Dr Pepper: Home Is Where The Heart, And Most Of The Growth, Is

To quote the Wizard of Oz– there’s no place like home. This has proven to be true for the beverage manufacturer Dr Pepper Snapple (NYSE:DPS), which has done well in recent times, despite lacking the growth opportunities in emerging markets that its much larger competitors The Coca-Cola Company (NYSE:KO) and PepsiCo (NYSE:PEP) boast of. Dr Pepper has grown market share in the domestic market, and while its compatriots have suffered at the hands of negative currency translations, the company has remained relatively immune to it, deriving ~90% of its net sales from the U.S. itself. The smallest of the three chief carbonated soft drink (CSD) players in the U.S. might be better placed in the near term, and here’s why:

We have a price estimate of $79 for Dr Pepper Snapple, which is roughly in line with the current market price.

See Our Complete Analysis For Dr Pepper Snapple

- Should You Pick General Electric Stock At $165?

- What’s Next For JetBlue Stock After A Sharp 19% Fall Post Q1 Results?

- Is Kimberly-Clark Stock Fairly Valued At $135 After A Solid Q1?

- How Will AMD’s AI Business Fare In Q1?

- Up 9% Year To Date, Will Chevron’s Gains Continue Following Q1 Results?

- Earnings Beat In The Cards For Honeywell?

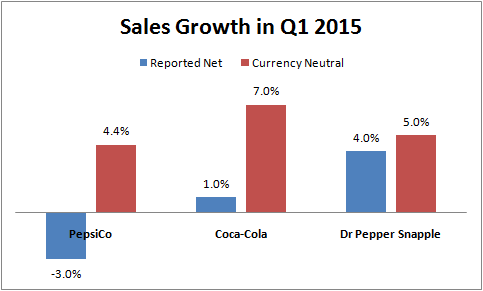

- Strengthening U.S. Dollar?–Not An Issue For Dr Pepper

While markets outside the U.S. form approximately 55% and 50% of the net sales for Coca-Cola and PepsiCo, respectively, only 12% of Dr Pepper’s top line is formed by international markets. (In 2014, 4% and 8% of the net sales came from Canada and Mexico and the Caribbean, respectively.)

As can be seen from the chart, the impact of depreciating foreign currencies is the least on Dr Pepper. After negative currency fluctuations were a 10 percentage point headwind on the top line in Q2, PepsiCo now expects currency translations to drag down full-year net sales and core EPS by 9 and 11 percentage points, respectively. On the other hand, currency is also expected to be a 5 point headwind on Coca-Cola’s net revenues this year. Now compare this to how things stand for Dr Pepper. The falling Canadian dollar and Mexican peso are expected to be only a 1 percentage point headwind on the financial results for the Texas-based company, which is not exposed to the more volatile currencies such as the Russian ruble and Venezuelan bolivar, which have dented reported sales for Coke and Pepsi in recent times.

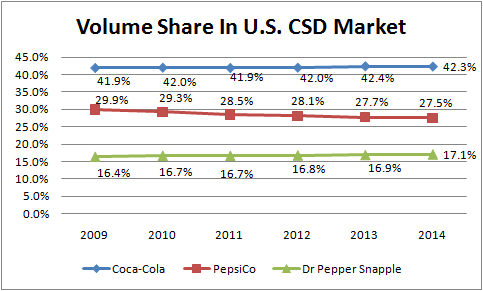

- Dr Pepper Is Growing Volume Share In An Otherwise Mature CSD Market

As consumers continue to cut back on their calorie consumption, the U.S. CSD market declined for the tenth consecutive year last year. Volume growth in this market is hard to come by, and is made even tougher due to the dominance of Coca-Cola and PepsiCo, which together account for almost 70% of the segment volumes. However, as seen from the chart, Dr Pepper has been able to consistently improve its volume share in an otherwise mature CSD market. In fact, the staple Dr Pepper drink grew volumes by 0.5% last year, outperforming both Coke and Pepsi-Cola, and consolidating its position as the fifth-highest-selling soft drink in the U.S. [1]

Apart from being able to achieve volume growth in U.S. CSDs, Dr Pepper has the opportunity to boost its top line through positive mix. Strengthening economic conditions in the country have allowed for an upward push in the consumer-price index for nonalcoholic beverages in recent months. A positive segment mix, i.e. higher proportionate sales of finished goods cases compared to concentrate cases, boosted net sales by 1.5% in Q1, while product mix increased net sales by over 1%. Dr Pepper has raised its retail prices, and combined price and mix could grow by about 2% this year for the company. [2]

There is even more opportunity for Dr Pepper to boost its revenue growth, as the company’s pricing is still lower than its peers. A positive mix is what has fueled top line growth for the company more than positive pricing in the last few quarters. Dr Pepper is not completely in the smaller packages segment, which has been a growth driver for both Coca-Cola and PepsiCo, in terms of higher price per unit in recent quarters. This means that Dr Pepper has further growth opportunities when it comes to CSDs, and could emphasize more on smaller packages, and further increase its product prices to spur revenues.

- Dr Pepper Is Growing More Compared To Coca-Cola And PepsiCo

Dr Pepper might be one of the biggest beverage manufacturers in the U.S., but the company is considerably smaller than its compatriots, whose businesses spread across the world. Coca-Cola and PepsiCo are roughly 12x and 10x as big as Dr Pepper, respectively. The latter has benefited from the stronger dollar and steady economic growth in the U.S. in recent times, especially in the core CSD category, which forms 80% of the net volumes for the company–making it the most significant category. Apart from CSDs, Dr Pepper also has strong non-carbonated beverage brands, such as the Snapple tea brand, which are geared for growth. In fact, as the company is focusing on the premium line of its Snapple tea brand, the effective net pricing and margins are getting a boost.

The top line growth for Dr Pepper has outpaced that of its competitors, mainly as negative currency translations have arrested growth for both Coca-Cola and PepsiCo, but also because of stagnating growth opportunities for both these companies, who are already omnipresent in the country. Dr Pepper still doesn’t exercise a lot of control on its shipping and store deliveries, with 59% of the volumes of the drink Dr Pepper being distributed by bottlers affiliated with Coca-Cola and PepsiCo last year. Dr Pepper’s increasing focus on direct store delivery, which allows the beverage manufacturer to bypass third-party and retailers’ distribution centers, could boost margins going forward, allowing the company to capture downstream margin opportunities.

The domestic market has been kind to Dr Pepper, which is expected to grow by more than the anticipated growth for both Coca-Cola and PepsiCo in the U.S. The P/E ratios suggest that Dr Pepper is the cheapest stock out of the three, while PepsiCo is the most expensive stock. While the stronger dollar, and volatility in some emerging markets, are choking growth for Coca-Cola and PepsiCo, Dr Pepper seems to be better poised to grow its top line and further expand margins. Could this mean that Dr Pepper is undervalued?

See the links below for more information and analysis:

- Dr Pepper earnings review: solid growth across carbonated and non-carbonated segments

- PepsiCo earnings review: snacks and beverages make a good marriage?

- Bottled water is a potential growth category that can’t be ignored

- Soda makers wonder: where could growth in U.S. come from?

- The strong dollar is weighing down these large beverage companies

- Trefis analysis: Dr Pepper North America CSD Revenues

- Trefis analysis: PepsiCo Soft Drink Revenues

- Trefis analysis: Coca-Cola Revenues

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research