Coca-Cola Earnings Review: Another Quarter Where Growth Gets Wiped Out By Currency Translations

There are a lot of things in transition for the world’s largest maker of non-alcoholic beverages, The Coca-Cola Company (NYSE:KO). The company is looking to restructure, consolidate some of its operations, and spin-off some others — all in a bid to drive operational efficiencies, reduce supply-chain costs, and improve profitability. And then, there are the Monster and Keurig deals, the premium milk brand Fairlife, all of which could add incremental sales going forward. But amid the altering dynamics, Coca-Cola continued to witness strong organic growth in Q3, reflecting a strong core business. Unit case volumes grew 3% year-over-year on a 2% and a larger 6%, growth in sparkling and non-sparkling volumes, respectively. [1] Price/mix was a major win, as expected, contributing 3 percentage points to the top line.

We estimate a $42 stock price for Coca-Cola, which is below the current market price.

See our full analysis for Coca-Cola

- Should You Pick Coca-Cola Stock At $60 After Q4 Beat?

- Down 10% This Year Is Coca-Cola Stock A Better Pick Over AbbVie?

- What’s Next For Coca-Cola Stock After 4% Gains In A Week Amid Q3 Beat?

- Down 15% This Year Will Coca-Cola Stock Rebound After Its Q3?

- Which Is A Better Beverage Pick – Coca-Cola Stock Or Monster Beverage

- Pricing Actions To Bolster Coca-Cola’s Q2?

However, as was also expected, the solid organic growth was let down by currency headwinds. In the tug of war between improved productivity and strong volume growth, and unfavorable currency translations, the latter seems to be winning, dragging down Coca-Cola’s overall results. This quarter too, while organic sales rose 3%, negative currency conversions were an 8% headwind. Considering that Coca-Cola generates more than 55% of its net sales from markets outside the U.S., macroeconomic volatility in overseas markets continues to be a downer for the American multinational. The U.S. dollar has continued to strengthen against foreign currencies, and could continue to get even stronger when the Fed decides to raise interest rates. After considering its current hedge positions, current spot rates, and the cycling of its prior year rates, Coca-Cola expects an approximate 7-point currency headwind on net revenue, and an 11-point headwind on operating income — thus wiping out all the organic growth.

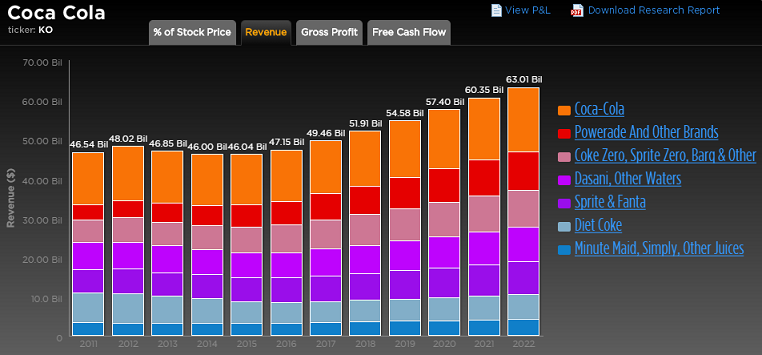

Currency has played spoilsport for mostly every large America-based multinational company this year, so it comes as no surprise that Coke’s revenues were down again this quarter, and down 2% year-over-year through the first nine months of the year. We’ll focus our analysis on the core performance of the beverage maker, particularly in terms of strategic pricing and marketing wins, and profitable growth.

Price/Mix Contributes Significantly To Organic Growth

The focus on smaller bottles and packs, which have higher price per unit volume, has boded well for Coca-Cola in recent times, and so has the sustained low gas prices and a general upbeat economic environment, which have boosted customer spending and allowed beverage companies to operate at higher price points. The U.S. GDP expanded at a solid 3.9% last quarter, which reflects stronger economic conditions. Coca-Cola’s incremental marketing is helping to accelerate revenue growth in some of its key markets, even North America, where the carbonated soft drinks (CSD) continues to face resistance. With a significant chunk of Coke’s revenues coming from the U.S., the home market becomes the most crucial operating unit for the company. Even more so now when the dollar is holding strong against foreign currencies; domestic growth is pivotal for Coca-Cola.

The good news is that the company is still managing growth through various marketing strategies and product campaigns that have resonated with the consumers, which is crucial considering that soft drinks are mostly an impulse buy, and what gives a company an edge is more reach, availability, and its social connect with the customer. Coca-Cola is also aiming to further increase its already large reach through long-time investments such as that in Monster Beverages and Keurig Green Mountain. Coca-Cola released some of its products with the Keurig Kold at-home carbonation machine just recently. In addition, the company signed a distribution agreement in the U.S. with Suja, a high growth organic cold-pressed juice company, and has announced plans to expand into plant-based protein drinks through the acquisition of the beverage business of China Green Culiangwang Beverages Holdings in China. So basically, Coca-Cola, being the beverage behemoth it is, is still looking to expand and find ways to grow consumption.

Coke Is Restructuring Its Way To More Profitability

Currency headwinds are expected to continue to drag down the top line in the near term, but Coca-Cola remains committed to increase spending behind its beverage portfolio, aiming for future growth. The company’s investment plans are supported by its plans to save an incremental $1 billion in productivity gains by 2016, and raise that to $2 billion by 2017, and $3 billion by 2019, through system standardization, supply-chain optimization, and industrious resource and cost allocation.

Coca-Cola is looking to refranchise two-thirds of its bottling territories in North America by the end of 2017, and a substantial portion of the remaining territories no later than 2020, in a bid to move away from the capital intensive and low-margin business of distribution. All this in hopes to improve operating performance. So far, the company has transferred or signed agreements for territories covering over 30% of U.S. bottle can volume, and announced the creation of the National Product Supply System, to strengthen and streamline U.S. production.

In addition, Coca-Cola announced during Q3 the combination of Coca-Cola Enterprises, Coca-Cola Iberian Partners, and the company’s subsidiary Coca-Cola Erfrischungsgetränke AG into one bottling company called Coca-Cola European Partners. What the consolidated bottling operations will do is trim the extra overhead costs, improve supply-chain efficiency, and leverage the best practices of each of the bottlers to improve service to customers and consumers across Western Europe — the company hopes.

Coca-Cola’s operating margins have dropped to 21% through the first nine months, from 23.5% a year ago, but this result has also been mostly impacted by unfavorable currency translations. Investments in marketing and advertising in a bid to boost consumption and productivity savings could help bolster profitability growth in the coming future.

See the links below for more information and analysis:

- Coca-Cola pre-earnings: expect the stronger dollar to wipe out strong organic growth yet again

- Bottled water is a potential growth category that can’t be ignored

- Soda makers wonder: where could growth in U.S. come from?

- Coca-Cola beats consensus estimates; delivers strong growth in Q1

- Negative currency translations overshadow PepsiCo’s strong organic growth in Q1

- Trefis analysis: Coca-Cola Coke U.S. Revenues

- Trefis analysis: Coca-Cola Diet Coke International Revenues

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research