Citigroup Stock Is Trading 25% Below Its Fair Value

[Updated 01/22/2021] Citigroup Update

Citigroup stock (NYSE: C) is currently trading close to $62, which is 75% above the March 23 lows of the last year and almost 21% below its pre-Covid peak. Trefis estimates Citigroup’s valuation to be around $78 per share – approximately 25% above the current market price. While the bank reported an earnings beat in the recently released fourth-quarter results, its revenues missed the consensus estimates. It reported total revenues of $16.5 billion – down by 10% y-o-y. While the Institutional Client Group (ICG) reported a meager 1% y-o-y drop driven by lower revenues in investment banking and treasury & trade solutions, closely matched by growth in Sales & Trading, the top-line mainly suffered due to a 14% decrease in the Global Consumer Banking segment. This could be attributed to a lower interest rate environment and a decline in card volumes.

Citigroup reported revenues of $74.3 billion for the full year 2020 – at the same level as the year-ago period. It was led by the growth in its ICG segment (sales & trading and investment banking businesses), which compensated for the weakness in its core banking revenues. We expect the core banking revenues to continue to suffer in FY2021, due to the lower interest rate environment and the negative impact of the Covid-19 crisis on consumer demand. Further, the sales & trading and investment banking revenues are expected to normalize in the subsequent quarters. This is likely to restrict Citigroup’s revenues to around $70.3 billion in FY 2021 – down by 5% y-o-y.

The earnings figure suffered in 2020, due to the sizable build-up in provisions for credit losses to counter the risk of loan defaults on the bank’s loan portfolio – EPS down 39% y-o-y to $4.87. The risk of loan default is tied to the economic slowdown. As the economic conditions improve, the financial health of the customers is likely to recover, reducing the risk of loan defaults and boosting Citigroup’s profitability. We expect the EPS figure to remain around $6.88 in FY2021. Additionally, the bank is likely to start its share repurchase program from the first quarter of 2021. Overall, the EPS of $6.88 coupled with the P/E multiple of just above 11x will lead to a valuation of around $78.

[Updated 12/10/2020] Citigroup Stock Still Has Some Potential

While Citigroup stock (NYSE: C) has gained around 70% since the March bottom, it is still down 25% YTD. Trefis estimates Citigroup’s valuation to be around $65 per share – around 10% above the current market price. Citigroup, a leading global financial services holding company that does business in over 160 countries, holds a sizable portfolio of outstanding loans and is very sensitive to changes in interest rates. In its recently released third-quarter results, Citigroup reported Total Revenues of $17.3 billion, down by 7% y-o-y. Although the Institutional Client Group (ICG) reported a 5% y-o-y growth mainly driven by higher Sales & Trading and investment banking revenues, it was more than offset by a 13% decrease in the Global Consumer Banking segment due to a decline in net interest income. The lending industry has suffered after the announcement of a zero-rate policy by the Federal Reserve in response to the Covid-19 pandemic – It decreases the net interest margin that banks earn by taking in deposits and offering loans.

We expect Citigroup’s revenues to see some growth in the last quarter results, mainly driven by a slight improvement in the consumer banking segment and the continued rally in sales & trading business. It is likely to report $74.3 billion in revenue for FY 2020 – marginally lower than the year-ago figure. Further, its net income margin is likely to drop from 24.5% in 2019 to 10% in the current year due to a jump in provisions for credit losses, decreasing the EPS figure to $3.44 for FY 2020. Thereafter, revenues are expected to decline to $71.2 billion in FY2021, mainly driven by a decline in investment banking and sales & trading business. However, the EPS figure is likely to improve to $6.09 due to a favorable decrease in provisions for credit losses. This coupled with the P/E multiple of just below 11x will lead to a valuation of around $65.

[Updated 7/22/2020] Should You Invest In Citigroup Stock?

Citigroup stock (NYSE: C) lost more than 55% – dropping from $79 at the end of 2019 to around $35 in late March – then spiked 46% to around $52 now. Despite this, the stock has lost 34% of its value so far this year.

This can be attributed to 2 factors – The Covid-19 outbreak and economic slowdown meant that market expectations for 2020 and the near-term consumer demand plummeted. This could cause significant losses for businesses and individuals alike, impacting their loan repayment capability and exposing Citigroup to sizable loan losses. The multi-billion-dollar Fed stimulus provided a floor, and the stock recovery owes much to that.

But this isn’t the end of the story for Citigroup stock

Trefis estimates Citigroup’s valuation to be around $61 per share – about 20% above the current market price – based on an upcoming trigger explained below and one risk factor.

The trigger is an improved trajectory for Citigroup’s revenues over the second half of the year. We expect the company to report $74.8 billion in revenues for 2020 – slightly higher than the figure for 2019. Our forecast stems from our belief that the economy is likely to open up in Q3. As the lockdown restrictions are easing in most of the world, consumer demand is likely to pick up, leading to improvement in business spending. Further, the bank’s Sales & Trading operations have driven positive revenue growth in Q1 and Q2 due to higher trading volumes, followed by higher growth in the investment banking business due to a jump in underwriting revenues after the Fed stimulus. This has largely offset the impact of weak revenues in other segments. Although the trading income is expected to decline as compared to the first two quarters, it is likely to drive positive growth in the second half as well. Overall, we see the company reporting an EPS in the range of $3.87 for FY2020.

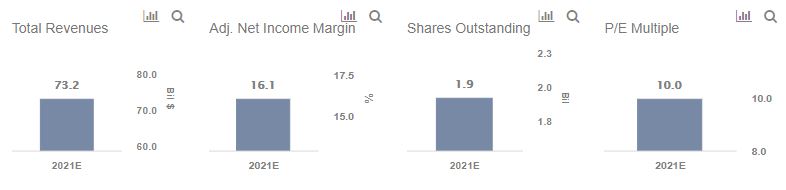

Thereafter, Citigroup’s revenues are expected to slightly reduce to $73.2 billion in FY2021, mainly due to a drop in sales & trading business. Further, the net income margin is likely to improve due to a decline in provisions for credit losses, leading to an EPS of $6.13 for FY2021.

Finally, how much should the market pay per dollar of Citigroup’s earnings? Well, to earn close to $6.13 per year from a bank, you’d have to deposit about $675 in a savings account today, so about 110x the desired earnings. At Citigroup’s current share price of roughly $51, we are talking about a P/E multiple of just over 8x. And we think a figure closer to 10x will be appropriate.

That said, banking is a risky business right now. Growth looks less promising, and near-term prospects are less than rosy. What’s behind that?

The economic downturn could cause significant losses for businesses and individuals alike, impacting their loan repayment capability. This could result in sizable losses for Citigroup, as it has a substantial loan portfolio of consumer and commercial loans. This is also evident from a huge jump in the bank’s provisions for loan losses in Q1 and Q2. Further, as the economy slows down, it will likely become more expensive for the bank to attract funding, negatively impacting all its operations.

The same trend is visible across Citigroup’s peer – Morgan Stanley. Its revenues are expected to benefit from positive growth in its trading arm and investment banking business in FY2020. This would explain why Morgan Stanley’s stock currently has a stock price of over $52 but looks slated for an EPS of around $5.02 in FY2021 (for a P/E multiple of nearly 11.5x).

What if you’re looking for a more balanced portfolio instead? Here’s a high quality portfolio to beat the market, with over 100% return since 2016, versus 55% for the S&P 500. Comprised of companies with strong revenue growth, healthy profits, lots of cash, and low risk, it has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Team