Cyclacel Pharma May Bring Huge Returns For The Long Term

Submitted by Scott Matusow as part of our contributors program

Cyclacel Pharma (NASDAQ:CYCC) engages in developing oral therapies that target the various phases of cell cycle control for the treatment of cancer and other serious diseases. Its core area of expertise is in cell cycle biology where the company focuses primarily on the development of orally-available anticancer agents that target the cell cycle with the aim of slowing progression or shrinking the size of tumors, and enhancing the quality of life while improving survival rates of cancer patients. Cyclacel’s lead drug candidate is Sapacitabine, a drug undergoing research for potential use in treating blood and other types of cancers. The companys other product i Seliciclib (CYC202), a CDK (cyclin dependent kinase) inhibitor that is in Phase IIb clinical trial for the treatment of NSCLC; and in Phase II clinical trials to treat nasopharyngeal cancer, as well as in Phase I clinical trials in combination with Sapacitabine to treat cancer.

Sapacitabine is an oral nucleoside analog prodrug that acts through a dual mechanism. I find this oral dosing to be a big benefit if proven effective as most everyone understands the terrible side effects common from typical chemotherapy and other cancer treatments. The compound interferes with DNA synthesis by causing single-strand DNA breaks and induces arrest of the cell division cycle at G2 phase.

- Rising 21% This Year, What Lies Ahead For Exxon Stock Following Q1 Earnings?

- Should You Pick General Electric Stock At $165?

- What’s Next For JetBlue Stock After A Sharp 19% Fall Post Q1 Results?

- Is Kimberly-Clark Stock Fairly Valued At $135 After A Solid Q1?

- How Will AMD’s AI Business Fare In Q1?

- Up 9% Year To Date, Will Chevron’s Gains Continue Following Q1 Results?

Sapacitabine has demonstrated potent anti-tumor activity in both blood and solid tumors in preclinical studies. In a liver metastatic mouse model, sapacitabine was shown to be superior to gemcitabine (marketed as Gemzar by Eli Lilly (NYSE:LLY)) in delaying the onset and growth of liver metastasis.

Sapacitabine oral capsules are currently involved in the following:

- The SEAMLESS Phase III trial being conducted under a special protocol assessment with the FDA as front-line treatment of acute myeloid leukemia (AML) in the elderly.

- Phase II studies for myelodysplastic syndromes (MDS) and solid tumors including lung cancer.

- Investigator-led studies such as a Phase II/III comparing sapacitabine to low dose cytarabine as front-line treatment of elderly patients with AML or high risk MDS unfit for intensive chemotherapy, and a Phase II study in chronic lymphocytic leukemia.

Business Highlights:

- Published results from a Phase 2 randomized trial of single-agent sapacitabine in elderly patients aged 70 years or older with newly diagnosed AML or AML in first relapse in The Lancet Oncology.

- Presented updated data at two separate sessions at The Eighth Annual Hematologic Malignancies 2012 Conference from an ongoing, multicenter, Phase 2 randomized trial of sapacitabine in older patients with intermediate-2 or high-risk MDS after treatment failure of front-line hypomethylating agents, such as azacitidine (Vidaza®) and/or decitabine (Dacogen®). Median overall survival to date for all 63 patients in the Phase 2 study is approximately 8 months. For 41 out of 63 patients with 10% to 19% blasts in their bone marrow median overall survival is approximately 9 months. Twenty-two percent of patients are still alive and longer follow-up is needed to assess 1-year survival and overall survival of each arm.

- Received a grant of approximately $1.9 million from the UK Government’s Biomedical Catalyst to complete investigational new drug (IND)-directed preclinical development of CYC065, a novel, orally available, second generation, cyclin-dependent kinase (CDK) inhibitor.

- Highlighted in multiple poster presentations the personalized medicine potential of Cyclacel’s innovative and diverse oncology pipeline at the 8th National Cancer Research Institute (NCRI) Cancer Conference, including translational findings demonstrating the combination potential of sapacitabine in patients with BRCA1/2 or homologous recombination repair (HRR) pathway defects and the Company’s Polo-Like Kinase 1 (Plk1) inhibitors.

- Entered into an agreement with Sinclair Pharmaceuticals Limited (“Sinclair”) to terminate, effective September 30, 2012, the distribution agreements relating to the promotion and sale of Xclair®, Numoisyn® Lozenges and Numoisyn® Liquid in exchange for a minimum of approximately $1 million in royalty revenues over a period ending in September 2015.

In an October 15th press release, Cyclacel announced positive Phase II study results from Sapacitabine. The company reported that the drug nearly doubled the expected survival rate in elderly patients with MDS after front-line therapy failure. One of these front-line treatment examples is azacitidine, marketed as Vidaza by Celgene (NASDAQ: CELG). I looked at what the sales were for Vidaza since it can give a picture of just a sliver of the opportunities out there for Cyclacel. In the third quarter alone, Vidaza reportedly had sales of $220 million, which obviously translates to close to a billion when put in a year-long expectation. Another example of a front line treatment is Dacogen from Astex Pharmaceuticals (NASDAQ: ASTX).

Prior to the press release, the data was discussed at The Eighth Annual Hematologic Malignancies 2012 Conference being held on October 10/14/12 in Houston, Texas. Median overall survival to date for all 63 patients in the Phase II study is 252 days or approximately 8 months. Median overall survival for 41 out of 63 patients with 10% or more blasts in their bone marrow is 274 days or approximately 9 months.

Median survival for patients with intermediate-2 or high-risk disease, as defined by the International Prognostic Scoring System (IPSS), is 4.3 to 5.6 months. Sapacitabine looks very promising so far, and I am looking forward to seeing what Phase III clinicial results will offer.

Additionally from Cyclacel’s pipeline are seliciclib oral capsules in phase two studies for the treatment of lung cancer and nasopharyngeal cancer and in a phase one trial in combination with sapacitabine. The company’s strategy is to build a diversified biopharmaceutical business focused in hematology and oncology based on a development pipeline of novel drug candidates.

I thought The Life Sciences Report (TLSR) had an excellent interview with John McCamant, (JM) editor of the Medical Technology Stock Letter. During this interview, questions were raised related to blood cancers and potential investments in this area as well as highlighting this landscape as an unmet medical need.

John believes MDS and AML represent nice opportunities for investors. One exchange from the interview in particular between John (JM) and The Life Sciences Report (TLSR) highlights Cyclacel from a valuation perspective and related to the press release I wrote about earlier:

TLSR: We just got some news from Cyclacel. It announced data in an ongoing Phase II trial with sapacitabine for older patients with MDS who had failed azacitidine and/or decitabine. Expected survival rates were doubled. What is your opinion on this study?

JM: We looked at some of the data, and the data looks solid, particularly with the Phase III trial ongoing in AML. That makes a difference for us. The key is the larger Phase III trial with AML: The potential gives the Street and analysts a little more confidence. The Phase II MDS trial does not use a placebo as the control arm, as it would be unethical to not use standard-of-care in elderly and frail patients. We also know that other trials are coming, using the Cyclacel compound in similar cancers. The data have been good to date, and the stock has responded nicely. We look forward to viewing the Phase III data in AML.

TLSR: Do you cover Cyclacel in your newsletter?

JM: No, but we’ve followed Cyclacel over the years. Frankly, it has been slow in development, but things seem to be accelerating, and the valuation looks pretty attractive right now. The company is a little low on cash, so we would not be surprised to see it trying to raise some capital. Also, it does not yet have a partner, which would help validate the technology. But it has a pretty good development team and a very nice pedigree, with Christopher Henney, a co-founder of Dendreon Corp. (NASDAQ: DNDN) and Immunex Corp. (acquired by Amgen (NASDAQ: AMGN) for $16 billion in 2002), as a board member. We’re going to do a little more homework on Cyclacel. We are trying to sit down with management and get its take on what’s going on as the company moves forward.

TLSR: Because of the recent data, Cyclacel’s stock is up sharply over the last month. However, even with its performance, the company only has a $46 million ($46M) market cap.

JM: That’s the key number. We can talk about share prices and all these other numbers, but that market cap really dials us in. For a Phase III cancer company, that’s an unusual valuation. The recent price rise probably increases the odds that the company can go out and raise some money. But Wall Street is skeptical when it comes to unpartnered small biotech companies. It is hard for these types of companies to gain traction or get any visibility. At the end of the day, if Cyclacel keeps doing its job and delivering good data, valuation will take care of itself.

TLSR: Can you speak to Astex Pharmaceuticals (formerly SuperGen Inc.)? It is also heavily involved in the heme/onc space.

JM: Astex is a different type of company. It has been around for quite some time under a different name. It made a good move when it merged with a British company and acquired a platform technology. Now Astex appears to be making some moves forward in the heme/onc space. That being said, we’re looking at a much different valuation.

TLSR: A $276M market cap, right?

JM: The market cap is five times that of Cyclacel. But Astex has an approved MDS product, Dacogen (decitabine), and it generates some revenue with that product. Management is solid. Generally, investors want an exciting molecule rather than a revenue-producing, older cancer drug. It can be difficult running two different companies at the same time-one having a sales organization out there marketing, and the other focusing on research and development. It is a lot for a smaller company to manage effectively.

TLSR: Dacogen is a DNA methyltransferase inhibitor used in MDS and AML. If Cyclacel gets sapacitabine approved for those indications, how much would that eat into Dacogen revenues?

JM: Quite possibly a good bit, because we are talking about a novel oral compound from Cyclacel. Safety is more important in these elderly patients, but efficacy is needed.

TLSR: Would you consider following Astex in your newsletter?

