Alcoa Overvalued After 120% Recovery?

After a formidable 120% rise since the March lows of this year, at the current price near $11 per share we believe Alcoa’s stock (NYSE: AA) has surpassed its near-term potential. Alcoa’s stock has rallied from $5 to $11 off the recent bottom compared to the S&P 500 which increased 33% during the same period. The stock was able to beat the broader market in the last 3 months as aluminum prices rebounded and started to rise since April. With the US government announcing a string of measures along with stimulus packages announced in other economies to keep businesses afloat, along with the Chinese economy opening up which led to expectations of a rise in aluminum demand. However, the stock is down 79% from levels seen in early 2018, a little over 2 years ago.

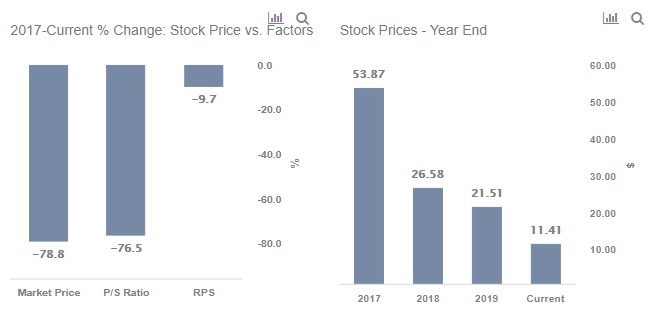

Though Alcoa’s stock is still lower than the level at which it was in early February 2020 (before the crisis), we think it is slightly above its fair value, as, in reality, demand and revenue will likely be lower than last year. Our dashboard What Factors Drove -79% Change In Alcoa Stock Between 2017 And Now? provides the key numbers behind our thinking.

Some of the stock decline of the last 2 years is justified by the roughly 10.5% decrease in Alcoa’s revenues from 2017 to 2019, while its operations turned loss-making in 2019 after reporting profits in 2017 and 2018. While Alcoa’s revenue declined in 2019 and has reached below its 2017 level, the P/S multiple has seen a continuous decline over the years. We believe that the stock is unlikely to see a further upside after the recent rally and the potential weakness from the recession driven by the Covid outbreak.

Alcoa’s P/S multiple declined from 0.9x in 2017 to 0.4x in 2019. While the company’s P/S is now 0.2x, we do not think it has much upside currently, and in the near term is likely to remain around the current level. A lower multiple would reflect expectations of lower revenue in the near term as under the new operating model announced by Alcoa, it has put 1.5 million metric tons of aluminum smelting capacity under review, which will lead to lower shipments in the future.

What’s the likely trigger for a downside?

As increasing number of steel players are shedding capacity, and demand from automobiles being modest, China has increased its exports of semi products at a lower price, which has, in turn, led to a decline in the price of primary aluminum products worldwide. On top of this, the global spread of coronavirus has led to lockdown in various cities across the globe, which has affected industrial and economic activity. The aluminum demand from industry players affects global aluminum price levels, in turn impacting the company’s price realization for its products. Lower demand from construction and automobile players, has led to a drop in global aluminum prices from $1,820/ton in January 2020 to $1,570/ton in June 2020.

This was reflected to a certain extent in the company’s Q1 2020 results, with the company reporting a 12.4% y-o-y drop in total revenues. But we believe Alcoa’s Q2 results in July will confirm the complete impact of the drop in aluminum and alumina prices with a greater hit to its revenue.

However, over the coming weeks, we expect continued improvement in demand and subdued growth in the number of new Covid-19 cases in the U.S. to buoy market expectations. Following the Fed stimulus — which set a floor on fear — the market has been willing to “look through” the current weak period and take a longer-term view. With investors focusing their attention on 2021 results, the valuations vs historic valuations become more important in finding value.

Even if we see signs of abatement of the crisis by the end of June 2020, we do not believe Alcoa’s stock has an upside in the near term from its current level, as it has already increased sharply in the last 3 months. Based on Alcoa’s valuation, Trefis has a fair price estimate of $9 per share for Alcoa’s stock, slightly lower than its current market price.

While Alcoa’s stock could see a marginal downside, here’s an insight into how rival Rio Tinto’s stock has performed.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams