How Does The Adient Spin-Off And Tyco Merger Create Value For Johnson Controls’ and Tyco’s Shareholders?

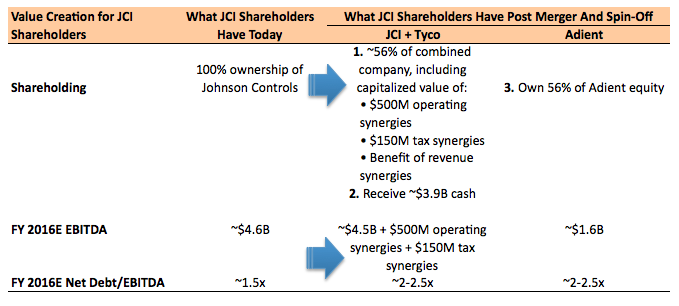

Under the terms of the JCI-Tyco merger agreement, Johnson Controls’ shareholders will hold a 56% equity stake in the combined company, and will receive a cash consideration of ~$3.9 billion, with Tyco owning approximately 44% of the equity. The combination of highly complementary businesses facilitates the new company to offer comprehensive and innovative solutions to a wider market globally, across numerous end markets. The main purpose of the merger seems to be gaining size in its area of focus, which is becoming a colossus in the building controls and equipment market. The new company will be able to witness immediate opportunities for growth, through cross-selling of products, complementary distribution networks, and a widened global reach. The geographic fit seems to be ideal, with JCI strong in the Chinese market, and Tyco effective in Europe.

The combined company is expected to furnish minimum operational synergies of $500 million over the first three years, after closing. According to Johnson Controls, this will be achieved by increasing efficiencies, removing redundancies, integrating global branch networks, and leveraging the combined scale of the $20 billion building’s business platform. Besides the above savings, tax synergies of over $150 million are expected as a result of the inversion deal, wherein the tax domicile of the new company will be shifted to Ireland, home of Tyco. In Ireland, the corporate tax rate is 12.5%, as opposed to the 35% in the U.S. In such a scenario, while the new company still has to pay U.S. taxes on U.S. income, it can avoid paying U.S. taxes on overseas income.

Notes:

View Interactive Institutional Research (Powered by Trefis):

- Q4’23 Earnings Preview: Down 21% YTD Will Johnson Controls Stock Continue To Underperform?

- What’s Next For Johnson Controls Stock After An 8% Fall Yesterday?

- Margin Expansion To Drive Johnson Controls’ Q3?

- What’s Next For Johnson Controls Stock After An Upbeat Q2?

- Here’s What To Expect From Johnson Controls’ Q2

- Here’s What To Expect From Johnson Controls’ Q1

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research