Factors That Will Drive JetBlue’s Valuation

Once a loss-making industry, the US airline sector has been flourishing over the last 15-18 months due to the plummeting crude oil prices. No doubt, the ongoing oil slump has proved to be a boon for the majority of the airlines across the globe, particularly in the US. However, JetBlue Airways (NASDAQ:JBLU) is one of the few US airlines that has not only outperformed its counterparts and industry benchmarks by a huge margin, but also has a significant upside to its current valuation. In this note, we aim to briefly touch upon the key factors that we believe will provide a boost to the low cost carrier’s stock in the short term.

Factors Driving JetBlue’s Valuation

Source: Bank of America Merrill Lynch 2015 Transportation Conference, May 2015

Premium Product Offering – “Mint Service”

- Gaining Over 20% This Year, What Lies Ahead For JetBlue Stock Following Q1 Results?

- Should You Pick JetBlue Stock At $6 After Q4 Beat?

- What’s Next For JetBlue Stock After A 35% Fall This Year?

- Here’s What To Expect From JetBlue’s Q2

- Will JetBlue Stock Recover To Its Pre-Inflation Shock Highs?

- What Led To A 62% Fall In JetBlue Stock Since 2019?

In order to tap the elite and corporate passengers, JetBlue had launched a premium service called “Mint” in June of 2014. This was mostly focused at business travelers flying on transcontinental routes in the US, such as San Francisco and Los Angeles. Given the affordability and higher quality of services offered, this new product gained a tremendous response from travelers and became a preferred choice of the passengers. In fact, the airline witnessed a 20% jump in the revenues on its Mint routes within six months of its launch. Since the Mint service is a high margin product, it resulted in a notable improvement in the airline’s performance over the last one year. The airline’s operating margin grew from 8% in the first three quarter of 2014 to 18% in the same period this year.

Source: Bank of America Merrill Lynch 2015 Transportation Conference, May 2015

To further capitalize on the new product, JetBlue plans to offer flights with Mint service on the Boston-San Francisco and Boston-Los Angeles routes starting early 2016. We expect to see the airline launching this premium service on other routes as well to enhance their operating margins in the future.

Low Cost Structure

While most of the US airlines are basking in the recent plunge in oil prices, JetBlue has remained grounded and is preparing well for the eventual rebound in oil prices. Thus, despite the huge fuel cost savings, the low cost carrier is consistently working towards controlling its unit costs (excluding fuel expenses). For this, the airline has been investing heavily on fuel-efficient aircraft and negotiating better terms in its labor contracts. Also, the New York-based airline aims to restrict its unit costs (excluding fuel costs) from growing at more than 2% annually over the next couple of years.

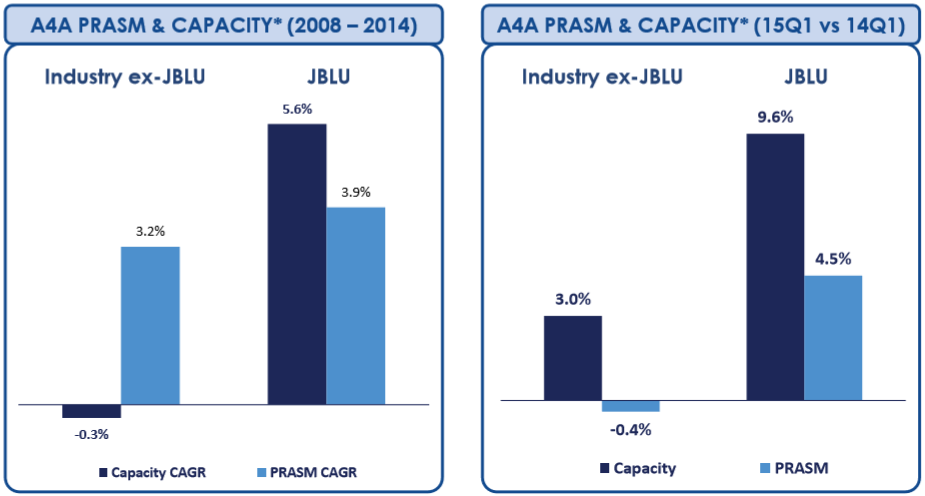

Moreover, JetBlue has an obvious low cost advantage over its peers due to its domestic operations, which has enabled the airline to remain immune to the foreign currency fluctuations and lower surcharges from the international markets. While the network carriers, such as American Airlines, Delta Air Lines, and United Continental, experienced a drastic fall in their unit revenue during the first nine months of 2015, JetBlue saw a constant rise in its unit revenue, despite the rapid capacity growth undertaken by the airline. Thus, given this low cost advantage, along with its cost reduction initiatives, we forecast that JetBlue will continue to deliver higher margins in the near future and compete head on with the legacy carriers.

Source: Bank of America Merrill Lynch 2015 Transportation Conference, May 2015

Expanding Into High Value Geographies

JetBlue’s management has always been cautious about the markets that it enters or operates in. The low cost carrier is based out of New York, which enables it to cater to a large number of passengers from the heart of the cultural and economic capital. The airline has a strong holding on the Los Angeles and San Francisco routes, which are considered to be the busiest and most coveted routes in that region. Having access to such high value markets allows JetBlue to steadily grow its passenger traffic, contributing to its top line growth.

However, the airline is not satisfied with its current market share. So, as a growing airline, it now plans to expand its operations in the Latin America and the Caribbean markets, one of the most lucrative and high value markets for airlines after Asia. Despite offering around 142 daily flights from the US to Latin America and the Caribbean, the airline launched flights to the Mexico City in October 2015 and to Antigua and Barbuda in November 2015. It plans to offer flights to Quito in February 2016.

Further, with the relaxation of travel restrictions between the US and Cuba, JetBlue launched its first weekly flight between New York and Havana this year. The airline has also announced a second weekly nonstop charter flight on the same route to deepen its presence in the formerly restricted destination. By offering charter flights at competitive fares and with high quality services to Cuba, early in the day, JetBlue is likely to tap an underexplored market which could further strengthen its position in the Latin American market. Thus, we foresee the Latin America and the Caribbean becoming a sizeable part of the airline’s revenue, and driving its long-term valuation.

Entering High Value Markets

Source: Bank of America Merrill Lynch 2015 Transportation Conference, May 2015

In a nutshell, we figure that JetBlue’s domestic presence and low cost structure have enabled it to outperform its larger competitors over the last year. Over the long term, we anticipate that the airline’s premium Mint service, and focus on high value markets, will drive its growth. Our price estimate for JetBlue stands at $28 per share, around 5% higher than its current market price.

See Our Complete Analysis For JetBlue here

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap