How Will The Virgin America Merger Impact Alaska Air’s Cost Of Capital?

The amalgamation of Alaska Air and Virgin America in an all cash deal of $2.6 billion is expected to create a low-fare carrier offering a premium product and quality service to its passengers. Apart from enabling Alaska Air to expand its footprint in California and complementing its superior customer service, the merger will have a notable impact on the Seattle-based airline’s cost of capital.

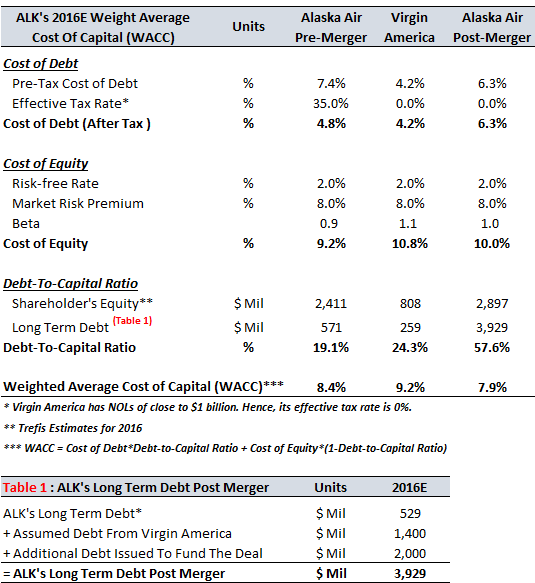

Alaska Air is neither a full-blown legacy carrier nor a low-cost carrier (LCC). Hence, the airline has been expanding its operations to compete with the legacy carriers, while maintaining its low cost advantage against its competitors. Consequently, the airline has managed to deliver industry leading operating margins over the years. However, the market is unsure of the implications that the airline’s proposed merger with Virgin America will have on its overall results. This has resulted in a 20% fall in the airline’s stock price since the announcement of the deal. The major cause of investor concern is that the transaction requires Alaska Air to assume almost $1.4 billion worth of long term debt and lease obligations from Virgin America, which is likely to alter the airline’s capital structure significantly. In our previous analysis, we had shown how the Virgin America merger will impact Alaska Air’s capital structure. While it is clear that the company’s capital structure will become highly levered post the merger, we believe that it could work in the airline’s favor in the long term.

Here we explain, how the merger will result in a lower cost of capital for Alaska Air, which will boost the airline’s valuation in the long term. The table below clearly depicts that Virgin America’s cost of debt (before tax) is notably lower than that of Alaska Air. As a result, even after assuming a significant portion of Virgin America’s debt, Alaska Air’s cost of debt is likely to drop to 6.3% post the merger. Further, Virgin America had net operating losses (NOLs) of over $1 billion at the end of 2015. Thus, Alaska Air’s pre-tax income (post merger) can be easily set off against these NOLs, resulting in zero tax obligations in 2016. Overall, Alaska Air’s cost of debt (after tax) post merger is estimated to be around 6.3% in 2016. This, coupled with the airline’s debt-to-capital ratio of almost 60% post the merger, will reduce Alaska Air’s overall cost of capital from 8.4% before the merger to 7.9% post the merger.

- Should You Pick Alaska Air Stock At $37 After Q4 Beat?

- Will Alaska Air Stock Rebound To Its Pre-Inflation Shock Highs of $70?

- What’s Next For Alaska Air Stock After A 24% Fall This Year And A Downbeat Q3?

- Which Is A Better Pick – Alaska Air Or UAL Stock?

- What’s In The Cards For Alaska Air’s Q2?

- Should You Buy Or Avoid Alaska Air Stock At $52?

Thus, we believe that despite resulting in a highly levered capital structure, the Virgin America deal will have a positive impact on Alaska Air’s cost of capital.

Have more questions about Alaska Air (NYSE:ALK)? See the following links:

- Will Alaska Air-Virgin America Face Antitrust Issues?

- How Will Alaska Air’s Market Share Change Post The Virgin America Deal?

- Why Is Alaska Air Acquiring Virgin America?

- How Will Alaska Air Benefit From The Virgin America Deal Operationally?

- How Will The Expected Return On The Alaska Air-Virgin America Merger Compare With The Previous Deals In The Sector?

- How Will The Virgin America Deal Alter Alaska Air’s Capital Structure?

- Has Alaska Air Paid A Fair Price For Acquiring Virgin America?

- Alaska Air’s Earnings Rise On The Back Of Rapid Capacity Growth And Lower Fuel Costs

- How Has Alaska Air Used Its Increased Cash Flows From Fuel Cost Savings?

- How Will Alaska Air’s EBITDA Be Impacted, If Crude Oil Prices Rebound To $100 Per Barrel By 2018?

- Capacity Expansions And Fuel Cost Savings Boost Alaska Air’s 2015 Results

- How Do Alaska Air’s Operational Statistics Compare With Its Peers?

- How Does Alaska Air’s Market Share (By Capacity) Compare With Its Peers?

- How Does Alaska Air’s Operating Margins Compare With Its Peers?

- How Much Will Alaska Air’s Revenue And EBITDA Grow In The Next 3 Years?

- How Has The Oil Slump Helped Alaska Air’s Operating Margins?

- How Has Alaska Air’s Revenue And EBITDA Composition Changed Over the Last Five Years?

- How Much Has Alaska Air’s Revenue & EBITDA Grown In The Last 5 Years?

- What Is Alaska Air’s Fundamental Value Based On Expected 2015 Results?

- What Constitutes Alaska Air’s Revenue And EBITDA?

- Why We Think Alaska Air Is Worth Much More?

- Why Is Alaska Air Ahead Of Its Peers? – Part 2

- Why Is Alaska Air Ahead Of Its Peers? – Part 1

Notes:

1) The purpose of these analyses is to help readers focus on a few important things. We hope such lean communication sparks thinking, and encourages readers to comment and ask questions on the comment section, or email content@trefis.com

2) Figures mentioned are approximate values to help our readers remember the key concepts more intuitively. For precise figures, please refer to our complete analysis for Alaska Air Group

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap