Upcoming BioPharma Catalyst Trades to Consider

Submitted by Scott Matusow as part of our contributors program.

Trading Biophama stocks before a catalyst event – if done correctly – can be a very profitable proposition, but if traded in a wrong manner can cause losses. I remarked in an article from March of this year that Horizon Pharma (HZNP) was a good mid-term catalyst trade heading into its PDUFA 7/26/12 of LODOTRA, a proprietary modified delayed-release formulation of prednisone for the treatment of rheumatoid arthritis.

- A 3x Expected Rise In Mounjaro Sales Is Likely To Drive Eli Lilly’s Q1

- What Should You Do With Danaher Stock At $250 After Q1 Beat?

- Will A Macau Recovery Drive MGM Stock Higher Following Q1 Results?

- Lockheed Martin Stock Will Likely Remain In Focus After A Stellar Q1

- Up 17% YTD, What To Expect From eBay Q1 Results?

- Rising 21% This Year, What Lies Ahead For Exxon Stock Following Q1 Earnings?

In the article from March I remarked:

I recommend Horizon as a strong buy for the short and midterm swing trade. As the company nears its PDUFA date for LODOTRA, the price should be nearing $7 a share as I do not see insiders selling before this point. It appears to me they believe the drug will gain approval based on their heavy insider buying.

- Short term price target: $4.25

- Midterm price target: $7.00

At the time of my write-up the stock was trading at $3.69 a share. My goal of $7 was reached long in advance of the actual decision, in which LODOTRA gained FDA approval. However, after trading as high as $8.72 on July 3rd, the stock sold off on investor fear that the company might not have enough money to properly market the drug, raising concerns of a possible secondary offering – shareholder dilution.

The above demonstrates the clear risk/reward potential of these types of trades. There are times I feel that holding through a catalyst event is warranted. The first company I mention here is one that both traders and investors should give serious consideration as a longer term hold.

Ligand Pharmaceuticals (LGND)

Ligand Pharmaceuticals engages in the acquisition and development of royalty revenue generating assets in the United States. The company’s assets include PROMACTA, an oral thrombopoietin receptor agonist therapy for the treatment of adult patients with chronic immune thrombocytopenic purpura; AVINZA, a pain therapeutic; Viviant/Conbriza for the treatment of postmenopausal osteoporosis; and Nexterone, an injectable formulation. Its late-stage development program is comprised of PROMACTA, which has completed Phase III studies for thrombocytopenia in patients with hepatitis C; and is in Phase II clinical studies for the treatment of oncology-related thrombocytopenia in patients with solid tumors, sarcoma, and advanced Myelodysplastic Syndrome.

An FDA decision is expected on November 30th for its supplemental new drug application (SNDA) to the FDA for Promacta (eltrombopag) as a treatment for thrombocytopenia in adults with chronic hepatitis C infection to enable the initiation of interferon-based therapy, and to optimize interferon-based therapy.

In July 2012, Ligand’s partner GlaxoSmithKline (GSK) was granted priority review from the US Food and Drug Administration for the sNDA for Promacta to treat thrombocytopenia in adult patients with chronic hepatitis C virus (HCV) infection. Priority Review designation is given to drugs that if approved, offer major advances in treatment, or provide a treatment where no adequate therapy exists. Under the Prescription Drugs User Fee Act (PDUFA), the goal for completing a Priority Review is six months.

Thrombocytopenia is a relative decrease of platelets in blood. A normal human platelet count ranges from 150,000 to 450,000 platelets per microlitre of blood. These limits are determined by the 2.5th lower and upper percentile, so values outside this range do not necessarily indicate disease. One common definition of thrombocytopenia is a platelet count below 50,000 per microlitre.

