Why Is Chesapeake Boosting Production Despite Low Oil Prices?

At a time when most of the oil and gas companies are restricting their operations due to the slump in the commodity prices, Chesapeake Energy Corporation (NYSE:CHK) has plans to expand its 2015 production by close to 4%, beating its original production estimate of a 1-3% increase for the year. The company, which presented at the Barclays Energy-Power Conference last week, attributed this growth to the drastic reduction in its operational costs and superior drilling results from its high quality assets across the US. Doug Lawler, the Chief Executive Officer (CEO) of Chesapeake Energy, who represented the company at the event, also elaborated on the recently signed gas gathering agreements with Williams Companies (NYSE:WMB), in the Haynesville and dry gas Utica shale region, to enhance its volumes as well as margins. In this article, we discuss why the company will be able to sustain a production growth even in a weak oil price environment and what impact this will have on the dynamics of the overall commodity market.

Source: Google Finance

Factors Driving Chesapeake’s Production Growth

- Will Chesapeake See Improved Results In 2019?

- Higher Oil Output And Better Pricing To Drive Chesapeake’s 3Q’18 Results

- Factors That Will Drive Chesapeake Energy’s Value In The Next Two Years

- Chesapeake Q2 Earnings Preview: Commodity Price Strength and Operational Efficiency To Drive Growth

- What Factor Is Driving Chesapeake’s Stock Rally?

- Key Takeaways From Chesapeake’s Q1

Chesapeake acknowledges the fact that the industry is going through a challenging phase. So, in the wake of depressed oil and gas prices, the company slashed its capital expenditure, which was approximately $1.5 billion in the last quarter of 2014, to almost $800 million in the second quarter of 2015, to maintain a flat production for the full year. However, given the slower-than-expected oil price recovery, the company had to further reduce its capital budget to close to $500 million for each of the remaining two quarters in this fiscal. Yet, in spite of this capital discipline, the company now expects its full year production to exceed its previous guidance of 1-3% growth by approximately 5%. This implies that the company is able to produce more while spending less on capital. Now, let’s look at the key factors that are responsible for this surge in production.

Operational Efficiencies

One of the crucial outcomes of the cyclicality in any industry is that the companies use innovative measures to reduce their operational costs in order to survive the down cycle. Same is the case with oil and gas companies, who are currently working hard to improve their costs to weather the current downturn in commodity prices. Like its peers, Chesapeake is also focused at sustaining its profitability in these tough times. In fact, the company has been lowering its lease operating expenses (LOE) and gathering expenses (G&A) by almost 9% annually over the last couple of years.

Chesapeake’s LOE and G&A Cost Structure

To further enhance its margins, Chesapeake recently entered into two gas gathering agreements with its primary gas gathering provider, Williams Companies, for the Haynesville and dry gas Utica shale region. The deal is likely to result in a remarkable reduction in gathering rates in both the regions starting from 2016. According to the company’s estimate, the gathering rates in the Haynesville area are expected to drop by 26% in 2016, and further decline by up to 40% by 2018. This will boost the company’s EBITDA by roughly $200 million annually and strengthen its margins. Given the cost reductions, Haynesville and Utica shale will be a significant part of the company’s portfolio going forward.

Benefit From The Recent Gas Gathering Agreements

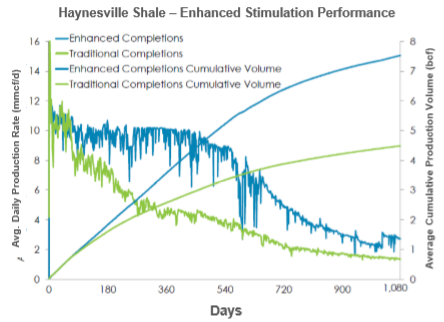

Superior Drilling Results

Apart from focusing on margins, Chesapeake has been stressing improving the recovery rates and reducing the drilling costs of its US onshore plays. For instance, the company has been using enhanced stimulation techniques and longer lateral tests to improve the well performance in its Haynesville area. Consequently, the production cost, which indicates the effectiveness of the company’s operations on the field, in the region has declined by more than 56% in the last one year. Moreover, the volumes from these wells have gone up. This makes the region one of the best quality and highly competitive assets in Chesapeake’s portfolio.

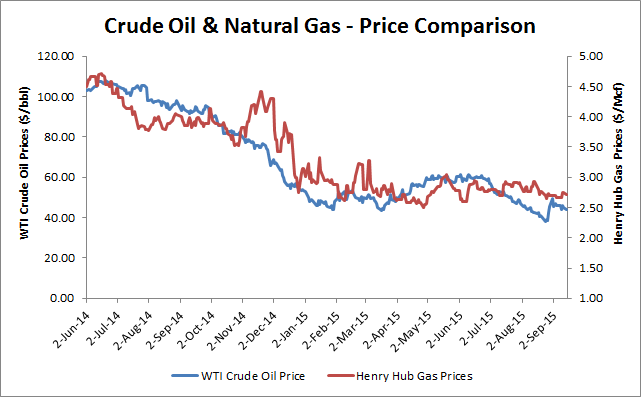

The Henry Hub gas prices, which are used as a benchmark for natural gas prices globally, have also been plummeting over the last 15 months, just like the WTI and Brent crude oil prices. The natural gas prices have averaged at $2.80 per Mcf so far in this year, representing a decline of more than 40% since June of last year. Consequently, it has become very challenging for most of the conventional gas producing companies to sustain their production at these low gas prices.

