A U.S. Economy Snap Shot, Part 1: The Growth Story In 2015

Even almost a decade after the sub-prime mortgage crisis, the U.S. hasn’t been able to return to pre-crisis growth levels. The Great Recession, as the 2007 crises is famously dubbed, was a result of a mortgage-driven credit crisis as too much was lent to sub-prime borrowers, in large part to satisfy demand for synthetic credit paroducts. While it is believed that 2009 marked the end of the crisis, its ripple effects continue to impact the U.S. even now, as it struggles to maintain its dominance in the changing world economy.

Through the first nine months of the year 2015, the U.S. economy expanded at a sub-par rate of 2.2% year over year. Throughout last year, the country confronted weakened exports stemming from the strong dollar, falling commodity prices due to the Chinese slowdown, and a broader global weakening in demand as commodities-dependent emerging market economies (EMEs) lost steam. Even the stock markets, which had rallied for 6 years continuously, finished flat in 2015.

In this note, we discuss the broad themes that emerged and affected the U.S. in 2015 and what they mean for the economy.

- What’s Next For JetBlue Stock After A Sharp 19% Fall Post Q1 Results?

- Is Kimberly-Clark Stock Fairly Valued At $135 After A Solid Q1?

- How Will AMD’s AI Business Fare In Q1?

- Up 9% Year To Date, Will Chevron’s Gains Continue Following Q1 Results?

- Earnings Beat In The Cards For Honeywell?

- Higher Keytruda Sales To Drive Merck’s Q1?

Broad Themes Of 2015

The year began at an exceptionally slow pace with the U.S. economy shrinking 0.64% in the first quarter. This was attributable mainly to poor weather conditions and a small inventory build in the previous quarter. However, in the second quarter, there were some signs of recovery as consumer spending grew and GDP growth touched 3.9%. Unfortunately, the recovery was short lived as, as the economy growth fell below 2% in Q3.

There were several macroeconomic and microeconomic factors at play, which made 2015 an unspectacular, if foundationally strong year for the U.S.

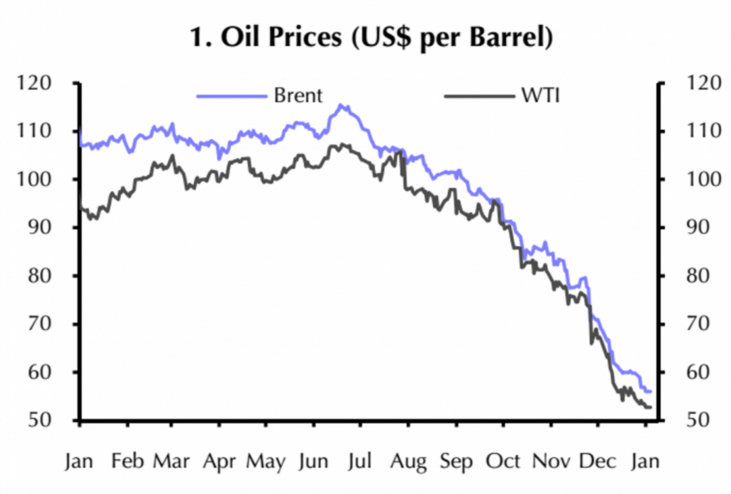

- The slump in oil prices which began in 2014, intensified in 2015, causing prices to sink to an 11-year low in December 2015. The plummeting oil prices were expected to be a boon for the economy as it effectively meant higher consumer disposable income. [1] Instead, consumers decided against spending the extra cash in hand in favor of savings, which rose to 5.5% in November 2015 as opposed to 4.6% in the year ago period. This suggests that consumers’ faith in the U.S. economic recovery isn’t completely restored yet. However, since oil prices have been low for some time now, people may think of the development as more long term in nature and spend the extra income in 2016.

- October marks the 23rd consecutive month in which home values rose. [2] Aggregate U.S. home values grew by 4.1% year on year in 2015 to an estimated $28.5 trillion overall, according to real estate research firm Zillow. Home prices rose 5.2% in November 2015, compared to year ago period, as per data provided by National Association of Realtors. Factors that are boosting house prices include a decrease in the number of house listed for sale (i.e., less supply than demand), the availability of cheap mortgages and recent increases in residential construction (including single family houses). In contrast, the number of houses sold in November dropped by 10.5% on a seasonally adjusted basis, mainly due to a federal rule change that’s lengthening the process of closing on a sale. In 2016, house sales may slow down due to the higher cost of borrowing.

- Consumer demand, which is the chief engine of the U.S. economy and accountable for nearly 70% of economic activity, rose about 3% in the third quarter year over year. ((Consumer, business spending support third quarter growth, Thomson Reuters, December 2015)) This may be due to the improvement in consumer sentiment which in turn stems from an improved labor market. The labor market was resilient in 2015, and successfully added 12 million jobs. Unemployment came down to 5% from a high of 10% in 2009. Even wages registered moderate growth at 2.3% year over year in November. According to the Conference Board, the consumer confidence index rose to 96.5 in December from 92.6 in November, signifying consumers’ assessment of present and future conditions bettered. With a stronger dollar denting the demand of U.S. made goods, it is imperative that consumer demand continues its momentum in 2016.

- The emerging market economies experienced weakness in 2015. Notably China’s GDP growth slowed from the targeted 7.5% to 6.9%. Moreover, Europe’s recovery remained sluggish throughout 2015 with extremely high levels of unemployment (10.7% in 2015). This, coupled with a strong dollar, resulted in American exports becoming more expensive for overseas buyers. Overall, the first 10 months of 2015 witnessed a 4.3 % drop in exports, according to the Census Bureau. Furthermore, low global commodities prices and tumbling profits due to oil slump, curbed business spending on factories and energy infrastructure.

- The stock market did not make any meaningful gains in the year 2015, despite major indexes hitting new highs. After six years of bull-run in the stock market, the Dow fell 13% from its July high to an August low of 15,666. (It has since recovered some lost ground.) The slump in oil prices, a slowdown in China, and the strong dollar compressing exports, were all a drag on corporate earnings, causing the stock market to finish the year flat. According to experts, amid continued economic growth, robust consumer spending and reasonable stock valuations, markets may see a gain in late single digits in 2016.

- Lastly, the Fed raised interest rates in December 2015 for the first time in nearly a decade. This move demonstrates that the Fed has confidence in the U.S. recovery. However, it has caused a lot of worry in the economy, even though the rise is only by a quarter of a percentage point. The hike’s immediate effect is an increase in the cost of borrowing, which may limit the demand in the housing market. Moreover, already low capital expenditure due to downturn in the energy sector may dampen further. Increase in interest rate will also result in a further strengthening of the dollar, increasing the limitations on exports. Many believe that the hike may curtail GDP growth and push the economy back into a recession, instead of fighting inflationary pressure, as the Fed believes.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research

- Delayed ignition from cheap fuel in U.S., Wall Street Journal, December 2015 [↩]

- U.S. Home Values Exceed Last Decade’s Peak, themortgagereports.com, January 2016 [↩]