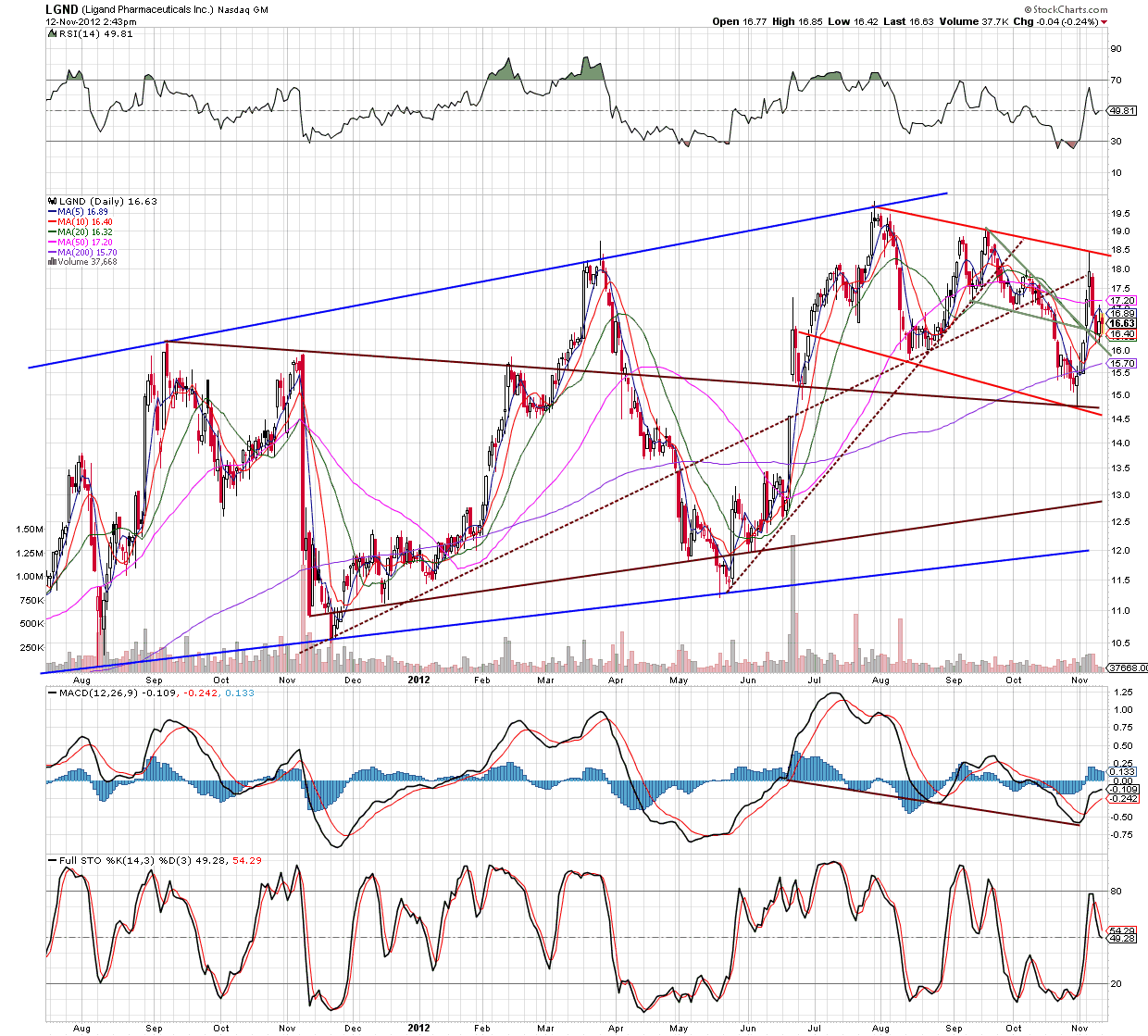

HCV is a huge market and is forecast to grow upwards of $8.5B by 2016, so I believe this event alone is a very good catalyst trade set up here for Ligand. Ligand also plans to start Phase 3 trials in multiple myeloma by the end of this year after reporting top-line results from their Phase 2 trial during Q4 2011. Ligand might also be a good longer term investment as two well-known analyst firms slapped a $25 price target on the company.

Onyx Pharma (ONXX), a partner of Ligand, reported $18.6M in Kyprolis sales for Q3 2012 — spurring Roth Capital to note that Ligand receives a 3% average royalty on Kyprolis sales. The firm believes that Kyprolis will help enable Ligand to rapidly become profitable and it maintains a $25 target and buy rating on the stock.

Cantor Fitzgerald also recently reiterated its rating of buy for Ligand, raising its price target from $22 to $25 — the same price target as Roth.

Also of note, the stock has a $35 price target from the point and figure chart.

(click to enlarge)

I like where the RSI and MACD signals are trending above and feel that with a market cap of $329.63M, the company makes for both an excellent catalyst event trade and long term buy and hold. My catalyst trade price target opinion is $19 – $20 with one year target of $27.

Catalyst trade strength opinion: 9/10

Impax Laboratories (IPXL)

Impax Laboratories engages in the development, manufacture, and marketing of bioequivalent pharmaceutical products. The company operates in two divisions, Global Pharmaceuticals and Impax Pharmaceuticals. The Global Pharmaceuticals division develops, manufactures, sells, and distributes generic pharmaceutical products. It provides its generic pharmaceutical prescription products directly to wholesalers and retail drug chains; and generic pharmaceutical over-the-counter and prescription products through unrelated third-party pharmaceutical entities.

On 2/23/12, IPXL announced the FDA acceptance of the IPX066 NDA to the FDA for the treatment of idiopathic Parkinson’s disease (PD).