JM: We have been tracking it off and on. We’ve known the company as SuperGen, from back in the day. But we have learned to never say never. The acquisition of Astex Pharmaceuticals (the British company mentioned above; SuperGen changed its name to Astex following the merger), with its discovery platform, is intriguing to us. It looks like the lead molecules make sense and are in the right cancer space. But the company has a different valuation than Cyclacel. We’ll do some work here, but it looks like the more exciting molecule might be at Cyclacel.

{kind=link}

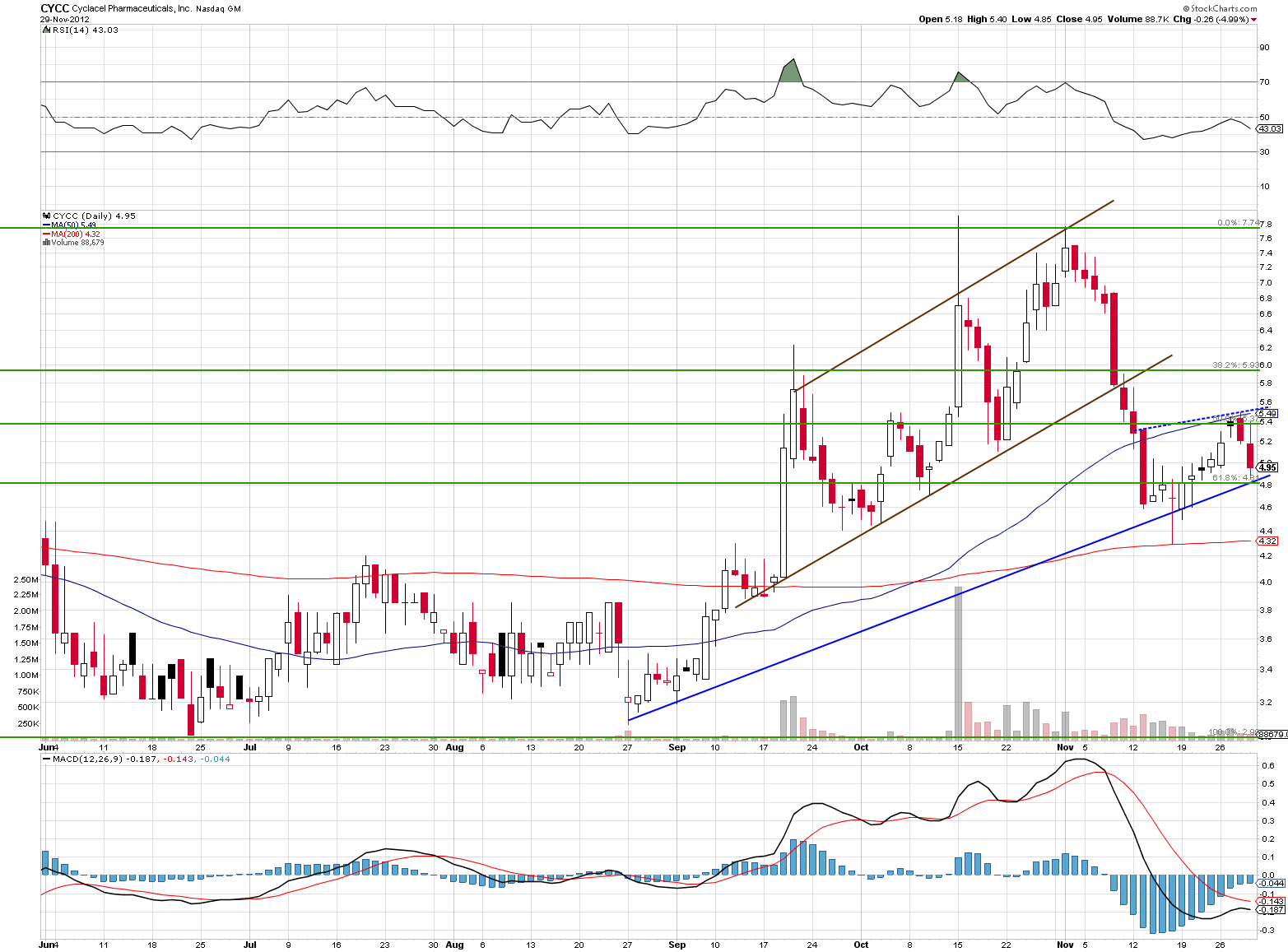

The chart above shows the stock is sitting between the 50% and 61.8% retrace points after coming down from a very strong up channel. It now appears to have found new footing with a new uptrend line. I believe the stock is poised to test the $6.50 level soon, after yesterday’s big move up.

Cyclacel is definitely high risk-high reward in terms of a long term hold. However, if the company’s pipeline confirms, its current market cap of $51.56M should be dwarfed with one 4 to 5 times higher.