Will The U.S. Treasury Department Rules, That Killed The Pfizer-Allergan Deal, Affect Johnson Controls-Tyco Merger?

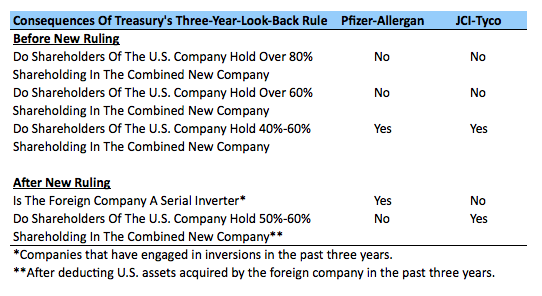

Inversion deals, wherein the tax domicile of the new company is shifted to that of the foreign company, have received a lot of flak recently in the U.S. Such deals are done mostly to take advantage of the lower tax rates in the foreign country, as the corporate tax rate in the U.S., of 35%, is among the highest in the world. Keeping this in mind, the U.S. Treasury Department issued new rules recently against corporate inversions. One of the new rules goes after “serial inverters” — companies that have indulged in multiple inversions in the past. As per the new rule, three years of past mergers with U.S. corporations are disregarded in order to determine the size of the foreign company. Therefore, by subtracting the value of U.S. assets that a foreign company has acquired, the foreign company would become smaller in relation to the U.S. company. The size of the company is taken into account to calculate the shareholding of the U.S. company in the combined firm. A foreign corporation is required to own at least 40% of the combined company in order to reap any significant tax benefits from an inversion. If, after the merger, the shareholders of the former U.S. company own at least 80% of the combined firm, the government treats the new combined firm as subject to U.S. taxes, eliminating the positives of the inversion. If they own at least 60%, some restrictions apply, but the company is still regarded as foreign. This has prompted companies to keep the level below 60%, leading the U.S. government to propose rulings halting such deals. As a result of this new rule, the Pfizer-Allergan deal could not move forward, as Allergan itself was a result of a number of inversions. However, Tyco has not made any significant acquisitions of U.S. based assets in the last three years, and therefore, the combined JCI-Tyco will not violate the new Treasury “three-year-look-back-rule.” This merger is also not just about tax savings; the combination of highly complementary businesses facilitates the new company to offer comprehensive and innovative solutions to a wider market globally, across numerous end markets.

Have more questions on Johnson Controls? See the links below:

- Johnson Controls’ Earnings Beats Expectations

- Will Johnson Controls Miss Estimates Again?

- How Has Johnson Controls’ Net Sales Changed By Geographic Areas?

- How Does The Adient Spin-Off And Tyco Merger Create Value For Johnson Controls’ and Tyco’s Shareholders?

- What Costs Did Johnson Controls’ 2015 Restructuring Plan Entail?

- Johnson Controls: Year 2015 In Review

- How Will Johnson Controls’ Revenue And EBITDA Composition Change In The Next 3 Years?

- How Has Johnson Controls’ Revenue And EBITDA Composition Changed In The Last 5 Years?

- What’s Johnson Controls’ Fundamental Value Based On Expected 2016 Results?

- By What Percentage Did Johnson Controls’ Revenue & EBITDA Grow In The Last 5 Years?

- What’s Johnson Controls’ Revenue And EBITDA Breakdown?

Notes:

- Q4’23 Earnings Preview: Down 21% YTD Will Johnson Controls Stock Continue To Underperform?

- What’s Next For Johnson Controls Stock After An 8% Fall Yesterday?

- Margin Expansion To Drive Johnson Controls’ Q3?

- What’s Next For Johnson Controls Stock After An Upbeat Q2?

- Here’s What To Expect From Johnson Controls’ Q2

- Here’s What To Expect From Johnson Controls’ Q1

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research