The FDA notified Impax that its September 28, 2012 submission of requested information on an excipient in the Rytary formulation to the FDA has been designated as a major amendment. Since the receipt date of this additional information is within three months of the PDUFA date, the FDA has exercised its option to extend the PDUFA date to review the information. No new clinical trials or studies have been requested by the FDA. The original PDUFA date set for 10/21/12 has now been extended 3 months to 1/21/13.

Rytary is an investigational extended release capsule formulation of carbidopa-levodopa for the treatment of idiopathic Parkinson’s disease — it’s not approved or licensed anywhere in the world.

Idiopathic Parkinson’s disease is a degenerative disorder of the central nervous system. The motor symptoms of Parkinson’s disease result from the death of dopamine-generating cells in the substantia nigra, a region of the midbrain; the cause of this cell death is unknown. Early in the course of the disease, the most obvious symptoms are movement-related; these include shaking, rigidity, slowness of movement and difficulty with walking and gait. Later, cognitive and behavioral problems may arise, with dementia commonly occurring in the advanced stages of the disease. Other symptoms include sensory, sleep and emotional problems. PD is more common in the elderly, with most cases occurring after the age of 50.

The global market for Parkinson’s disease drug therapies is nearly $3 billion a year and growing — including $720 million in the United States.

Rytary is licensed to GlaxoSmithKline for countries outside the U.S. and Taiwan for development and marketing.

On October 30th, Impax shares fell as much as 18% following the release of disappointing third-quarter earnings results. With its current price of $20.25, I strongly feel it’s a very good entry point to go long up to the new PDFUA date of 1/21/13.

(click to enlarge)

The above chart demonstrates a possible pinch play. A pinch play is a good way to take advantage of dips and oversold stocks. The pinch play was founded on the convergence/divergence of the PPO and ADX indicators which can be found on all chart time intervals and markets. The chart above reflects a “knee jerk” sell-off reaction the stock saw after its earnings disappointment. Considering all the factors here, I rate Impax a very solid long catalyst trade.

Catalyst trade strength opinion: 8/10.

Amarin Corporation (AMRN)

Amarin focuses on developing the treatment for cardiovascular disease in the field of lipid science. Its lead product is Vascepa, a prescription-only omega-3 fatty acid comprised of icosapent ethyl or ethyl-EPA for the treatment of patients with very high triglyceride levels and high triglyceride levels or hypertriglyceridemia.

Vascepa hopes to compete with GlaxoSmithKline’s 1 billion dollar drug Lovaza. Both Vascepa and Lovaza are essentially pharmaceuticalized fish oil drugs that went through the full phase 1 to phase 3 process, and are now approved by the U.S. Food and Drug Administration for treating very high triglyceride levels.

Amarin has been expecting a FDA orange book decision on its New Chemical Entity (NCE) status soon for its recently FDA approved Vescepa — however, NCE approval or denial status continually has been delayed.

A new chemical entity or new molecular entity (NME) according to the U.S. Food and Drug Administration is a drug that contains no active moiety that has been approved by the FDA in any other application submitted under section 505(b) of the Federal Food, Drug, and Cosmetic Act.

An active moiety is a molecule or ion excluding those appended portions of the molecule that cause the drug to be an ester, salt (including a salt with hydrogen or coordination bonds), or other noncovalent derivative (such as a complex, chelate, or clathrate) of the molecule which is responsible for the physiological or pharmacological action of the drug substance.

A NCE is a molecule developed by the innovator company in the early drug discovery stage, which after undergoing clinical trials could translate into a drug that could be a cure for some disease. Synthesis of an NCE is the first step in the process of development of a drug. Once the synthesis of the NCE has been completed, companies have two options before them. They can either go for clinical trials on their own or license the NCE to another company.

In the latter option, companies can avoid the expensive and lengthy process of clinical trials, as the licensee company would be conducting further clinical trials and subsequently launching the drug. Companies adopting this model of business would be able to generate high margins as they get a huge one-time payment for the NCE apart from entering into a revenue sharing agreement with the licensee company.

The most important aspect of an NCE status grant is that it gives a drug a five year exclusivity period — giving the granted NCE status drug strong insulation from generic competition and challenges. This translates into more possible revenue — a higher stock price.

The FDA updates its orange book this Friday, so a decision for Vescepa is possible then. Based on this factor, I consider Amarin a decent catalyst trade this week.

Catalyst trade strength opinion: 7/10.

Additional disclosure: Disclaimer: This article is intended for informational and entertainment use only, and should not be construed as professional investment advice. They are my opinions only. Trading stocks is risky — always be sure to know and understand your risk tolerance. You can incur substantial financial losses in any trade or investment. Always do your own due diligence before buying and selling any stock, and/or consult with a licensed financial adviser.