Philip Morris In Emerging Markets: Is A Slowdown Here To Stay?

Operational diversification has been the key to success for a number of business houses. In particular, many names such as Philip Morris International (NYSE:PM) have turned to a number of emerging markets in hopes of garnering growth. While the addictive nature of the products that the company sells, could prove to be an asset, emerging markets have been anything but lucrative recently. In a two-part series, we discuss whether the risks associated with functioning in emerging markets could actually outweigh the rewards for a company like Philip Morris. In this part, we discuss recent developments across major emerging economies. We further discuss contributing factors to these developments, along with how long it could last.

Annual GDP growth (in%) for developing nations, The World Bank

Overview of Major Emerging Markets

- Should You Pick Philip Morris Stock After 7% Fall This Year And Q4 Miss?

- Will Philip Morris Stock Rebound After A 10% Fall This Year?

- After 8% Drop This Year, Pricing Growth To Bolster Philip Morris’ Q3

- Pricing Gains To Drive Philip Morris’ Q2?

- Does Philip Morris Stock Have Upside Potential To Its Pre-Inflation Peak?

- Here’s What To Expect From Philip Morris’ Q1

Let’s start by discussing recent developments across key markets in Asia, Africa, and Latin America, that have made emerging markets less lucrative.

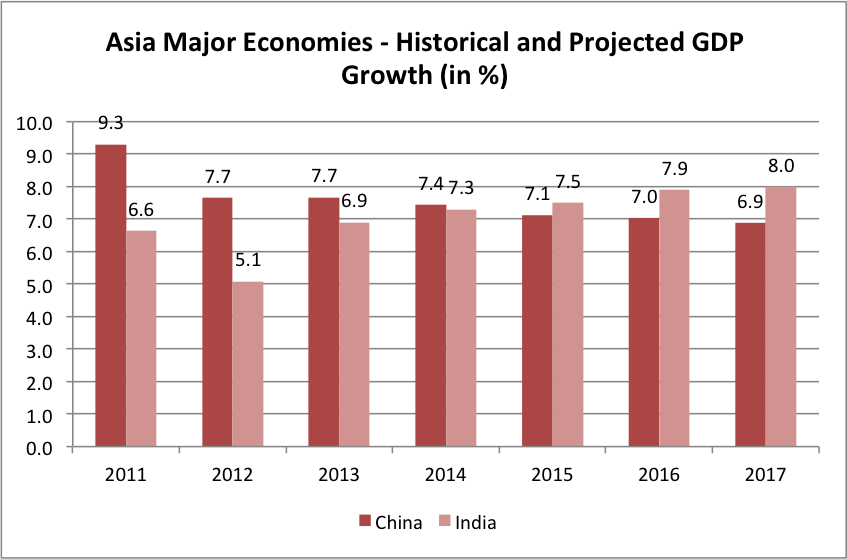

— Asia: It was not very long ago when most economists and business houses looked at Asia, particularly China, to be the engine of global growth. As the country’s economy underwent double-digit growth for decades, every one wanted a slice of the pie. However, things are no longer the same. China’s growth rate is expected to touch ~7% this year, the slowest rate in over 20 years, to make the region less lucrative than it was previously thought to be.

Source: The World Bank

— Latin America: Next, let’s move on to Latin America. Over the past decade, Latin America saw a drastic decline in poverty and rapid growth in its middle class population (~50% increase). This, along with improving infrastructure, made the region a bright spot for investments and business expansion. More recently, however, things are not quite the same for countries in the region. For one, growth rates have slowed. From growing at rates of about 4-5% until 2012, Latin American countries are clocking in rates of about 2% more recently, against the Chinese slowdown, declining investments, and dwindling commodity prices. Moreover, a number of important economies in the region, such as Brazil, Argentina, and Venezuela are facing major deceleration, that seem to have little scope of reversal in the near future. [1]

