Cost Reduction Efforts May Not Improve Halliburton’s 3Q Earnings, Yet The Company Is Positive On Its Future Prospects

Despite the challenging oil price environment and the hurdles faced in completing its merger with Baker Hughes (NYSE:BHI), Halliburton (NYSE:HAL) continues to fight back strongly. The oilfield services company is fully committed towards the merger, which is likely to generate over $2 billion in cost synergies, and consequently, has directed most of its time and efforts in obtaining the regulatory approvals for completing the merger, particularly in the last three months. Yet, the company has not lost sight of the difficult times ahead and has been working towards reducing its costs and improving its operating efficiency to weather the current commodity down cycle. Although these efforts may not be able to prevent the meaningful decline that the company is likely to witness in its third quarter earnings, we expect to see a more resilient performance from the company in the next couple of quarters even with a bleak outlook for crude oil prices. Here’s our take on the company’s third quarter performance ahead of its earnings release, which is expected to be released on 19th October 2015. [1]

See Our Complete Analysis For Halliburton here

Weak North American Drilling Activity Will Weigh On Halliburton’s Revenues

- Up 7% This Year, Will Halliburton’s Gains Continue Following Q1 Results?

- What To Expect From Halliburton’s Q3 After Stock Up 10% This Year?

- What To Expect From Halliburton’s Stock?

- Can Halliburton Stock Return To Its Pre-Inflation Shock Highs?

- Halliburton Stock Likely To See Higher Levels Post Q1 Results

- What to Watch For In Halliburton’s Stock Post Q4?

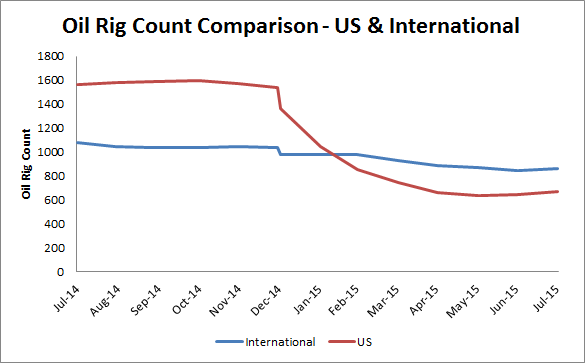

After having recovered to over $60 per barrel in the second quarter, the crude oil prices saw yet another sharp fall in the third quarter, attributable to the fear of a slower-than-expected growth in the Chinese economy, which could severely impact the demand for crude oil, further adding to the supply glut. Thus, in the wake of falling crude oil prices, the large Exploration and Production (E&P) companies in the US continue to hold back their upstream capital spending even in the current quarter. This is evident from the plummeting rig count globally, more significantly so in the North American region. The US oil rig count, one of the closely watched metrics in the industry, stood at 640 units at the end of the September quarter [2], representing a decline of almost 60% since the beginning of the year. With more than half of Halliburton’s revenues coming from the North American drilling markets, we expect the oilfield giant’s revenues to experience a notable decline during the current quarter.

Contrary to this, the international drilling markets have been somewhat insusceptible to the falling crude oil prices due to the lower break-even costs of their conventional oil plays. Also, the international upstream participants have larger reserves and are better leveraged. Thus, the international oil rig count has dropped by only 16% since the beginning of the year, which is roughly one-third of the decline in the US oil rig count [3]. While this might soften the blow of the falling North American drilling demand, it may not be able to completely offset the significant decline in Halliburton’s top line.

Source: Baker Hughes Rig Count Data

Cost-Cutting Efforts May Not Pay Back Much In 3Q But Likely To Improve Margins Going Forward

The Houston-based oilfield service company recently cut down its workforce by 2,000, primarily in the North American region, as the region has been the worst hit by declining commodity prices (Read: Will Halliburton’s Proactive Efforts Work In Its Favor?). With these job cuts, the company has reduced almost 19% of its headcount since the beginning of the oil slump. However, unlike its competitor, Schlumberger (NYSE:SLB), Halliburton began these initiatives very late in the day, i.e. in the first quarter of this year. Thus, we do not expect these initiatives to show a significant impact on the company’s earnings in the September quarter. But, in spite of a weak outlook for the crude oil market, we anticipate these cost reduction measures, coupled with the cost synergies from the Baker Hughes merger (if it passes through), to allow the company to survive this downturn much more efficiently.

Overall Positive Outlook For the Future

While its counterparts are wailing over the depressing outlook for the oil market, Halliburton appears to be very optimistic about its future prospects. The No. 2 player in the oilfield services industry expects its exposure to the North American markets to become a sizeable upside, as and when the oil prices rebound. In a recent industry conference, the company pointed out that the North American unconventional plays are likely to yield higher returns due to lower costs and will require shorter time to be developed. Thus, the North American unconventional markets will be able to provide the fastest incremental barrel of oil to the market, once the current oversupplied oil market eases out. Since the company expects the market to revive as soon as the decline rates of the existing wells dry up the supply glut, it sees the North American exposure as an opportunity to outperform its peers (read: Schlumberger) who have limited exposure to the coveted market.

Source: Barclays CEO Energy-Power Conference, September 2015

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes: