Year-End Bounce Contrarian Investing Stock Opportunities

Submitted by George Putnam, III as part of our contributors program.

Year-End Bounce Contrarian Investing Stock Opportunities

Most of the time, I focus on fundamental business factors that affect the values of particular stock picks. But at this time of the year, we often see artificial selling pressures that may present buying opportunities almost regardless of stock fundamentals. These selling pressures come from two sources: Tax loss selling and portfolio window dressing.

- Rising 21% This Year, What Lies Ahead For Exxon Stock Following Q1 Earnings?

- Should You Pick General Electric Stock At $165?

- What’s Next For JetBlue Stock After A Sharp 19% Fall Post Q1 Results?

- Is Kimberly-Clark Stock Fairly Valued At $135 After A Solid Q1?

- How Will AMD’s AI Business Fare In Q1?

- Up 9% Year To Date, Will Chevron’s Gains Continue Following Q1 Results?

Tax loss selling happens when investors sell their losers to generate taxable losses to offset previously realized gains. After the strong stock market gains of the past two years, many investors probably have some significant gains to shelter this year.

Portfolio window dressing takes place when professional managers look over their funds as year-end approaches and notice that some of their holdings are showing big losses. They would rather not have those big losers show up in their published annual reports, and so they sell the embarrassing positions to get them out of the portfolio before it is memorialized at year-end.

When the new trading year begins in January, this artificial selling pressure disappears, causing many of these losing stocks to become winners, at least temporarily. Sometimes this year-end bounce will get a stock back into the limelight, and it will continue to go up for a prolonged period.

This strategy does not always work, but it often does. For example, in 2010-11, 2011-12 and 2012-13, the year-end bounce candidates that I identified in the December issue significantly outperformed the S&P 500 index over the first month or two of the year. 2014’s year-end bounce candidates were less successful, but the year-end effect may have been dampened because of the broad market weakness experienced in January 2014.

Nonetheless, I think it is worth mining for year-end bounce candidates again this year. The stocks profiled below represent the worst performers in the S&P 500 during calendar 2014, adjusted somewhat so that there is good diversification by industry group. My most recent contrarian investing newsletter discusses an additional five year-end bounce stock opportunities.

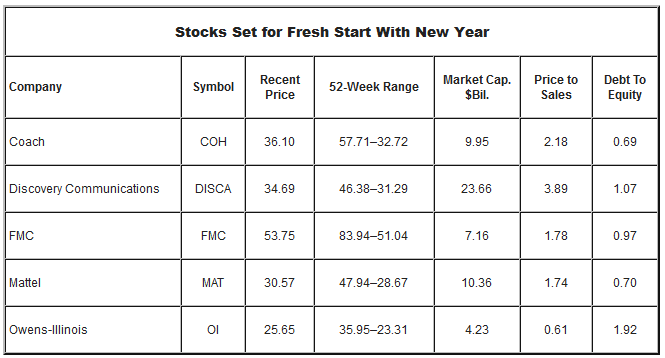

Coach (COH) is in the midst of a turnaround necessitated by its handbags and accessories falling somewhat out of fashion. Management responded by expanding the product line to include shoes and clothing. The operational rebound may still be several quarters away, but the brand is strong, and the stock looks like a good candidate for a year-end bounce.

Discovery Communications’ (DISCA) shares sold off earlier this year when a merger agreement with Scripps Networks fell through, and then fell further on disappointing ratings for the company’s cable networks. However, international revenues jumped 14% in the latest quarter. John Malone, a savvy media investor, controls the company, and so one can expect continued share repurchases and cannot rule out Discovery becoming part of the industry’s consolidation trend.

FMC (FMC), a diversified chemical company targeting agriculture (55% of 2013 sales), health and nutrition (20%) and minerals (25%), started 2014 on a high note. In March, the stock rallied on the news that the company would spin off its minerals segment. More recently, however, management changed course, made an acquisition and cut back on the planned divestitures. The action surprised investors, and the stock has been in a steady decline over the last nine months. The company is still in the process of transforming itself, and year-end selling could provide a good entry point into the stock.

Mattel (MAT), a well-known maker of toys, is facing the changing tastes of a generation brought up on electronic entertainment. While challenged, operations remain profitable and continue to throw off solid cash flow, and the brand still carries clout. The attractive dividend appears sustainable.

Owens-Illinois (OI) manufactures glass containers used in a wide range of food, beverage and pharmaceutical products. Sales and profit slides in North America and Asia Pacific should be offset by gains in Europe and Latin America. Management is focused on reducing costs and streamlining production, as well as increasing exposure to emerging markets.