Source: The World Bank

— Africa: Finally, there is Africa, which was just as promising as Asia or Latin America, if not more. Back in 2013, an African Development Bank report suggested that Africa has been growing faster than any other continent, with a third of the countries posting growth rates of over 6%. [2] However, much like developing economies in Asia and Latin America, growth rates have slowed, even in African countries. The World Bank expects Africa’s growth rates to fall below 4% this year, which is lower than the 4.5%+ rates that the region has managed to sustain since the financial crisis. The major reasons cited for this development include slowing commodity prices, slow growth in China, electricity shortages, unstable currencies, high inflation rates, and mounting debt levels. Major economies such as Nigeria and South Africa have all seen growth slumps in Q2 2015, with Nigeria recording its slowest growth in a decade. [3]

Source: The World Bank

Top Contributing Factors

The recent developments in emerging markets can be broadly attributed to the Quantitative Easing (QE) taper in the U.S., low growth, and demand in China, and declining commodity prices. Let’s discuss each of these, in turn, to look for signs of reversal in the near future.

— QE taper in the U.S.: In the post recession period, the Federal Reserve resorted to a type of unconventional monetary policy called quantitative easing. In this, the Fed began electronically creating money, which was used to buy government bonds and mortgage-backed securities from commercial banks. Through this plan, the central bank achieved the twin goals of injecting liquidity, and lowering interest rates, in order to kick start growth. (To know more about QE, read Quantitative Easing In Focus) Recently, the Fed announced a QE taper. Against this, investors increasingly started moving funds back to the U.S. from emerging markets, in anticipation of higher interest rates. For some time now, the Fed has been indicating at implementing a rate hike this year. However, so far, there has been no change on this front, with interest rates remaining close to zero. According to a poll by the Wall Street Journal, 92% of economists believe that the rate hike should come in December. [4] While there is uncertainty even regarding this, the fact that the first hike is supposed to be followed by subsequent rounds of rate increases, could exacerbate the capital flight that emerging markets are seeing. Against this, we expect little reprieve on this front in the near future.

— China Slowdown : The slowdown in China can be attributed to a number of factors including waning demand for its exports, a slackening real estate sector, and lower global steel demand. With little notable progress in any of these areas, China’s low growth streak is expected to continue in 2015 and 2016, with the IMF projecting growth rates to reach 6.8% and 6.3%, respectively. [5] However, the crux of the problem lies in a lack of sustainability of the double-digit growth that China had been facing previously. While Chinese authorities have been pursuing a number of policies such as devaluing the yuan, lowering lending rates for commercial banks, pulling down reserve requirements, increasing infrastructure expenditure, and cutting taxes, to stimulate economic activity, a return to the double-digit growth rates seems to be highly unlikely, at least in the near term.

— Low Commodity Prices: Last, but not the least, are commodity prices. In recent times, the price of key commodities, such as oil, has more than halved, from costing over $100 per barrel, to a little less than $50. The drastic fall in price, can be attributed to a major spike in supply, while demand continued to wane against weakness in a number of economies. Now, according to a recent report by the International Energy Agency, oil prices are expected to remain low for another five years. This is expected to occur as the OPEC continues to hold on to supply, to avoid losing market shares, among other factors. [6] As oil prices continue to remain low, emerging markets that rely predominantly on oil exports to sustain their economies could continue to suffer even going forward.

Research by Capital Economics based on 19 emerging markets, shows that industrial output and consumer spending in Q2 hit the lowest level since the recession. In fact, the chief emerging markets economist at Capital Economics calls this the “new normal.” [7] Clearly, if these trends are really the “new normal,” it could entirely negate the benefits that companies such as Philip Morris expected to reap from diversifying operations into these markets. On the other hand, if emerging markets do recover in time, their vulnerability to crisis situations could mean more risk than rewards. In a follow-up article, we examine this situation more closely, to understand future prospects for Philip Morris from these markets.

We have a price estimate for Philip Morris’ stock price of around $81, which is slightly below the current market price.

See Our Complete Analysis For Philip Morris International

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap | More Trefis Research

Notes:- Latin America and Caribbean (LAC) Overview, World Bank [↩]

- Africa’s economy ‘seeing fastest growth’ [↩]

- African Economies See Substantial Slowdown [↩]

- Economists Overwhelmingly Expect Fed to Raise Interest Rates in December [↩]

- World Economic Outlook Update [↩]

- Oil price: traders ‘blindsided’ as oil inventories build towards 80-year high [↩]

- The emerging market slowdown: Don’t expect a quick recovery [↩]