Halliburton Delivers Strong 2Q Earnings Despite Sluggish US Drilling Demand

Oilfield services major, Halliburton (NYSE:HAL), followed the footsteps of its closest competitor, Schlumberger, and surprised the market by reporting stronger-than-expected second quarter results before the market opened on Monday, 20th July 2015. Despite the plunge in the US drilling activity, the company managed to post profits (excluding special items) of $380 million or 44 cents per share((Halliburton Announces Second Quarter Results, 20th July 2015, www.halliburton.com)), beating the market estimate by almost 15 cents per share. While the quarterly revenues were down both sequentially, as well as annually, due to the sharp decline in the US oil rig count, they exceeded the consensus estimate by more than a $100 million. Going forward, we expect the acquisition of Baker Hughes to strengthen Halliburton’s product offering and enable the company to face the current downturn more efficiently. In this article, we discuss the key highlights of Halliburton’s second quarter earnings release and its outlook going forward.

See Our Complete Analysis For Halliburton here

North American Revenues Decline On Weak Drilling Demand

- Up 7% This Year, Will Halliburton’s Gains Continue Following Q1 Results?

- What To Expect From Halliburton’s Q3 After Stock Up 10% This Year?

- What To Expect From Halliburton’s Stock?

- Can Halliburton Stock Return To Its Pre-Inflation Shock Highs?

- Halliburton Stock Likely To See Higher Levels Post Q1 Results

- What to Watch For In Halliburton’s Stock Post Q4?

Despite a 26% decline in the worldwide rig count during the quarter, Halliburton’s total revenue declined only 16% on a sequential basis to $5.9 billion, beating the market expectation of $5.8 billion((Halliburton Announces Second Quarter Results, 20th July 2015, www.halliburton.com)). However, the North American revenues continued to be a drag on the company’s revenue, falling 25% sequentially due to a 40% drop in the North American oil rig count during the June quarter. The Latin American market remained weak driven by the currency headwinds and spending restrictions in Venezuela. All the other international markets also suffered moderately due to the large pullback in upstream spending during the quarter.

Halliburton’s operating income from the North American region declined more than 50% to $130 million [1] on the back of lower drilling demand and high cost deflation. However, the effect of this sharp fall was partially offset by the operating income from the Europe/Africa/CIS region, which improved on a sequential basis due to the increased activity in Eurasia and Norway along with higher stimulation activity and completion sales in Algeria and Angola. This coupled with the cost reduction measures of the company, resulted in an adjusted income of $380 million, or 44 cents per share, down from $418 million, or 49 cents per share, in the last quarter, exceeding the analyst forecast of 29 cents per share for the June quarter.

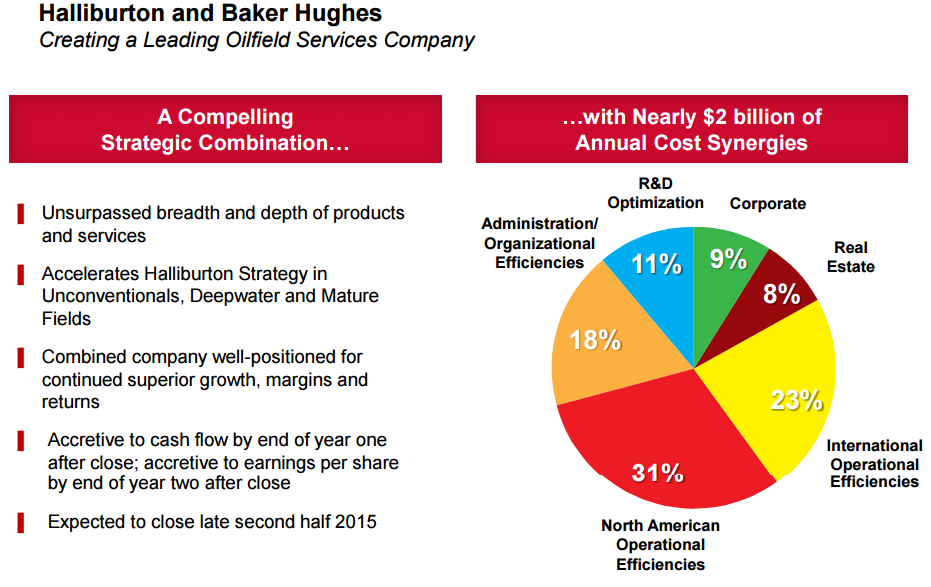

Merger To Be An Upside In The Future

Based on the latest update on the merger((Halliburton and Baker Hughes Provide Update On Proposed Acquisition)), Halliburton and Baker Hughes (NYSE: BHI) have entered into an agreement to extend the time for the Antitrust Division of the US Department of Justice (DOJ) to review the compliance certificates furnished by the two companies. The companies now expect their certificates to be reviewed latest by the 25th November 2015 and expect to close the deal by 1st December 2015.

For the June quarter, Halliburton recorded an acquisition cost (after tax) of $67 million as opposed to $35 million((Halliburton Announces Second Quarter Results, 20th July 2015, www.halliburton.com)) in the last quarter. The oilfield giant is currently marketing its Fixed Cutter and Roller Cone Drill Bits, Directional Drilling, and Logging-While-Drilling (LWD)/Measurement-While-Drilling (MWD) businesses for sale to comply with the antitrust requirements relating to the merger. In addition, the company is working closely with various competition enforcement authorities around the world to ensure that the deal receives all regulatory clearances within the stipulated time frame.

Source: Halliburton 1Q15 Investor Update Presentation

Outlook

Despite a bleak outlook for the industry, we expect Halliburton to stay strong and fare better than its peers with its vast product offering and cost control initiatives. Besides, we see that Halliburton is fully committed to close the transaction and achieve cost synergies of nearly $2 billion, which will enable the combined entity to easier navigate the challenging oil price environment and be well positioned when oil prices recover. However, these cost synergies will kick in only in the next year as the merger completion date has been pushed to the end of the year.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes:- Halliburton Announces Second Quarter Results, 20th July 2015, www.halliburton.com [↩]