With Smartphone Business Floundering, Is Samsung Becoming A Semiconductor Company?

Samsung Electronics (PINK:SSNLF) is at a crossroads. Its flagship smartphone business has been struggling, with significant market share declines (down to about 22% in Q2’15 from 30%+ in 2013) and thinning margins, amid intense competition from Apple (NASDAQ:AAPL) as well as low-cost Chinese vendors. [1] On the other hand, its semiconductor business – the world’s second largest, behind Intel (NASDAQ:INTC) – has been performing very well, driven by strong demand for memory products and advances in its logic chip manufacturing foundries. Given that its smartphone troubles run fairly deep, some investors and analysts are betting that Samsung will shift its focus primarily to semiconductors, given the thicker margins and the company’s inherent competitive advantages (related: Samsung Q2 Review: The Smartphone Turnaround Isn’t Going As Planned). While the company has certainly strategically emphasized its semiconductor segment of late, the smartphone business remains of vital importance for Samsung. Accordingly, it is unlikely that the company’s focus shifts substantially from the smartphone space in the near term. Below we discuss why.

See our full analysis for Samsung Electronics

Trefis has a $1,250 price estimate for Samsung, which is over 25% ahead of the current market price.

- A 3x Expected Rise In Mounjaro Sales Is Likely To Drive Eli Lilly’s Q1

- What Should You Do With Danaher Stock At $250 After Q1 Beat?

- Will A Macau Recovery Drive MGM Stock Higher Following Q1 Results?

- Lockheed Martin Stock Will Likely Remain In Focus After A Stellar Q1

- Up 17% YTD, What To Expect From eBay Q1 Results?

- Rising 21% This Year, What Lies Ahead For Exxon Stock Following Q1 Earnings?

Semiconductor Business Is Volatile, Capital Intensive

Samsung’s semiconductor business can be broadly broken into three segments – the core DRAM memory business (48% of fiscal 2014 semiconductor revenue, by our estimates), the NAND memory business (26%) and logic chips and other products (26%). All three segments have been doing well in recent quarters. While the DRAM business is benefiting from higher pricing – on account of careful capacity management across the industry and sales of higher-value products – the NAND business is being driven by growth in demand from mobile devices and SSD sales. The logic-chip unit, which primarily manufactures microprocessors for third parties and for Samsung’s own mobile unit, has seen an increase in profitability led by the rollout of the 14-nm FinFET process technology. This has reportedly helped the company win business from Apple for the next iteration of the iPhone, as well as from other semiconductor companies such as Nvidia (NASDAQ:NVDA) and Qualcomm (NASDAQ:QCOM). The semiconductor division has been more profitable than the smartphone business of late, accounting for close to half the company’s operating profits in the second quarter of 2015. Semiconductor revenues grew by 15% y-o-y during Q2 – while mobile revenues declined by 7% in the same period – and profits from the division are now greater than those of the smartphone division (about 23% higher in Q2).

However, despite the strong recent growth, the semiconductor division does face a few challenges. Unlike asset-light fabless semiconductor players, Samsung incurs massive capital expenditures for its semiconductor business. Samsung’s semiconductor capex has been the highest in the chip industry for the last five years, and the company is expected to invest up to $15 billion in 2015, according to an estimate from Digitimes Research. [2] In comparison, we estimate that the mobile division’s capex stands at under $4 billion.

Moreover, the memory business is cyclical, and companies face boom and bust phases for their products. When times are good, profits soar, owing to better pricing and operating leverage benefits. However, the down cycles can be brutal. With the high fixed costs and low variable costs of semiconductor manufacturing, downturns can pummel margins. For instance, we estimate that Samsung’s per-gigabit DRAM pricing fell by over 55% between 2010 and 2012. Samsung’s memory business does have a tech edge in many areas, but this doesn’t fully insulate the company from the risks of the largely commoditized memory market.

In the logic chip space, Samsung’s biggest strengths lie at the foundry level, relating to fabrication and process technologies (the ability to miniaturize and pack more transistors into a chip) and a bulk of the company’s processor revenues come from contract manufacturing for third parties. This can be a lumpy business, as device manufacturers occasionally switch suppliers over their product life cycles. For instance, in 2014 Samsung apparently lost significant ground to rival TSMC as a supplier of Apple’s A-series application processors, causing the company’s logic chip revenues to fall by close to 25%. [3] While Samsung is making progress with its own logic chip designs – with products such as the Exynos, used in the company’s latest S and Note smartphone flagships – it has yet to gain significant traction in selling them to other vendors.

Mobile Business Provides Revenue Base For Components Segment

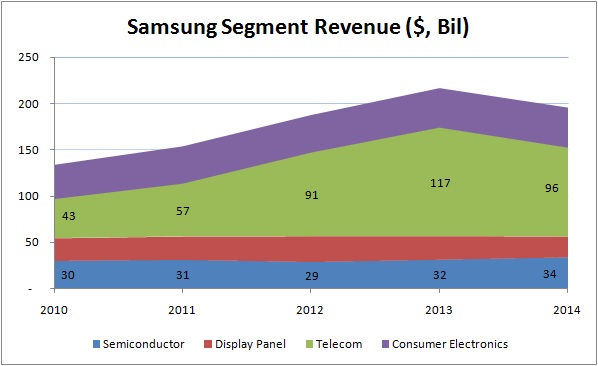

Samsung’s mobile division has been its biggest earnings driver in recent years, as the company transformed itself from a feature phone manufacturer into the world’s largest smartphone vendor. Mobile revenues grew from around $43 billion in 2010 to about $96 billion in 2014 (smartphone revenues peaked in 2013), a CAGR of about 23%, and accounted for about 85% of Samsung’s total top line growth during the period. Although smartphone sales have slowed considerably over the last year, the segment remains Samsung’s biggest and most valuable business, by our estimates. Moreover, it remains a demand driver for the semiconductor business. While detailed breakdowns are not reported, inter-company revenues from the semiconductor business stood at about $30 billion in 2014, accounting for more than 45% of total semiconductor sales. It’s safe to assume that Samsung smartphones account for much of this revenue. [4]

For example, Samsung sources most of the major cost drivers for its latest Galaxy S6 Edge flagship device from its internal components business – display, app processor, DRAM and NAND. The company is also reportedly using its own modem chips rather than Qualcomm chips on some variants of its new flagship handsets. Considering the phone’s estimated $284 bill of materials, this means that the semiconductor division alone provides at least 34% of materials by value, and the number jumps to about 64% if we account for the screens provided by the hardware segment. [5] While these intercompany revenues are not reflected on Samsung’s consolidated top line, they do still provide a significant source of demand and help company-wide operating margins.

What Does This Mean For Samsung?

Although we believe that semiconductors will account for most of Samsung’s growth going forward, the mobile business still provides the foundation of the firm’s earnings and valuation. It remains in the company’s best interest to stabilize handset shipments, even if it means re-examining its pricing strategy for its newer (mostly well-reviewed) handsets, since a further drop in sales could have ripple effects across the company (related: Samsung Galaxy Note 5 And The Case For Lower Device Pricing). The bottom line: Samsung’s semiconductor business has been performing strongly, but the company will need to get its smartphone business back in order, or the stock could see further headwinds in the near term.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes:- Worldwide Smartphone Market Posts 11.6% Year-Over-Year Growth in Q2 2015, the Second Highest Shipment Total for a Single Quarter, According to IDC, July 2015 [↩]

- Digitimes Research: Samsung semiconductor capex to reach record high in 2015, Digitimes, April 2015 [↩]

- Samsung’s Other Weakness: It Is Selling Fewer Chips to Apple, WSJ, August 2014 [↩]

- Samsung 2014 Annual Report [↩]

- Samsung Galaxy S6 Edge Teardown, IHS, April 2015 [↩]