Baidu Stock: China’s Google Rival Has More Upside Despite A 50% Rally

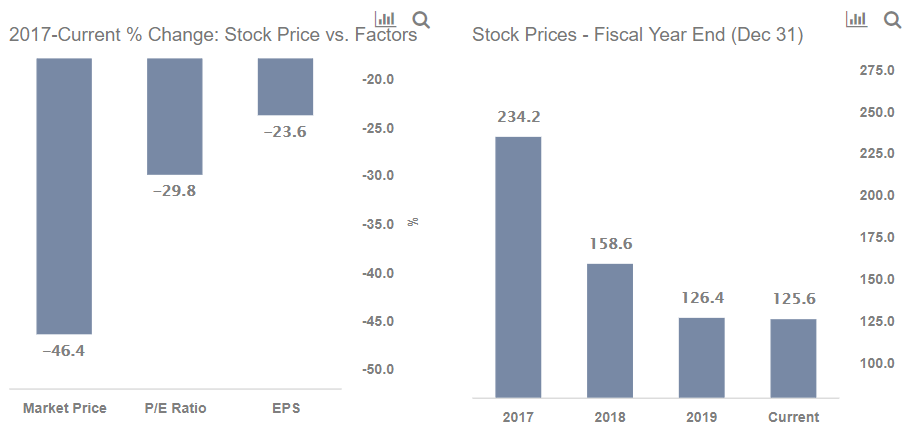

After a 50% rise since the March lows of this year, at the current price of around $125 per share, we believe Baidu’s stock (NASDAQ: BIDU) has more to go. China’s leading internet search provider has seen its stock underperform through the coronavirus crisis, with a 1% decline year-to-date (compared to a 4% growth in the S&P). Baidu’s stock is also about 46% lower than it was at the end of 2017, a little over 2 years ago. Our dashboard What Factors Drove 46% Decline In Baidu Stock Between 2017 And Now? explains more with underlying numbers.

Large concerns over competition in the China advertising market from rivals such as ByteDance, its increasing dependence on its unprofitable streaming video iQiyi for revenue growth, and the popularity of apps such as Tencent’s WeChat – has led the company’s stock to decline for the third year in a row. Although the company’s stock decline has been partly self-inflicted, the overall online advertising market in China itself has been softening since the country’s economy started to slow amid U.S. trade tensions since last year. It should be noted that Baidu generates the majority of its revenues from online ads. And the data it collects from users in this process, along with its presence and expansion in smart speakers, virtual assistants, and driverless cars – promises a potential growth trajectory in the Artificial Intelligence (AI) market.

Although Baidu’s revenues saw an 18% growth during the 2017-2019 period, this growth was largely offset by a 24% decrease in profitability as adjusted net income margin declined from 26.2% in 2017 to 16.9% in 2019. The stock price declined largely during this period due to lower margins. This fall led to a decline in the P/E multiple from 24x in 2017 to 17x in 2019. Although the multiple currently stands at 2019 levels, we expect it to grow further going forward on the back of its investments in the AI industry.

So how has Coronavirus impacted the stock?

In Q1, Baidu’s revenue declined 7% year-over-year (y-o-y) to $3.18 billion, with shelter-in-place orders having a marked impact on sales for the internet company. While its core business revenue (flagship search, feed, and Artificial Intelligence businesses) was down 13% y-o-y, iQiyi revenues were up 35% y-o-y in Q1. However, adjusted pre-tax operating earnings grew 38% y-o-y on the strength in margin figures.

The internet company was able to transition successfully toward mobile devices. Daily active user counts were up 28% y-o-y to 222 million, with in-app search queries soaring 45% y-o-y. Going forward, this growth could also likely offset the headwind of a weak online advertising market.

For Q2, Baidu is guiding to revenues of about $3.5 billion – $3.9 billion, representing growth of -5% to 4% y-o-y. That assumes that core revenue growth will range from -8% to 2% y-o-y. Baidu isn’t back to where it was at its peak, but it is taking some steps in the right direction as China starts to breathe new life into its economy. The company has been investing heavily in its cloud-computing segment in recent years and announced plans to deploy 5 million intelligent cloud servers by 2030 and train 5 million AI experts over the next 5 years. All its AI investments are not generating meaningful revenue for the company yet, but are expected to strengthen its business in the long-term.

Want out-performance? Try guessing the % returns for our Pershing-inspired portfolio – based on billionaire Bill Ackman’s firm Pershing Square – vs. the S&P over the last 1 week, 1 month, 3 months, YTD or even 3 years. Our portfolio combines high growth, quality, and risk mitigation criteria in an interesting way.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams