Why Goldman’s Long-Term Quarterly Results Could Look A Lot Like Those For Q1

Goldman Sachs (NYSE:GS) reported notably poor results for the first quarter of the year on Tuesday, April 19, as the premier investment bank witnessed a sharp year-on-year reduction in revenues for each of its operating divisions. [1] Although the top line figure shrank more than what investors estimated for the period, Goldman managed to beat earnings estimates by slashing compensation expenses by a steep 40% year on year — allowing it to report an almost 30% reduction in total operating costs.

Now Goldman’s revenue problem is not specific to the bank, as the industry at large has reported significantly lower revenues due to volatile equity market conditions, an uncertain interest rate environment and weak geopolitical conditions in several key global economies. Interestingly, however, the weak Q1 results may actually represent the impaired revenue generating capability of Goldman’s current business model, given that future global regulatory changes are likely to severely crimp the bank’s revenues from fixed income trading as well as from its principal investments. After all, Goldman is the only major investment banks that is looking to grow its fixed income trading desk, even as peers have implemented sizable cuts in the segment. This is a bet that can weigh on both the company’s results as well as its capital structure in the near future, if debt trading activity does not pick up substantially worldwide. Also, Goldman still has considerable investments in hedge funds and private equity funds — something it has to slash over 2016-2017 to be compliant with the Volcker Rule.

- Trailing S&P500 By 18% Since The Start Of 2023, What To Expect From Goldman Sachs Stock?

- Down 12% In The Last Twelve Months, Where Is Goldman Sachs Stock Headed?

- What To Expect From Goldman Sachs Stock?

- Goldman Sachs Stock Is Undervalued At The Current Levels

- Goldman Sachs To Edge Past the Consensus In Q1

- Goldman Sachs Stock Is Trading Below Its Intrinsic Value

That said, trading conditions have been exceptionally poor over the last three quarters, and things are definitely expected to improve in coming quarters. While a reduction in its extremely profitable (and volatile) proprietary investments unit will drag down revenues and profits in the long run, Goldman is exploring additional avenues of growth, including products and services targeted towards retail banking customers. Moreover, the bank still commands the largest share in the global securities trading and M&A industries. This is why we stick to our $200 price estimate for Goldman’s stock, which is around 20% ahead of the current market price.

See the full Trefis analysis for Goldman Sachs

Is Goldman Overly Optimistic About The Fixed Income Industry?

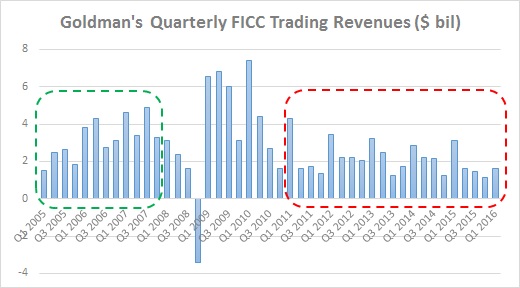

Goldman’s fixed-income, currency and commodities (FICC) trading desk generated $1.7 billion in revenues in Q1 2016 – roughly half the $3.2 billion figure roped in a year ago (after adjusting for accounting gains or losses from revaluation of its own debt). While these revenues were expected to be poor, given the weak levels of trading activity worldwide, the fact that results were exceptionally poor is made quite clear by the fact that this was Goldman’s worst first quarter FICC trading performance since 2005. After all, the seasonal securities trading business sees the most gains in the first quarter of a year.

But there appears to be a larger, more far-reaching factor at work behind Goldman’s sub-par FICC trading performance over recent quarters. It must be remembered here that full-year 2015 was the worst period for Goldman’s FICC trading desk since 2008, in terms of total revenues. The chart below captures Goldman’s FICC trading revenue for each quarter since early 2005, and it makes it easy to discern the marked difference in performance before and after the economic downturn.

To better understand the change in these revenues, it will help to divide the time period into two parts: the pre-recession phase (2005-2007) and post-recession phase (2011 onwards). Given the extreme volatility in capital markets over 2008-2010, we have ignored this period for our the analysis. On an average, Goldman’s FICC trading desk generated $3.2 billion in revenues each quarter over 2005-2007. In comparison, the figure since 2011 has been $2.1 billion – a 35% decline. While a chunk of this difference can be attributed to over-sized gains on mortgage-backed securities in the run-up to the downturn, there has been an undeniable impact of stricter regulatory requirements on the industry as a whole.

While nearly every other global investment bank has cut down on its FICC trading operations (especially Morgan Stanley and UBS which have shifted their focus on equity trading), Goldman continues to believe that the debt trading industry will soon witness a turnaround. And if conditions in the industry actually improve, Goldman is in a position to pocket much bigger gains than any of its rivals, due to its much larger presence. However, if global debt trading revenues remains depressed in the long run, this will represent a significant downside to Goldman’s value.

The Investment & Lending Division Is Coming Up On Its Volcker Rule Deadline Soon – And It Will Hurt Revenues

Goldman’s Investment & Lending division has been the subject of considerable discussion among investors and regulators in recent years because of the extent of its proprietary investments. The Volcker Rule prohibits banks from indulging in proprietary trading activities, and also limits the amount of its own cash that a bank can invest in private-equity funds or hedge funds to 3%. According to Goldman’s annual report for the year 2015, the bank had investments of $7.76 billion in funds that come under the purview of the Volcker Rule – nearly all of which it will have to exit by mid-2017. This poses two problems for the bank: firstly, the depressed market conditions have hurt the valuation of these investments – something that stands out from the fact that Goldman reported quarterly revenues of just $87 million for the division in Q1 2016 compared to $1.3 billion in the previous quarter and $1.7 billion a year ago. Unless market conditions improve quickly, Goldman will have to dispose of these investments at sub-par prices and incur losses in the process. Secondly, even if market conditions reverse soon, these funds are quite illiquid in nature, and will anyway see mark-downs as the bank tries to sell them off.

All things considered, Goldman has exploited several loopholes in the Volcker Rule to work-around some restrictions – something we have illustrated over the years in the bank’s use of business development companies and long-term hedging trades. Unless these loopholes are closed, Goldman’s investment & lending division should report sizable revenues in the long run – albeit at levels lower than what it has seen in the past. You can see how a reduction in these revenues impacts Goldman’s share value by making changes to the chart below.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research

- 2016 First Quarter Results, Goldman Sachs Press Releases, Apr 19 2016 [↩]