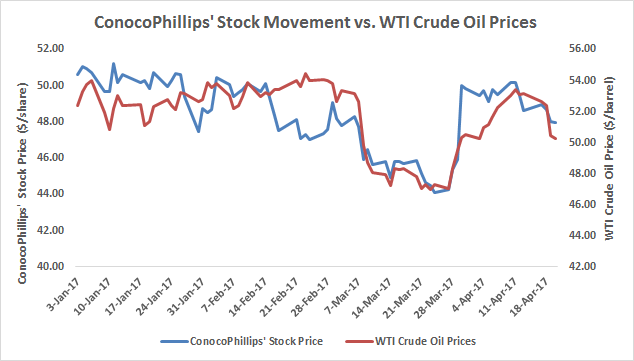

As mentioned earlier, the commodity markets finally showed some resilience in the March quarter, as the Organization of Petroleum Exporting Countries (OPEC) implemented the production cuts agreed upon in November 2016. As a result, crude oil prices surged and averaged at around $52 per barrel during the quarter, as opposed to an average of only $33 per barrel in the same quarter of last year. Also, since gas prices move in tandem with oil prices, the Henry Hub gas prices increased from $1.99 per MMBTU in 1Q’16 to over $3.02 per MMBTU in the latest quarter. This rebound in oil and gas prices is expected to result in an improvement in ConocoPhillips’ price realizations, boosting the company’s top-line growth for the quarter.

Data Source: Google Finance; US Energy Information Administration (EIA)

Early Achievement of Divestment Plans

During the quarter, ConocoPhillips announced the sale of its 50% non-operated interest in the Foster Creek Christina Lake (FCCL) oil sands partnership, and the majority of its western Canada Deep Basin gas assets, to Cenovus (NYSE: CVE) for total sum of $13.3 billion in March 2017. The company will receive $10.6 billion in cash, and 208 million Cenovus shares worth $2.7 billion as part of the deal, along with five years of uncapped contingent payments, triggered if the Western Canada Select (WCS) crude price exceeds $52 Canadian dollars per barrel.

The cash received from the deal will allow the company to rapidly pare down its long term debt from $27 billion to $20 billion by the end of this year, as opposed to its expectation of meeting this target by 2019. Lower debt obligations will not only improve the company’s chances of achieving an “A” credit rating, but will also shrink its interest expenses significantly, lifting its profitability in the short term. In addition, the oil and gas producer plans to double its share repurchase authorization to $6 billion to deliver higher value to its shareholders.

Within a fortnight of announcing the Canadian deal, ConocoPhillips sold its interests in the San Juan Basin to an affiliate of Hilcorp Energy Company for a sum of $3 billion. Of the deal value, $2.7 billion will be received in cash and the remaining amount will be a contingent payment of up to $300 million, beginning 2018 for a term of six years. The company’s San Juan Basin assets produced 124 thousand barrels of oil equivalent per day (BOED), of which roughly 80% was natural gas.

On analyzing the transactions, we believe that both the deals are aligned with ConocoPhillips’ strategy to reduce its global footprint by 50%, particularly in the North American gas markets, and concentrating on strategic and high-margin markets. The company anticipated that the two deals will lower its average cost of supply from $40 per barrel at the beginning of the year to around $35 per barrel by the end of this year. In the current volatile price environment, a reduction in the cost of supply will allow the company to improve its margins and returns.

On the flip side, the transactions will bring down the company’s proved reserves from 6.4 billion boed to 4.5 billion boed, and will trim its 2017 production from the expected 1,555 MBOED (mid-point) to 1,160 MBOED. That said, the closure of these sales will generate more than $16 billion of funds during the year, which it plans to utilize to finance its expansion needs, and enhance its capital structure (described earlier). The deals are expected to close in the second and the third quarter of 2017 respectively, subject to receiving all regulatory clearances.

Thus, we expect 1Q’17 to turn out to be a crucial quarter in the turnaround of ConocoPhillips. The recovery in commodity prices, coupled with its focus towards high-margins plays, and divestment of non-strategic assets, will allow the company to improve its profitability and shareholder value in the current as well as forthcoming quarters.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap