Capital One Stock Is Trading Above Its Near Term Potential

[Updated 04/01/2021] Capital One Update

Having gained close to 200% since the March 23 lows of last year, at the current price near $127 per share, we believe Capital One’s stock (NYSE: COF) has some room for a price correction. Capital One, an American bank holding company specializing in credit cards, auto loans, and banking, has seen its stock increase from $43 to $127 off the March 2020 bottom compared to the S&P 500 which gained almost 80% – the stock is leading the broader markets by a considerable margin and is trading 21% above its pre-Covid-19 peak in February 2020. Part of this meteoric stock rise was in the recent months – up 29% YTD, after the bond yields in the U.S saw some upward momentum. The effect was also felt on other financial stocks, with the benchmark Dow Jones U.S. Banks Index gaining 24% YTD. Along with this, the company outperformed the consensus estimates for revenues and earnings in the third and fourth quarters of 2020. Further, it reduced its provisions for credit losses in both quarters on a year-on-year basis, boosting the firm’s profitability. A drop in provisions also signifies that COF perceives some improvement in the loan default risk. Additionally, consumer spending levels saw some recovery in the second half of 2020. All these factors have helped in shaping a positive investor sentiment toward Capital One stock.

Capital One’s revenue of $28.5 billion for the full year 2020 was marginally lower than the 2019 figure. This was primarily due to a 2% drop in net interest income (NII) driven by lower yields on average earning assets, a decline in outstanding domestic card loans, and higher deposit balances. However, the weakness in NII was almost offset by a 7% y-o-y growth in non-interest income, mainly due to an unrealized valuation gain of $535 million on equity investment in Snowflake Inc. On the profitability front, COF’s net income slipped almost 50% y-o-y to $2.7 billion. This drop could be attributed to a build-up in provisions for credit losses from $6.2 billion to $10.3 billion coupled with higher compensation costs.

- Capital One Stock Gained 44% In The Last 6 Months, What’s Next?

- Up 40% Since The Beginning Of 2023, How Will Capital One Stock Trend After Q4 Earnings

- Up 25% Since The Beginning Of 2023, Will Capital One Stock Continue To Rally?

- Capital One Stock Gained 14% YTD And Outperformed The Estimates In Q3

- What To Expect From Capital One Stock?

- Capital One Missed The Consensus In Q1, What’s Next?

Net Interest Income contributes around 80% of the total revenues for Capital One. Hence, changes in interest rates can have a significant impact on COF’s top-line. Further, the consumer spending level is also a very important factor that directly impacts the new loan issuance and card transaction volumes. The transaction volume and outstanding loans have recorded some improvement over the recent quarters and we expect them to further improve with recovery in the economy. That said, the lower interest rate environment has troubled the company in 2020 and is unlikely to see an immediate recovery to the pre-Covid-19 levels. Overall, Capital One‘s revenues are likely to touch $29 billion in FY2021. Additionally, COF’s P/E multiple changed from just above 6x in 2018 to close to 19x in 2020. While the company’s P/E is around 25x now, there is a downside risk when the current P/E is compared to levels seen in the past years – P/E multiple of around 19x at the end of 2020. Our dashboard “What Factors Drove 68% Change In Capital One Stock Between 2018-End And Now?” provides the key numbers behind our thinking.

[Updated 01/04/2021] Gaining 125%, Capital One Stock Is Done Charging Higher

After more than a 125% gain since the March 23 lows of this year, at the current price of $99 per share, we believe Capital One Stock (NYSE: COF) has a limited upside. Capital One, the credit card giant, has seen its stock rally from $43 to $99 off the recent bottom compared to the S&P which moved around 70% – so the stock is leading the broader markets by a huge margin. The stock growth could be attributed to a Q3 2020 earnings beat and improvement in consumer spending, despite the lower interest rate environment – cumulative nine months 2020 revenues of $21.19 billion were marginally ahead of the year-ago period. However, the provision for credit losses increased to $10 billion for the nine months as compared to $4.4 billion in the year-ago period, mainly due to the higher risk of loan defaults on outstanding loans.

Capital One’s stock has partially reached the level it was at before the drop in February due to the coronavirus outbreak becoming a pandemic. This makes the COF stock fully valued, as the demand will likely be lower than last year.

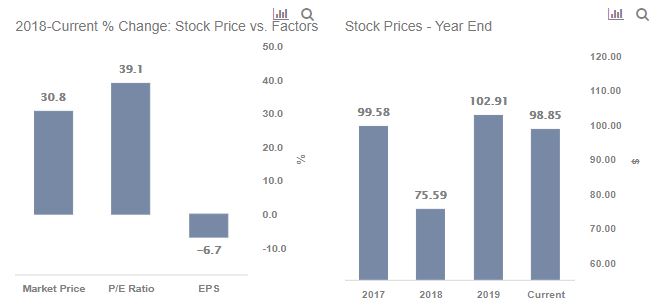

The company’s revenues increased by a meager 2% over 2018-2019, however, the net income figure decreased by 8% over the same period. This was mainly due to higher compensation costs which reduced the net income margin from 21.4% in 2018 to 19.4% in 2019.

While the company has seen slow growth in revenue over 2018-2019, its P/E multiple has increased. We believe the stock is unlikely to see significant upside after the recent rally and the potential weakness from a recession-driven by the Covid outbreak. Our dashboard “What Factors Drove 31% Change In Capital One Stock Between 2018-End And Now?” has the underlying numbers.

Capital One’s P/E multiple has changed from just above 6x in FY 2018 to around 9x in FY 2019. The company’s P/E has benefited from the Q3 earnings beat and is just below 9x now. This leaves limited scope for upside when the current P/E is compared to levels seen in the past years.

So Where Is The Stock Headed?

While Capital One’s top-line suffered in Q1 and Q2 2020 due to the Covid-19 crisis, the revenues bounced back in Q3 driven by a 49% y-o-y growth in non-interest income. Overall, the company’s cumulative revenues for the first nine months were marginally ahead of the previous year’s figure. That said, the consumer spending in the U.S, though improved, is still behind the pre-Covid-19 levels and the recovery is expected to take some time. Hence, Capital One’s revenues are unlikely to see significant growth in the near term. Additionally, the economic slowdown has increased the risk of loan defaults, leading to a sizable build-up in provisions for loan losses. This will further hamper the company’s growth prospects. Overall, Capital One stock has limited upside potential in the near term.

The actual recovery and its timing hinge on the broader containment of the coronavirus spread. Our dashboard Trends In U.S. Covid-19 Cases provides an overview of how the pandemic has been spreading in the U.S. and contrasts with trends in Brazil and Russia. Following the Fed stimulus — which set a floor on fear — the market has been willing to “look through” the current weak period and take a longer-term view. With investors focusing their attention on 2021 results, the valuations become important in finding value. Though market sentiment can be fickle, and evidence of an uptick in new cases could spook investors once again.

Think Bitcoin could disrupt the banking industry? Looking for upside from Bitcoin adoption, without buying into the cryptocurrency itself? Check out our theme on Cryptocurrency Stocks

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams