Starbucks Q4 Fiscal 2015 Earnings Preview: Three Drivers To Look Out For

Starbucks Corporation (NASDAQ: SBUX), the leader in the coffee industry, is scheduled to report its Q4 earnings report for the fiscal 2015 on October 29. [1] Market analysts are expecting the company to post an EPS of 43 cents, up 16% year-over-year (y-o-y), on a revenue growth of 17% y-o-y. [2] With strong coffee sales, driven by new menu additions and reserve coffee items, as well as strong market share in the single-serve market, the company might post yet another solid comparable sales growth, and end its fiscal year 2015 on a stronger note. Perhaps the key factors that the investors would be looking forward to in this quarterly result are:

- Comparable sales growth

- Digital Growth (Mobile ordering and Payment)

- Performance in the single-serve market

See our full analysis for Starbucks Corportion

Look Out For Comparable Sales Growth

- Down 7% Since 2023, Can Starbucks’ Stock Reverse This Trend Post Q1 Results?

- Down 26% From Its Pre-Inflation Shock High, What Is Next For Starbucks Stock?

- After 6% Drop This Year, Pricing Growth To Bolster Starbucks’ Q4

- Can Starbucks Stock Return To Pre-Inflation Shock Highs?

- Starbucks’ Stock To See Little Movement Past Q3?

- Starbucks Stock To Likely Trade Lower Post Q2

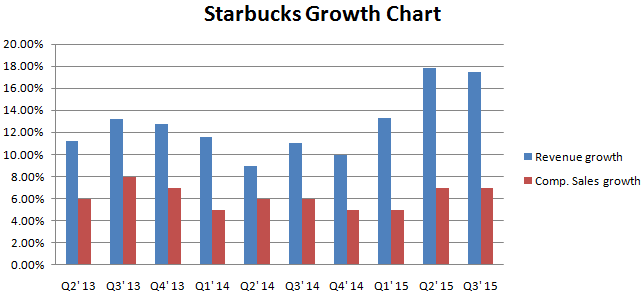

For the last 4 quarters, the coffee giant has been posting EPS growth in-line with market expectations, with double digit y-o-y revenue growth in 9 of the last 1o quarters, as well as high single digit comparable store sales growth over the same period.

As a result, the company’s stock has risen more than 60% since January 2014, with positive sentiments among the investors. The company has not even posted one moderate result over the past 20 months, and with accelerated advancements in the operations, such as the introduction of Starbucks Roastery and Tasting rooms, it is more likely for the company to post another strong comparable store sales growth. One of the key factors that drive comparable sales growth for the company is its customer traffic.

Now, the first half of this year witnessed a decline in the prices of coffee, as the coffee December futures contract dropped 13% from June’15 to August’15. Despite the decline, Starbucks raised the menu price on some of its items in July, which effectively cost 1% more to the customers. [3] Starbucks’ coffee items are among the most expensive in-store coffee items in the industry. Furthermore, the company blamed the increasing labor and rent expenses as the reason for the hike.

The interesting thing to note will be whether or not the customers take this positively. A decline in customer traffic would significantly impact the comparable store sales growth for the company. So, the question that arises is if slowness in customer traffic would offset the increase in check. And if so, then will it be enough to drag the comparable sales growth below 5%. Moreover, it makes it tough for the company to post yet another high single-digit comparable sales growth considering the y-o-y comparison is extremely strong.

Trefis estimates the beverage spend per customer visit to rise by 1% y-o-y in 2015, whereas average daily customer per store is estimated to increase by 2% in 2015. The impact of these drivers on Starbucks’ valuation can be analyzed below:

Digital Growth: How Big Can It Get?

Starbucks’ mobile payment and ordering initiative is turning out to be a huge success for the company, attracting more customers every quarter. This innovative feature is now available in nearly 4,000 of the company’s U.S. company operated stores, and will be available throughout the country by the end of the holiday season. [4] As a result, the impact of this initiative will be clearer in the upcoming quarterly result.

There is no doubt that this feature will improve Starbucks’ revenue growth, as well as its margins. As this feature makes it convenient for the customers to order and pay, it will attract more customers, finally translating to increase in customer traffic. Furthermore, operational efficiency and reduced credit card processing charges might boost the margins for the company-operated stores.

With this feature expanding to more stores nationwide, and probably across borders in the coming years, we can expect further improvement in the revenue growth and increased efficiency.

Strength In Single-Serve Market

Recently, UBS analysts released a report stating that Starbucks’ industry-wide market share in the K-Cups segment rose by 40 basis points to 16.7%. [5] Starbucks’ single-serve sales rose nearly 41% y-o-y for the one month period ended September 5, 2015, primarily due to volume growth of 53% y-o-y over the same period.

Apart from the K-Cups segment, the company’s traditional ground packaged coffee segment witnessed sales growth of 14% y-o-y during the month of August 2015, compared to the overall category’s 2.5% growth. This robust performance in the category was driven by 20% volume growth, compared to 14% growth in the prior 12 month period. Starbucks’ marketing strength, innovative products, and operational efficiency led to an extraordinary growth during this stiff competition. (Read: Starbucks Looks Forward To Winter Season, As Single-Serve Market Share Improves)

With the company outperforming the overall growth of this segment in the U.S., Starbucks has an upper hand in the industry going into the winter season. Trefis estimates the revenues generated by Consumer Products Group segment to rise 8% y-o-y in 2015.

Below is the chart showing the Trefis net revenue estimates for the company:

To summarize, the above three factors, along with a positive guidance, might just drive the company’s stock price. However, any slowness in the growth might instill negative sentiments among the investors.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes: