Dr Pepper Snapple Earnings Preview: The Perpetual Third Is Poised To Grow By More Than Its Compatriots

Dr Pepper Snapple (NYSE:DPS) is scheduled to announce its Q2 and mid-term earnings on July 23, and our focus will be on whether the perpetual third in the U.S. carbonated soft drinks (CSD) market is able to, yet again, outpace the growth seen by its much larger compatriots — The Coca-Cola Company (NYSE:KO) and PepsiCo (NYSE:PEP). [1] The U.S. forms almost 90% of Dr Pepper’s net sales, and CSDs alone are 80% of the volume sales for the maker of Snapple tea and Dr Pepper soda.

While currency has remained a pivotal talking point in the earnings previews of most large U.S.-based multinationals, Dr Pepper’s relatively lower exposure to foreign markets (In 2014, 4% and 8% of the net sales came from Canada and Mexico and the Caribbean, respectively), makes it less vulnerable to the impact of depreciating foreign currencies — one reason why the company’s solid organic growth has gone on to be reflected in the net growth, too. After all, what good is strong core organic growth, if it is reversed by negative currency translations?

See Our Complete Analysis For Dr Pepper Snapple

- Will United Airlines Stock Continue To See Higher Levels After A 20% Rise Post Upbeat Q1?

- Up 8% This Year, Why Is Costco Stock Outperforming?

- Down 7% In A Day, Where Is Travelers Stock Headed?

- What’s Next For Johnson & Johnson Stock After Beating Q1 Earnings?

- Should You Pick UnitedHealth Stock At $480 After A Q1 Beat?

- American Express Stock Is Up 17% YTD, What To Expect From Q1?

In this article, we will discuss how Dr Pepper could grow again this quarter, maybe even more than both Coca-Cola and PepsiCo, organically, and considering how the former is less exposed to currency risk, this growth could be more pronounced.

- Dr Pepper Could Achieve Growth In U.S. CSDs In Q2 Again

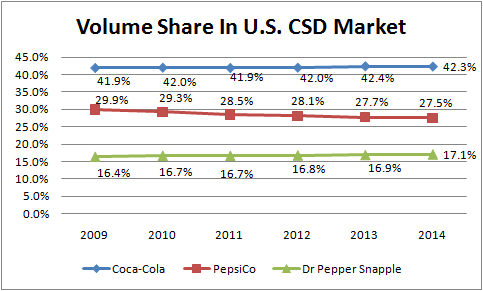

In Q1, CSD volumes grew 3% for Dr Pepper, and net volumes rose 2% in the U.S., outperforming both Coca-Cola and PepsiCo’s volume growth. And this trend could continue into the second quarter. Why? Because Dr Pepper has more scope to grow in the U.S. CSDs than its chief competitors, who are almost omnipresent in the country, and together already account for ~70% of the segment volumes. The sugary sodas market in the U.S. is relatively mature, and has declined for ten consecutive years now, reflecting how volume growth in this space might be hard to come by. But while it might be tough for the likes of Coca-Cola and PepsiCo to further grow their already large volume shares, Dr Pepper has that opportunity.

For example — the staple Dr Pepper drink grew volumes by 0.5% last year, outperforming both Coke and Pepsi-Cola, and consolidating its position as the fifth-highest-selling soft drink in the U.S. [2] Considering that most of these top companies are generally well-regarded by customers, volume sales become a function of reach and availability–where Dr Pepper lags both Coca-Cola and PepsiCo. As around 59% of volumes of the drink Dr Pepper are distributed by bottlers affiliated with Coca-Cola and PepsiCo, Dr Pepper doesn’t possess as much control over shipments to ensure optimum store placement, somewhat hampering its reach and availability.

Now with more focus on direct store delivery (for example, Dr Pepper acquired Davis Beverage Group and Davis Bottling Company, which almost doubled Dr Pepper’s distribution in Pennsylvania), which allows the beverage manufacturer to bypass third-party and retailers’ distribution centers, Dr Pepper could further improve its visibility, and, in fact, also boost margins. By bringing distribution in-house, the company could leverage its integrated model to capture downstream margin opportunities. Dr Pepper’s direct store delivery (DSD) system could provide shelf inventory management and reduce costs of re-ordering and merchandising for the retailer, aiming to improve sales and margins for the retailer, as well. This could protect the company’s shelf space in retail stores.

Not only on the back of volume growth, Dr Pepper’s top line growth is expected to be boosted by positive price and packaging mix in Q2. The consumer price index for non-alcoholic beverages has risen through Q2 in the domestic market, bolstered by stronger economic conditions, and higher retail per unit value could be the revenue driver in CSDs this quarter. And remember, as the revenues are mostly from the U.S., this growth won’t be lost due to currency conversion, which has dragged down net sales for both Coca-Cola and PepsiCo.

- Non-Carbonates To Join The Party This Year

While both Coca-Cola and PepsiCo have looked to derive growth from their non-carbonated drinks portfolio in the absence of strong CSD growth, Dr Pepper had somewhat struggled to do so in the past, because of the absence of strong Dr Pepper brands in some of the fastest growing segments of the non-sparkling beverage category such as energy drinks, sports drinks, and bottled water. Non-carbonated beverage (NCB) volume declined 1% for the company in 2014, mainly as the letdowns in this segment in the first half offset the stronger performance in the latter half. However, the non-carbonated segment is poised to grow this year, after growing by an impressive 5% in Q1, on the back of strong sales for the ready-to-drink tea brand Snapple, and Hawaiian Punch, which returned to growth in the quarter (~7% volume rise), following consecutive quarters of large declines.

A strong start to the year for the NCB segment set the tone for the rest of the year for Dr Pepper, and along with the expected growth in CSDs, Q2 could be another solid quarter for the Texas-based company.

See the links below for more information and analysis:

- Dr Pepper: home is where the heart, and most of the growth, is

- Dr Pepper earnings review: solid growth across carbonated and non-carbonated segments

- PepsiCo earnings review: snacks and beverages make a good marriage?

- Coca-Cola mid-year earnings preview: strong dollar to weigh on results again?

- Soda makers wonder: where could growth in U.S. come from?

- The strong dollar is weighing down these large beverage companies

- Trefis analysis: Dr Pepper North America CSD Revenues

- Trefis analysis: PepsiCo Soft Drink Revenues

- Trefis analysis: Coca-Cola Revenues

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research