Source: US Energy Information Administration (EIA)

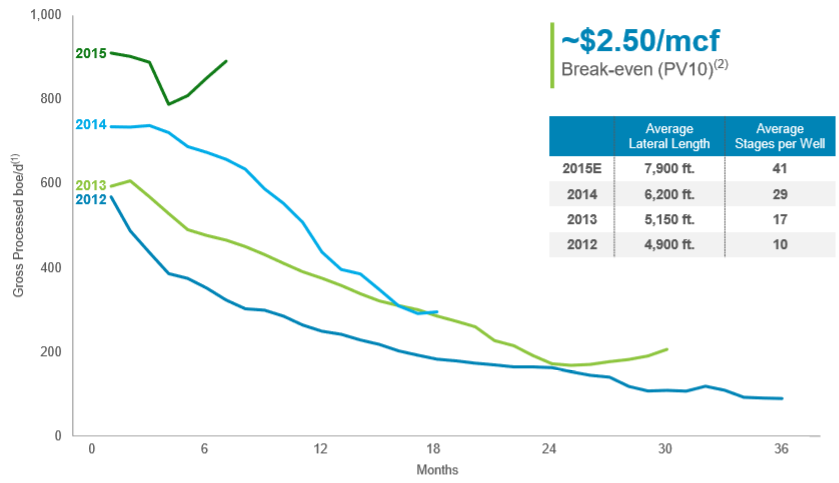

However, Chesapeake has a large exposure to unconventional gas reserves in the form of the Utica shale region, where the company has acreage of over 1 million acres. Due to the company’s ongoing initiatives to improve its operational performance, this region has also been delivering impressive results. On comparing the results with the 2013 performance, we find that the company has managed to drill at a 30% faster rate and has used 50% longer laterals in the region. More importantly, the well cost per lateral foot has declined by 20% over the last two years. This, coupled with the improved production volumes from the region, has pulled down the break-even point of these wells to $2.50 per Mcf, which is notably lower than its peers.

Utica Shale Production Profile

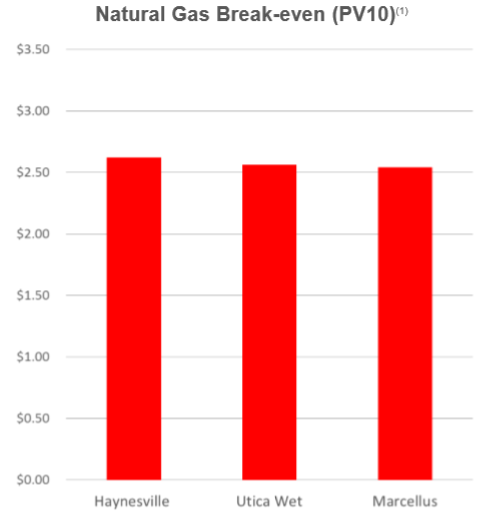

In fact, Chesapeake has managed to sustain a break-even price of around $2.50 per Mcf in most of its gas plays. This, along with the excellent drilling results, has enabled the company to increase its gas production while most of its peers are holding back their operations. Baring these factors in mind, we expect the Utica shale assets to play a key role in the company’s growth even in the future.

Besides the substantial upside from the natural gas assets, Chesapeake also has high quality oil reserves which have the potential to drive the company’s value in a strong oil price market. However, the company has been matching its production to the volatility in oil prices, while continuing to reduce the operational costs from the oil fields. For instance, the well costs per lateral foot in Chesapeake’s Eagleford oil play has declined by 20% in the last three years. Also, the company is very optimistic about its acreage in the Anadarko basin. Overall, the majority of Chesapeake’s oil plays, excluding the Oswego stack in the Mid-continent region, can sustain oil production even at sub-$50 per barrel levels.

Since Chesapeake’s portfolio has a good mix of gas and liquids reserves, that are delivering extraordinary results, it has an option to adjust its production to maintain its margins. Furthermore, the geographical diversity of its reserves also adds to the company’s ability to alter its production based on the commodity prices.

Impact Of Chesapeake’s Production Growth On Commodity Prices

Anyone who has been following the commodity market or the oil and gas sector would know that the global markets have been suffering from an oversupply of almost 2 million barrels of oil, which has been one of the key factors behind the plummeting commodity prices. In such a scenario, where most of the oil and gas companies are holding back their production, if not curtailing it, to ease out the pressure in the market, Chesapeake is expected to grow its production by almost 4% during 2015. While the cost efficiencies and extraordinary drilling results have made it economically feasible for the company to produce more at lower costs, the additional oil that will enter the market is likely to add to the existing oil glut in the markets. However, Chesapeake’s production on a standalone basis may not trigger any volatility in the commodity prices. Yet, any additional production in the already over saturated market is likely to have implicit implications in the larger scheme of things. Thus, it is difficult to quantify the impact that Chesapeake’s production will have on the commodity prices.

Conclusion

The superior results from Chesapeake’s assets, coupled with its cost reduction measures, has enabled the company to expand its production even in the current low oil price environment. Further, the company has an optionality to tamper its production based on the commodity prices. Thus, we believe that Chesapeake is well-positioned to overcome this downturn with its excellent operational performance and high quality assets.

See Our Complete Analysis For Chesapeake Energy Corporation Here

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap